Introduction

I am a value investor, and all my investments are made with a long-term objective in mind. Consequently, I am a believer that time in the market is often what matters most. However, I will qualify that remark by saying that you also make your money on the buy side. What this means to me is that time in the market will benefit you most when your initial investment is made at a sound and/or prudent valuation.

Additionally, if you can buy or invest in a stock at a very attractive valuation your long-term results will even be better. But perhaps best of all, the lower the valuation you pay relative to a company’s intrinsic value, the less risk you take and the more money you eventually will make. The risk I am referring to is price or valuation risk.

The reason the risk is lower is because a company is trading at fair value or undervalued levels is less likely to fall as much in a bad market as an overvalued company. Moreover, in the long run a company’s stock price will align with fair value. Consequently, if fundamentals remain solid, it is virtually an inevitability that stock price will recover and most likely advance to new highs. However, this is not market timing because it is not an attempt to forecast short-term price movements. Instead, it is simply calculating the fundamental value of the business based on an estimated discounting of future cash flows to the present value. Which further implies that this is a long-term thinking concept.

To my way of thinking, what I simply stated above is common sense, and many agree with me. On the other hand, there are those that simply cannot or will not embrace or accept the notion of long-term. However, to be fair, there is a reason why many investors cannot embrace or maintain the patience to trust that fair valuation will inevitably manifest. Unfortunately, most investors are quick to judge their holdings over a timeframe that is too short. Therefore, in his 1996 Berkshire Hathaway annual report Warren Buffett provided this sage advice: “if you aren’t willing to own a stock for 10 years don’t even think about owning it for 10 minutes.”

Nevertheless, the real problem is that although the reversion to the mean, as statisticians would call it, are virtually an inevitability, the time it takes the reversion to occur is not precise. Once again Warren Buffett explains it quite succinctly with the following quote: “The fact that people will be full of greed, fear or folly is predictable. The sequence is not predictable. Warren Buffett.”

My Inspiration for This Article: How Long Do You Wait for An Undervalued Stock to Recover?

Although what I’ve written above is truthful and accurate, it lacks a level of precision that many people want or need. Consequently, as a value investor, one of the more common questions that I receive goes something like: how long must I, or how long do I, need to wait before the mean reversion rewards me? Investors have a strong need and desire for precision in that answer, however, the unfortunate truth is that the required timeframe often can or will try the investor’s patience beyond what they can tolerate.

Therefore, what I believe investors really need is an antidote to sooth their anxiety. Trust is the only remedy that I believe could accomplish this. However, investors cannot trust short-term stock price volatility because it is not only unpredictable, it is also very irrational at times. Consequently, you cannot really apply logic or common sense to irrational behavior. Of course, if you could, it wouldn’t be irrational.

Investors can trust fundamental values because they are tangible whereas emotional responses (short-term volatility) is intangible. Fundamentals such as earnings, cash flows, revenues, dividends and balance sheet items can be precisely measured and intelligently evaluated. But perhaps most importantly, in the long run this is what drives stock prices (values). This is exactly what Ben Graham was attempting to teach us with his market metaphor: “In the short run, the market is a voting machine, reflecting a voter registration test that requires only money, not intelligence or emotional stability. But in the long run, the market is a weighing machine.” It is this profound investing principle that produces the inevitable reversion to the mean.

Although I am steadfast in my belief in the philosophical reality of the above, I also understand that it is not enough for many people. Instead of rational theory, they want precise answers to the questions of how long you should wait for value to manifest. This fact became vividly clear to me based on the following comment made by a regular reader in my previous article “Valuation Is More Important Than Politics Or Interest Rates: And Most Stocks Are Overvalued Today.” Here is the well-articulated comment that served as the inspiration for this article:

“Chuck Carnevale is commendably clear in explaining the criteria by which he values a company. He is no less clear in identifying some of the companies that are over- or under-valued by these criteria.

He is remarkably imprecise, however, in identifying the time periods in which these predictions are likely to work out. Stock market performance can only be measured by total returns (dividends + capital appreciation) between time T1 and time T2. It matters not whether this time period is 1 day or 1 lifetime. It does matter to individual investors, however. We can’t make much sense of Chuck’s predictions unless we have some idea of the time period he is talking about.”

What is the Long-Term?

