Introduction

Although many Health Technology Sector companies have significantly outperformed the market on a long-term basis, they have significantly underperformed the market since the beginning of 2015. With only a few minor exceptions, this is true for most companies, especially the pharmaceutical companies, operating in this sector.

On the other hand, there are several examples where operating performance has been exemplary even though stock price performance has been dismal. In my long history analyzing stocks, I have concluded that the combination of strong operating performance coupled with low valuations usually represents great opportunity. The old adage “buy when there’s blood in the street” or Warren Buffett’s recent recommendation “be greedy when others are fearful and fearful when others are greedy” both apply. This particular scenario applies most aptly to the biotechnology subsector within this broader sector.

Finally, the Health Technology Sector once again provides real-life examples and evidence that it is clearly a market of stocks and not a stock market. Consequently, from my point of view, the evidence continues to support the notion that it is more important to pay attention to your individual holdings than it does to the general market at large. As I am now more than halfway through the 20 sectors reported on by FactSet this message becomes crystal clear.

A Sector By Sector Review

In part 1 found here I covered the Consumer Services Sector. In part 2 found here I covered the Communication Sector. In part 3 found here I covered the Consumer Durables Sector and its many diverse subsectors. In part 4 found here I covered Consumer Nondurables. In part 5 found here I covered companies in the Consumer Services Sector. In part 6 found here I covered the Distribution Services Sector. In part 7 found here I covered the Electronic Technology Sector. In part 8 found here I covered the Energy Minerals Sector. In part 9 found here I covered the Finance Sector. In part 10 found here I covered the Health Services Sector.

In this part 11 I will be covering the Health Technology Sector.

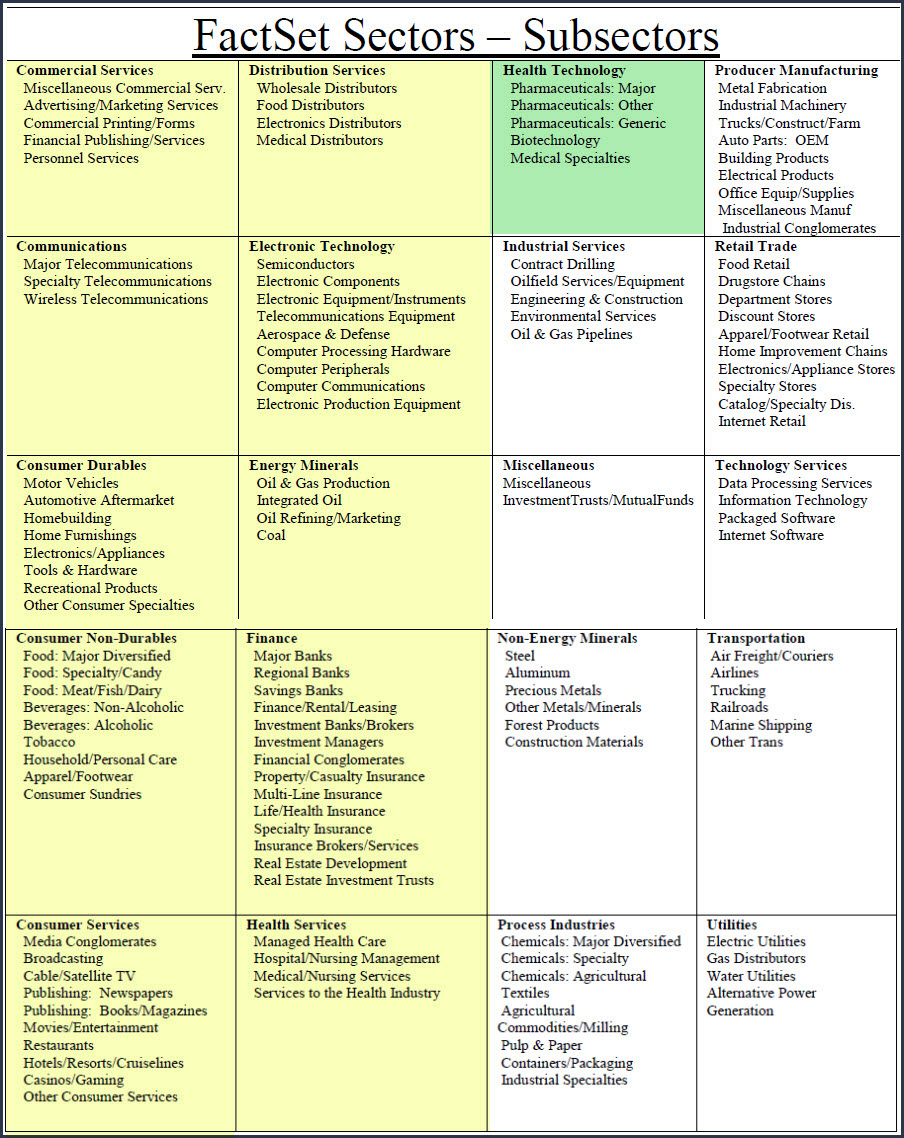

In each article in this series, I will be providing a listing of screened research candidates from each of the following industry sectors, the sector I’m covering in this article is marked in green:

