In this video, Chuck Carnevale, co-founder of FAST Graphs, dives deep into Comcast (CMCSA) to evaluate whether today’s low stock price represents risk or opportunity.

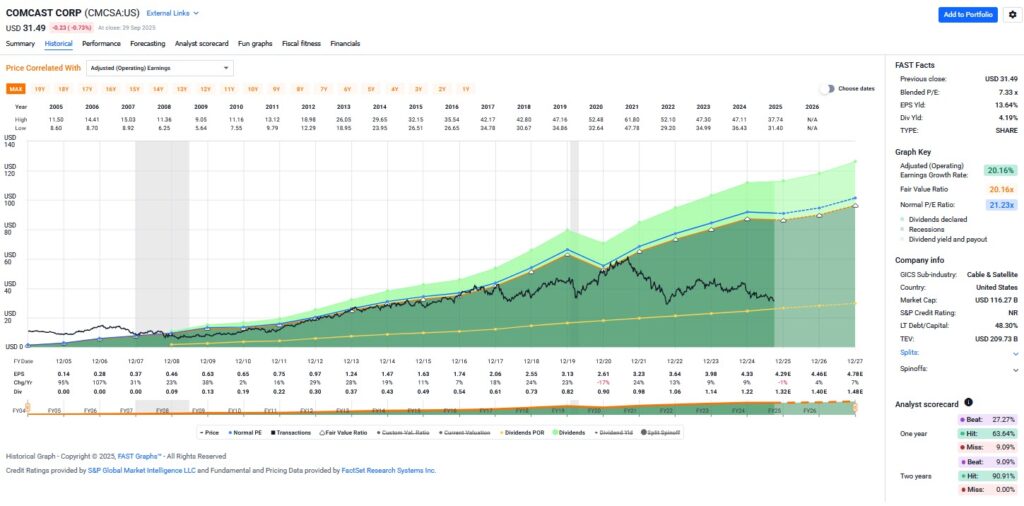

Using FAST Graphs, Chuck shows how Comcast has historically traded above fair value but now sits at one of its lowest valuations in decades. The stock trades at a P/E of 7, roughly half of what would normally be considered fair value for a company growing around 9% annually. At this depressed price, investors get an earnings yield of over 13% and a dividend yield above 4%, with that dividend well-covered by both operating and free cash flow. Comcast has raised its dividend for 18 consecutive years, supported by strong cash generation and ongoing share buybacks.

Despite solid fundamentals, Comcast faces serious headwinds:

While legacy businesses are shrinking, Comcast is investing in:

Analysts expect modest revenue growth of 2–3% and EPS growth of 4–5% through 2028. Morningstar rates Comcast 5 stars, estimating fair value near $49 versus a current price around $31. Depending on valuation assumptions, fair value estimates range from $48–$73 per share. Even at conservative multiples, FAST Graphs shows potential double-digit annualized returns over the long run.

Comcast’s fundamentals—strong cash flows, dividend safety, share buybacks, and diversified businesses—appear much stronger than its beaten-down valuation suggests. The market is pricing in a worst-case scenario for its legacy cable/broadband segment, while discounting the potential of wireless, streaming, and theme parks.

For income investors, the safe 4%+ dividend with room to grow makes Comcast compelling. For value investors, today’s price may represent opportunity rather than risk, with significant upside if sentiment shifts and the company executes on growth initiatives.

FAST Graphs™ is a stock research tool that empowers subscribers to conduct fundamental stock research deeper and faster than ever before.