As I indicated above, there is no precise or specific answer to the questions posed above. Furthermore, I want to be clear that the only “prediction” that I ever make is that price will inevitably move into alignment with fair value – if fundamentals dictate. However, there are insights that can be offered that simply relate to the definition of the long-term in contrast to the short-term.

Conceptually, the long-term implies a timeframe long enough for a business to create and generate additional value to its shareholders. More simply stated, a timeframe long enough to produce revenue, earnings, cash flow and dividend growth, etc. My personal short form definition is at the minimum a business cycle. Business cycles are generally (but not precisely) defined as 3 to 5 years in length, once again, at a minimum. But the longer the better, i.e., Warren Buffett’s above suggestion for owning a stock for at least 10 years.

Additionally, the rate of earnings growth going forward will be a major factor regarding how quickly and to what extent an undervalued stock will rise (revert to the mean). Faster earnings growth will shorten the timeframe it takes to recover, while slow or negative earnings growth will lengthen the timeframe. Regardless, when attempting to make a sound long-term investment decision, the company’s relative valuation coupled with these factors will provide insights, not precisely, but generally as to how quickly you can expect the stock to return to its fair value justified level.

So, in summary, you cannot know with perfect precision or accuracy when an undervalued stock will return to its fair value levels. On the other hand, you don’t necessarily need to wait until a stock recovers all the way to fair value. If a stock is performing well as a business, and your original purchase price was low (undervalued), you can make extremely good long-term returns as the stock is in the process of reverting to the mean. In order to whet your appetite, I offer the following examples of once undervalued stocks that were reverting to the mean, but had not fully gotten there, with return calculations provided.

These are all examples of companies that I had written articles about indicating that they were undervalued at the time. Each example is listed by the title of the article and the date it was published. With most of these examples I run the return calculations at the minimum holding period of 3 years. However, I do run a couple out through the five-year timeframe. Nevertheless, as you can see, investors purchasing the stocks when they were undervalued did quite well over the minimum business cycle timeframe notwithstanding that the stocks had not yet fully recovered to full value. Furthermore, you might note that most of the stocks went on to become dramatically overvalued generating enormous returns for investors with foresight to buy them when no one else wanted them.