Sector 11: Health Technology

Pharmaceuticals: Major

Pharmaceuticals: Other

Pharmaceuticals: Generic

Biotechnology

Medical Specialties

A Simple Valuation and Quality Screening Process

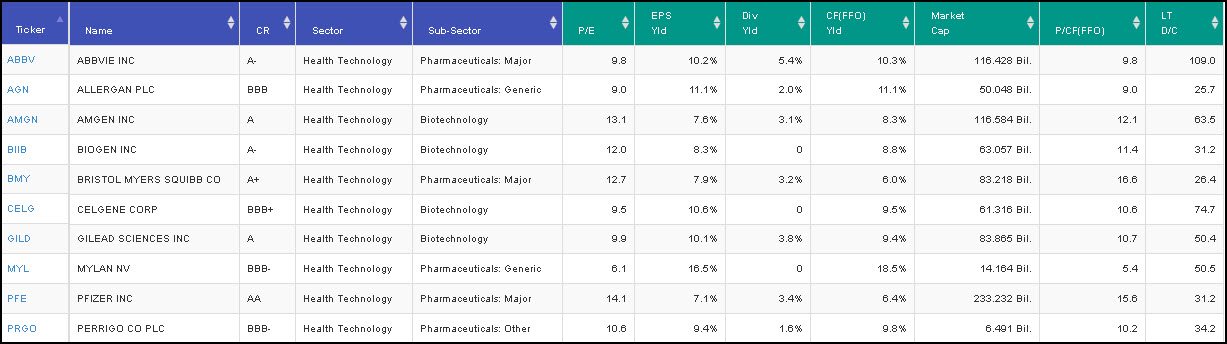

With this series of articles, I will be presenting a screening of companies that have become attractively valued primarily as a result of the bearish market activities experienced in 2018 from each of the above sectors. I will be applying a rather simple valuation and quality-oriented screen across each of the sectors. First, I have screened for investment-grade S&P credit ratings of BBB- or above. Next, I have screened for low valuations based on P/E ratios between 2 and 17. Finally, I have screened for long-term debt to capital no greater than 70%.

By keeping my screen simple, and at the same time rather broad, I will be able to identify attractively valued research candidates that I might have overlooked through a more rigorous screening process. In other words, I’m looking for fresh ideas that I might have previously been overlooking. Furthermore, I want to be clear that I do not consider every candidate that I have discovered as suitable for every investor. However, I do consider them all to be attractively valued. Additionally, I also believe that every investor will be able to find companies to research that meet their own goals, objectives and risk tolerances as this series unfolds

Portfolio Review: Health Technology Sector: 10 Research Candidates

FAST Graphs Screenshots of the 10 Research Candidates

The following screenshots provide a quick look at each of the 10 candidates screened out of over 19,000 possibilities. However, there are only 1256 companies categorized as Health Technology, and these 10 were the only ones I was comfortable presenting in this article. The company descriptions are provided courtesy of the Wall Street Journal. In the FAST Graphs analyze out loud video that follows the screenshots, I will provide additional details and thoughts on the possible attractiveness as well as the potential negatives of each of these research candidates.

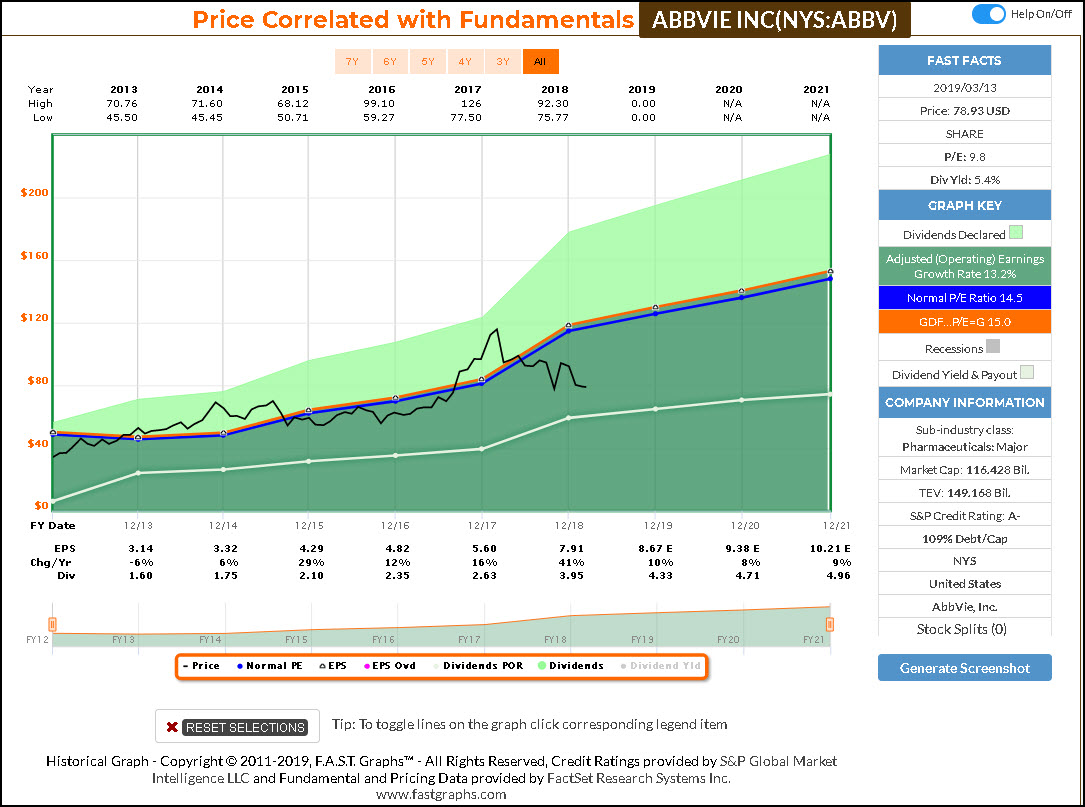

AbbVie (ABBV)

AbbVie, Inc. is a research-based biopharmaceutical company, which engages in the development and sale of pharmaceutical products. It focuses on treating conditions such as chronic autoimmune diseases in rheumatology, gastroenterology and dermatology; oncology, including blood cancers; virology, including hepatitis C virus (HCV) and human immunodeficiency virus (HIV); neurological disorders, such as as well as Parkinson’s disease; metabolic diseases, comprising thyroid disease and complications associated with cystic fibrosis; pain associated with endometriosis; and other serious health conditions.