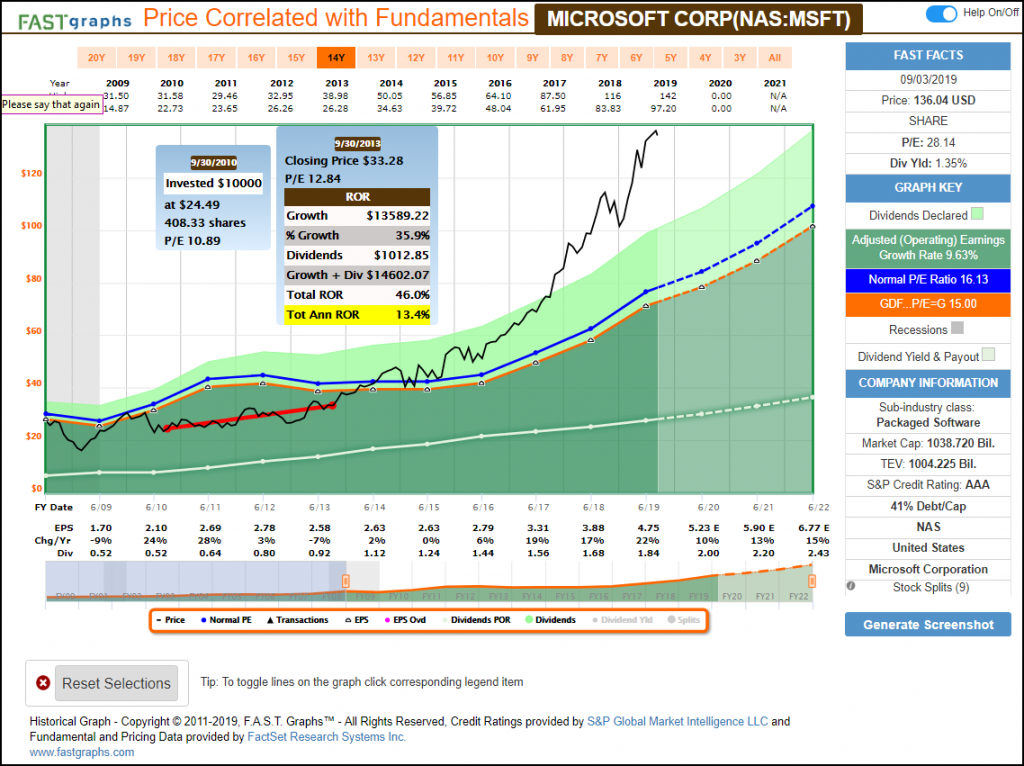

After a Lost Decade, Is Microsoft a Buy? September 2010

When Microsoft (MSFT) was undervalued in 2010 through 2013, it was an excellent investment even though earnings growth was faltering. Fast forward to today and the results of buying Microsoft when it was inexpensive are extraordinary (this calculation not shown below but will be in the video that follows).

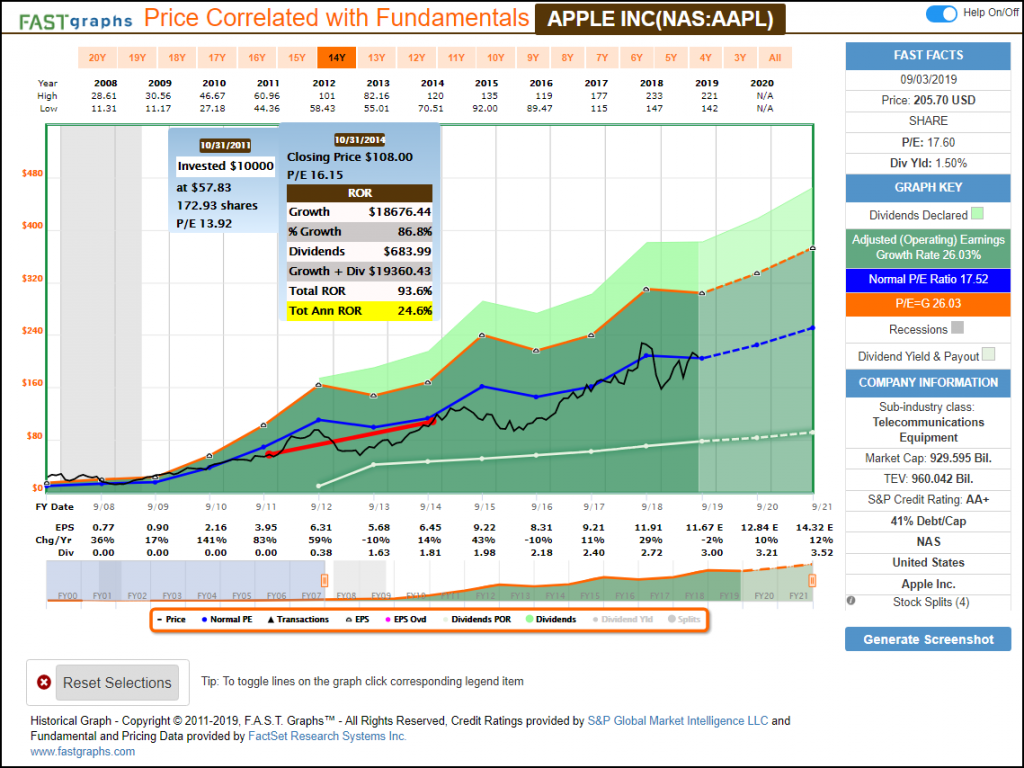

Steve Jobs’ Legacy, and Apple’s Record, Will Live On: October 2011

Apple (AAPL) was very inexpensive in 2011 and produced exceptional total returns over the next 3 years even though it did not move back into alignment with its earnings justified value (the orange line on the graph).