The company was founded on January 1, 2013 and is headquartered in North Chicago, IL.

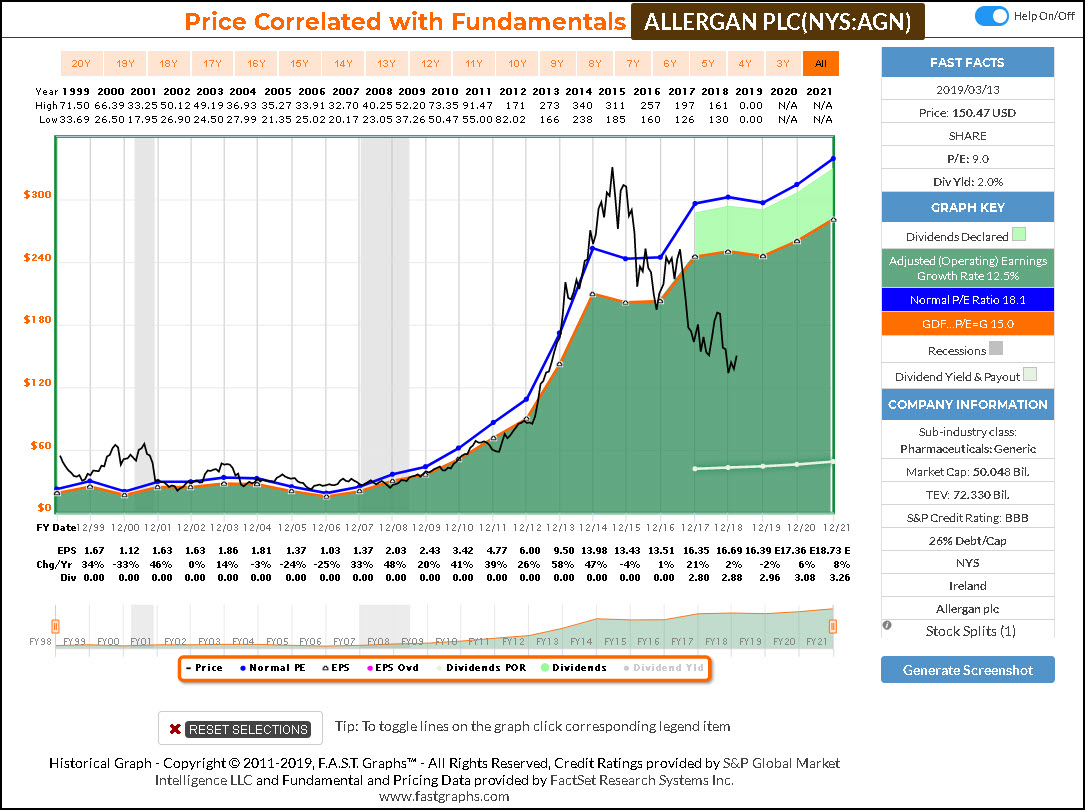

Allergan (AGN)

Allergan Plc engages in the research, development, and manufacture of pharmaceutical products. It operates through the following business segments: US Specialized Therapeutics; US General Medicine, and International.

The US Specialized Therapeutics segment includes sales and expenses relating to branded products within the United States. The US General Medicine segment involves Central Nervous System; Gastrointestinal; Women’s Health; Anti-Infectives; and Diversified brands. The International segment comprises of products sold outside the United States.

The company was founded on in 1984 and is headquartered in Dublin, Ireland.

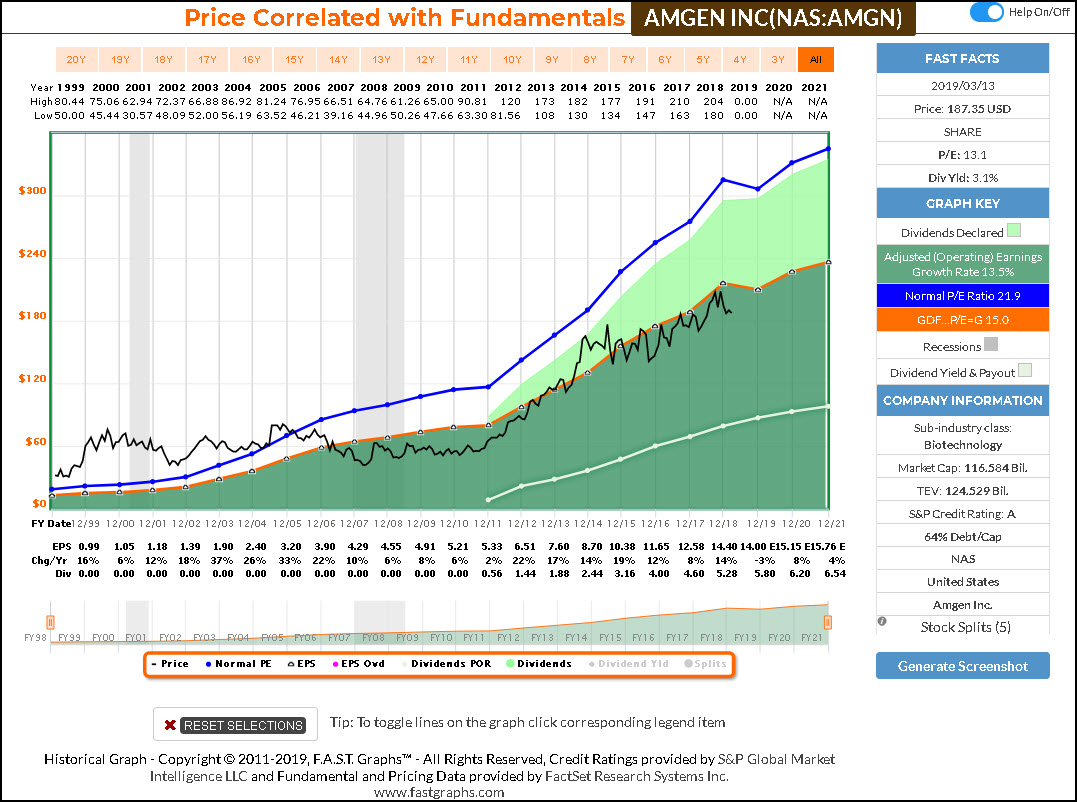

Amgen Inc (AMGN)

Amgen, Inc. is a biotechnology company, which engages in the discovery, development, manufacture and marketing of human therapeutics. Its products include the following brands: Aranesp, BLINCYTO, Corlanor, ENBREL, EPOGEN, IMLYGIC, KYPROLIS, Neulasta, NEUPOGEN, Nplate, Parsabiv, Prolia, Repatha, Sensipar, Vectibix, and XGEVA.

The company was founded by William K. Bowes, Jr., Franklin Pitcher Johnson, Jr., George B. Rathmann and Joseph Rubinfeld on April 8, 1980 and is headquartered in Thousand Oaks, CA.

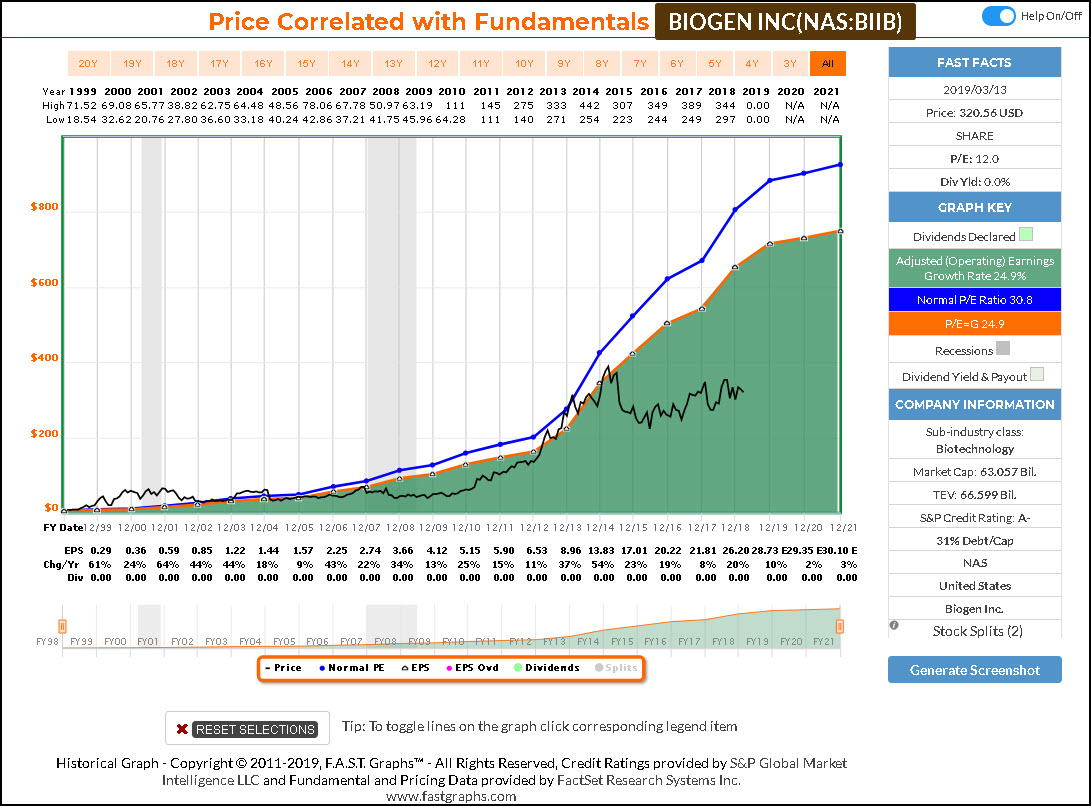

Biogen Inc (BIIB)

Biogen, Inc. is a biopharmaceutical company, which engages in discovering, developing, and delivering therapies for neurological and neurodegenerative diseases. It offers TECFIDERA, AVONEX, PLEGRIDY, TYSABRI, ZINBRYTA, and FAMPYRA for the treatment of multiple sclerosis; SPINRAZA for the treatment of spinal muscular atrophy; and FUMADERM for the treatment of severe plaque psoriasis.