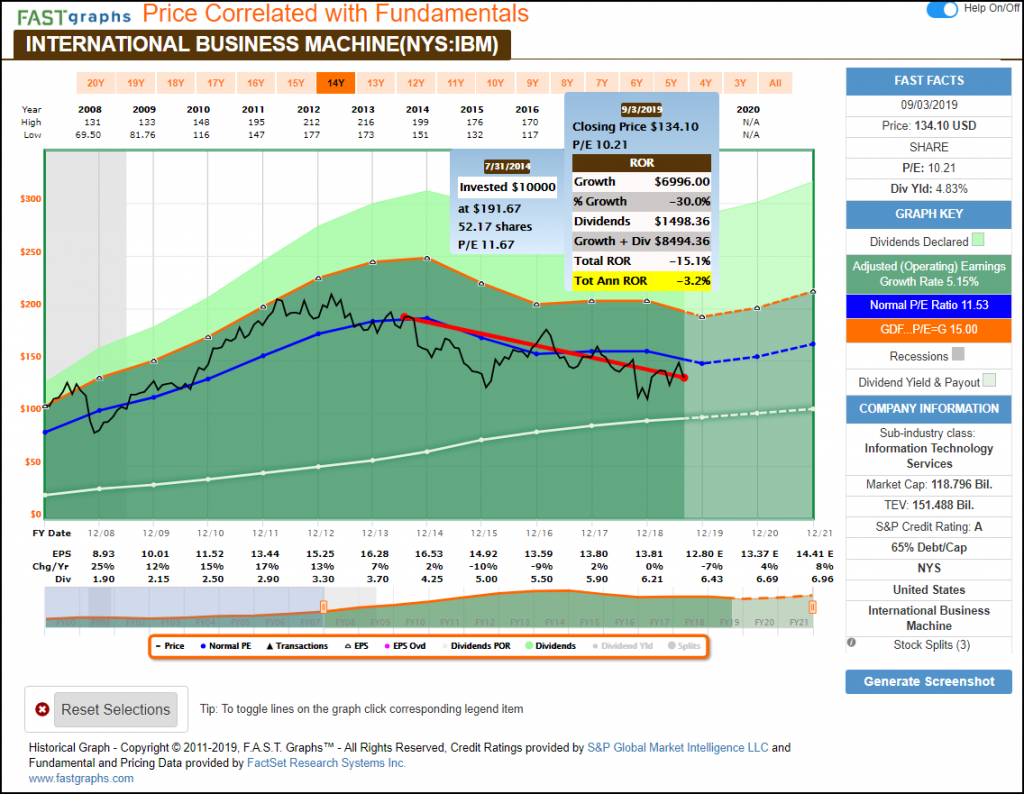

I Feel Like A Thief Buying IBM At Today’s Low Valuation: August 2014

I originally invested in International Business Machine (IBM) for the dividend and dividend growth. Thus far, it has been disappointing on a total return basis and in this case, I’ve run their calculation out to the five-year timeframe. However, IBM has produced double-digit dividend growth which was what I bought it for. Finally, I am quite content and happy to own this stock for another 5 years and I believe I will be well-rewarded for doing so. Time will tell.