The company was founded by Charles Weissmann, Heinz Schaller, Kenneth Murray, Walter Gilbert, and Phillip Allen Sharp in 1978 and is headquartered in Cambridge, MA.

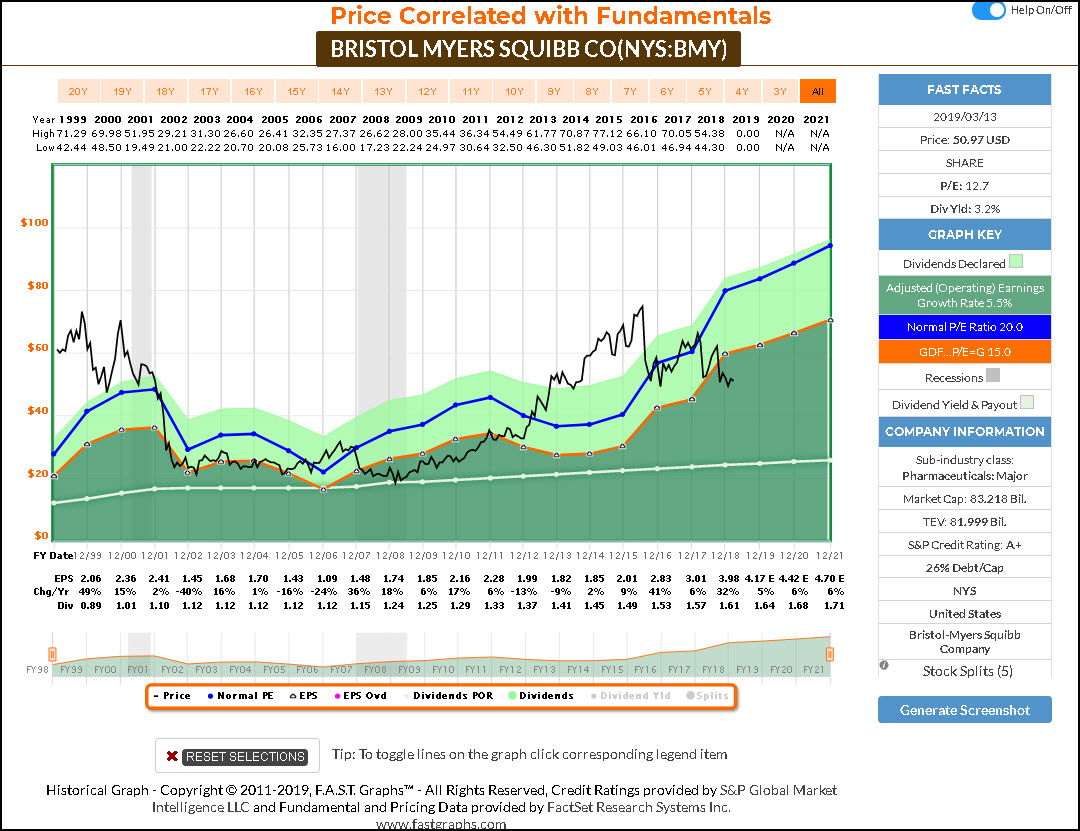

Bristol Myers Squibb Co (BMY)

Bristol-Myers Squibb Co. engages in the discovery, development, licensing, manufacture, marketing, distribution, and sale of biopharmaceutical products. It includes chemically-synthesized drugs or small molecules and products produced from biological processes called biologics.

The company was founded in August 1933 and is headquartered in New York, NY.

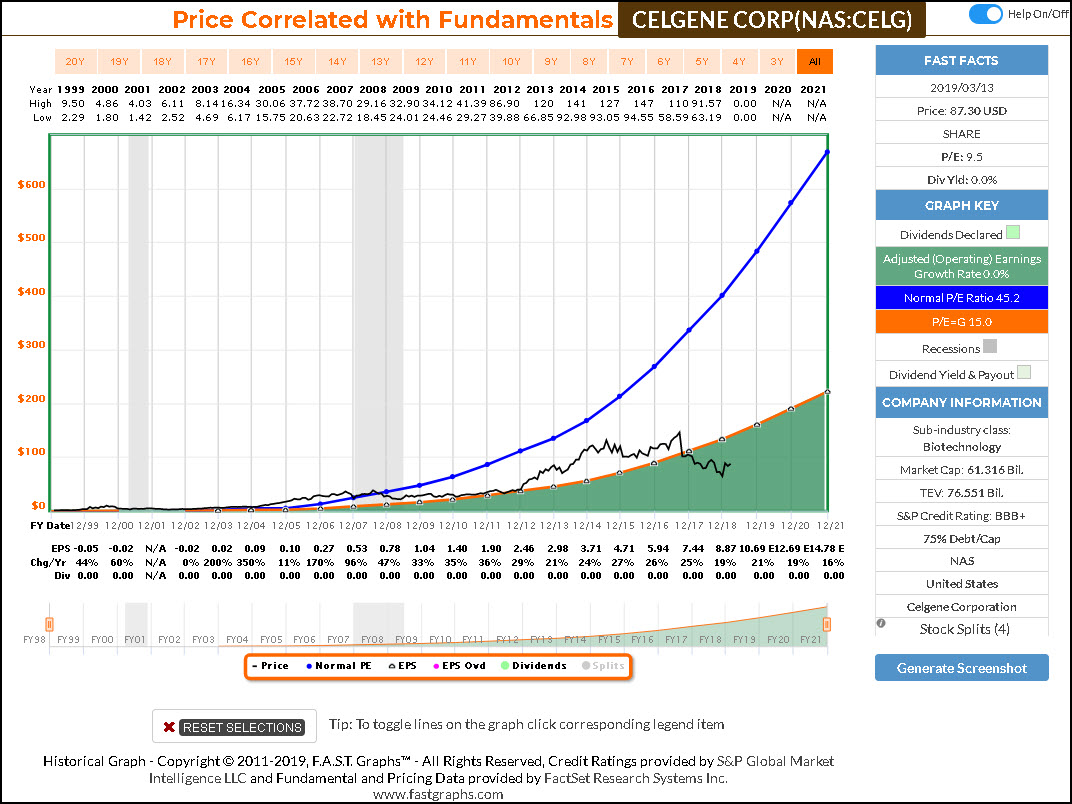

Celgene Corp (CELG)

Celgene Corp. is an integrated global biopharmaceutical company, which engages in the discovery, development and commercialization of therapies for the treatment of cancer and inflammatory diseases. Its primary commercial stage products include REVLIMID, POMALYST, IMNOVID, OTEZLA, ABRAXANE, and VIDAZA.

The company was founded by David Stirling and Sol Barer in 1986 and is headquartered in Summit, NJ.

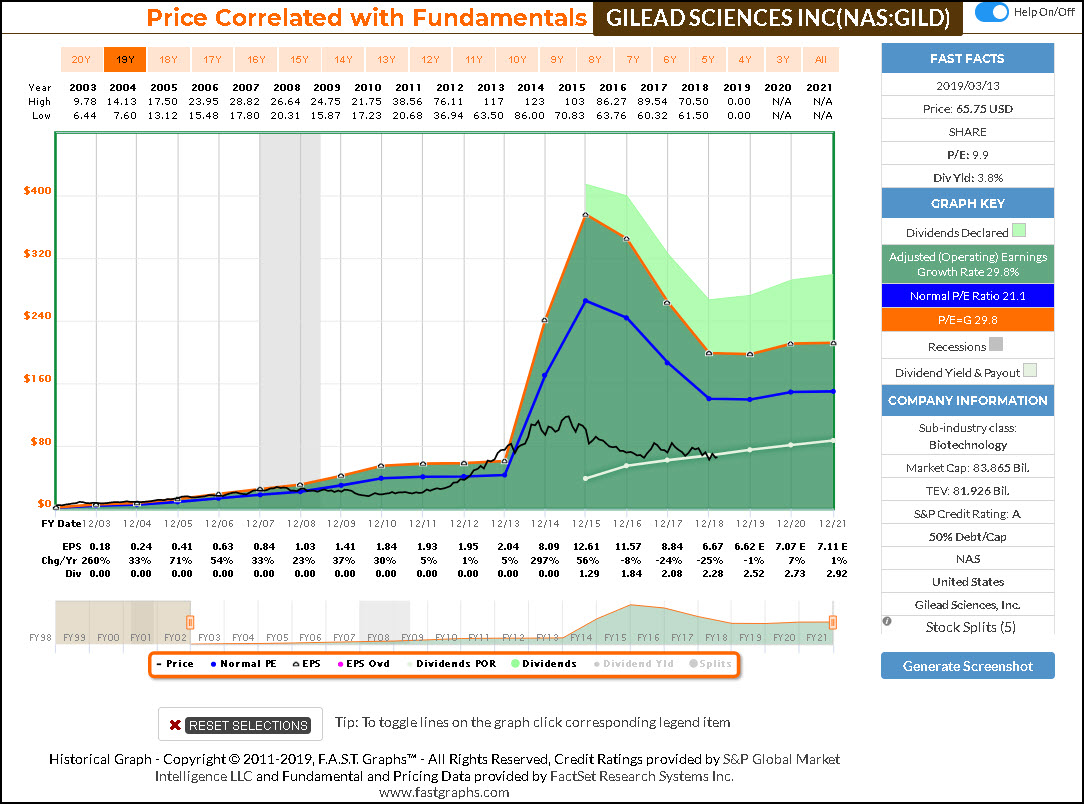

Gilead Sciences Inc (GILD)

Gilead Sciences, Inc. is a biopharmaceutical company, which engages in the research, development, and commercialization of medicines in areas of unmet medical need. Its primary areas of focus include human immunodeficiency virus, acquired immunodeficiency syndrome, liver diseases, hematology, oncology, and inflammation and respiratory diseases. It offers antiviral products under Harvoni, Genvoya, Epclusa, Truvada, Atripla, Descovy, Stribild, Viread, Odefsey, Complera/Eviplera, Sovaldi, and Vosevi brands.

The company was founded by Michael L. Riordan on June 22, 1987 and is headquartered in Foster City, CA.

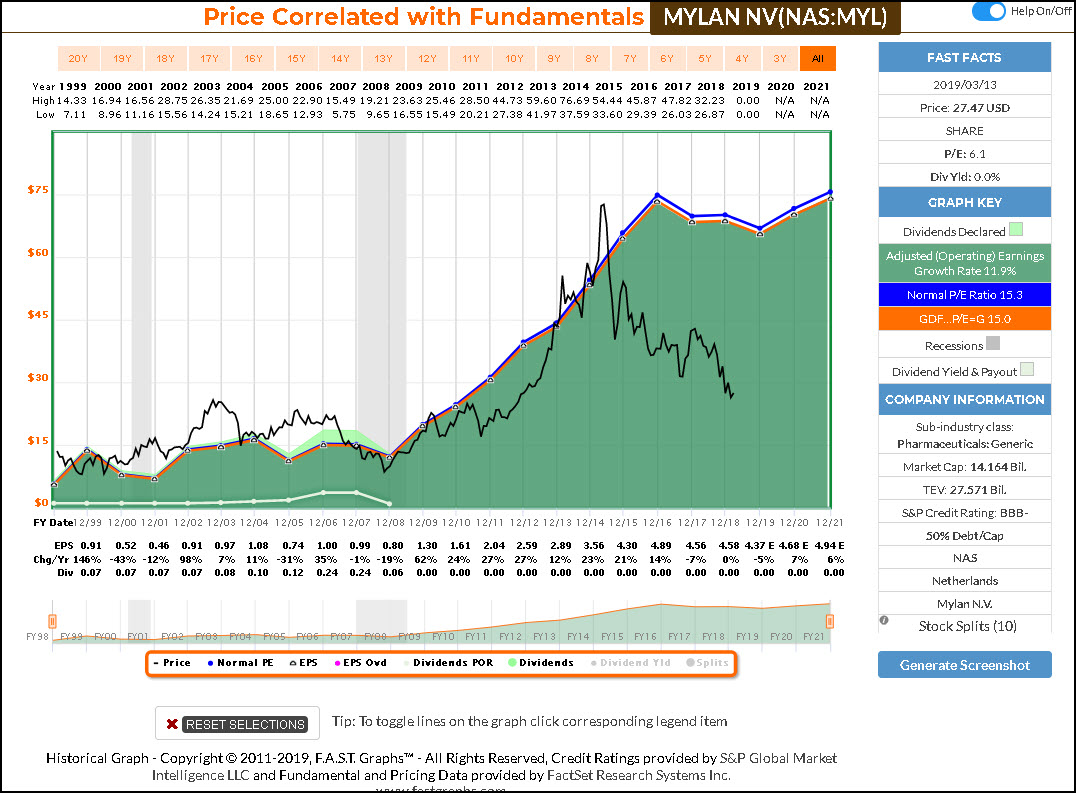

Mylan (MYL)

Mylan NV is a pharmaceutical healthcare company. The firm engages in the development, license, manufacture, market and distribution of generic, branded generic and specialty pharmaceutical products. It operates through the following geographical segments: North America, Europe and Rest of World.

The North America segment develops, manufactures, sells, and distributes pharmaceutical products in tablet, capsule, injectable, transdermal patch, gel, nebulized and cream, or ointment form. The Europe segment operates through subsidiaries in Italy, Germany, the United Kingdom, and Spain. The Rest of World segment comprises of operations in Japan, Australia, China, Brazil, Russia, India, South Africa, Middle East and South East Asia.

The company was founded in 1961 and is headquartered in Hatfield, the United Kingdom.

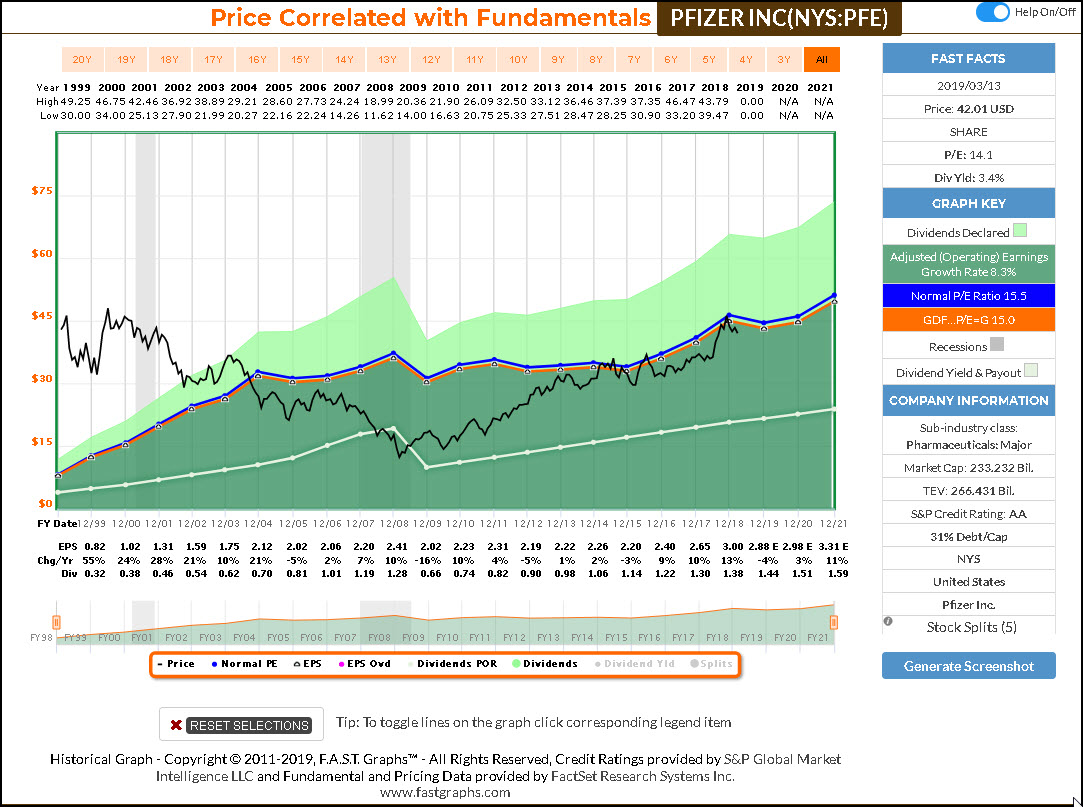

Pfizer Inc (PFE)

Pfizer Inc. engages in the discovery, development, and manufacture of healthcare products specializes in medicines, vaccine, and consumer healthcare. It operates through the Pfizer Innovative Health (IH) and Pfizer Essential Health (EH) segments.

The IH segment focuses on the development and commercializing medicines and vaccines for internal medicine, oncology, inflammation and immunology, rate disease, and consumer healthcare. The EH segment is involved in development and supply of branded generics, generic sterile injectable products, biosimilars, and select branded products including anti-infectives.

The company was founded by Charles Pfizer Sr. and Charles Erhart in 1849 and is headquartered in New York, NY.

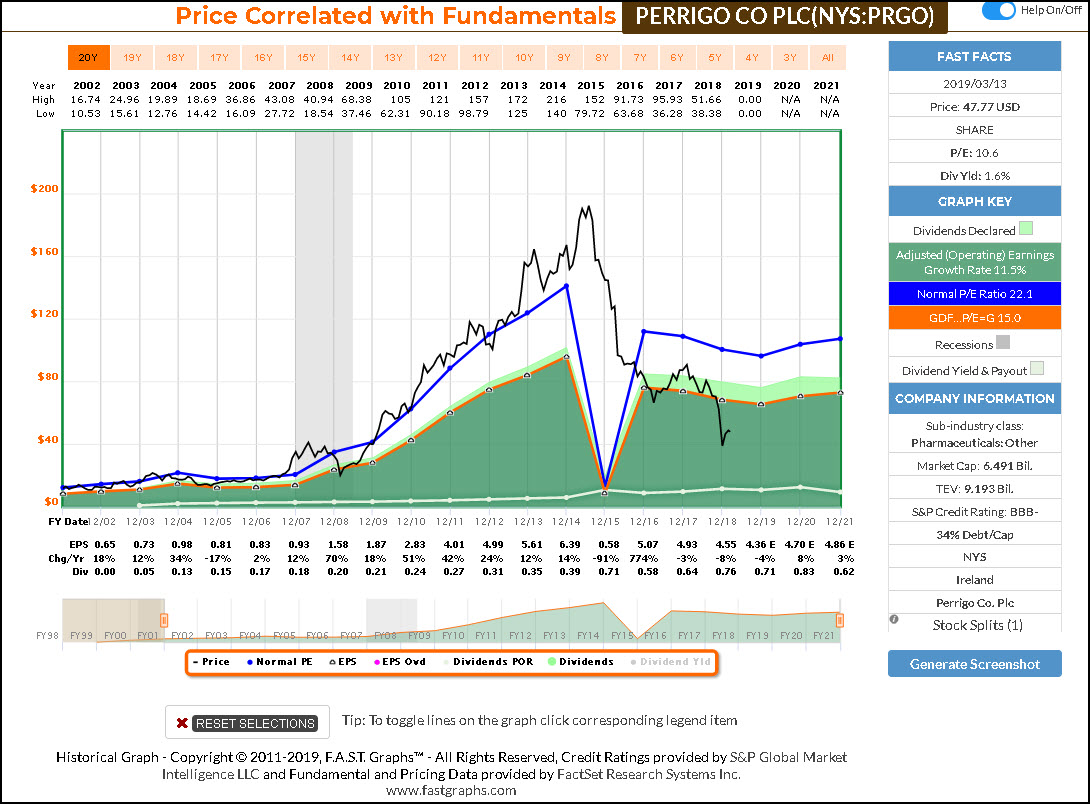

Perrigo Co (PRGO)

Perrigo Co. Plc is a healthcare company, which engages in the production of over-the-counter consumer goods and specialty pharmaceutical products. It operates through the following segments: Consumer Healthcare Americas, Consumer Healthcare International, and Prescription Pharmaceuticals.

The Consumer Healthcare Americas segment comprises the U.S., Mexico and Canada consumer healthcare business. The Consumer Healthcare International segment includes branded consumer healthcare business primarily in Europe and consumer focused businesses in the U.K., Australia, and Israel.

The Prescription Pharmaceuticals refers to the U.S. prescription pharmaceuticals business. The company was founded by Luther Perrigo in 1887 and is headquartered in Dublin, Ireland.

F.A.S.T. Graphs Analyze Out Loud Video:

Summary and Conclusions

The Health Technology Sector – perhaps more than most others – provides something for everyone. If you’re investment objective is growth and total return, the sector offers attractive research candidates. If your investment objective is safe, above-average and growing dividend yield, there are attractive opportunities for you as well. In short, this sector holds interesting pure growth opportunities and above-average yielding dividend growth opportunities as well.

The real challenge is to evaluate whether (or not) politics represent a true threat or whether demographics provide undeniable long-term opportunity. These contra indicators – politics versus demographics – make this sector interesting indeed.

Disclosure: Long ABBV, AMGN, CELG, PFE at the time of writing.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.