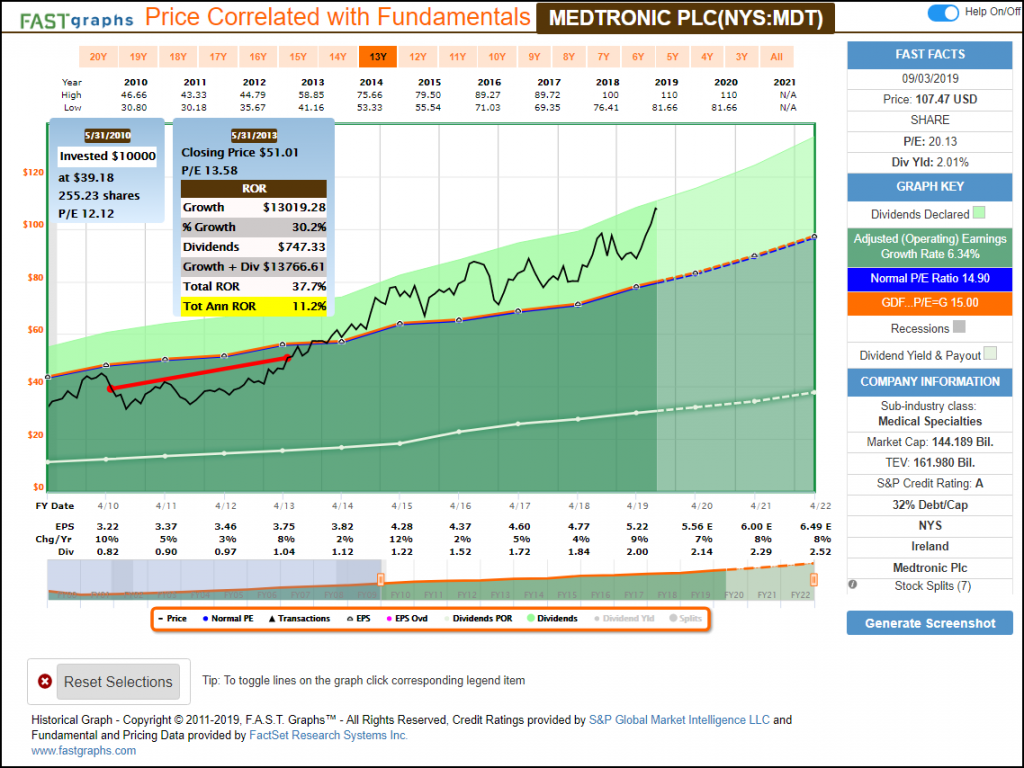

Medtronic: High Quality, High Growth, More Dividends: May 2010

Medtronic (MDT) performed well over the 3 years after I originally wrote the article. But most importantly, its low valuation at the time of my writing set it up for extraordinary longer-term gains. These longer-term calculations are not shown below but will be in the video. Furthermore, the video will also show how insidious overvaluation can be to long-term returns.

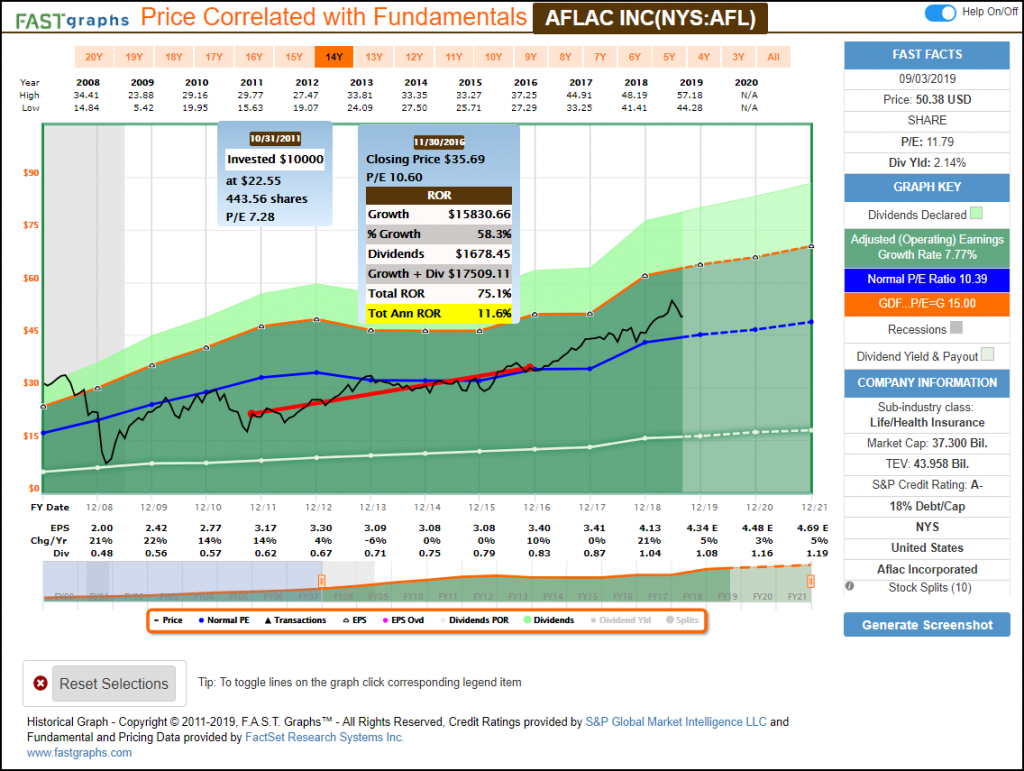

Aflac’s Fair Value PE Ratio Should Be Double, And So Should Its Price: November 2011

Aflac (AFL) was undervalued when I wrote about it in November 2011. Although I did not get the double in the P/E ratio that I suggested, nor did I get a doubling in its price. Nevertheless, I am happy with the results especially considering that I feel Aflac remains an undervalued dividend growth stock even today.

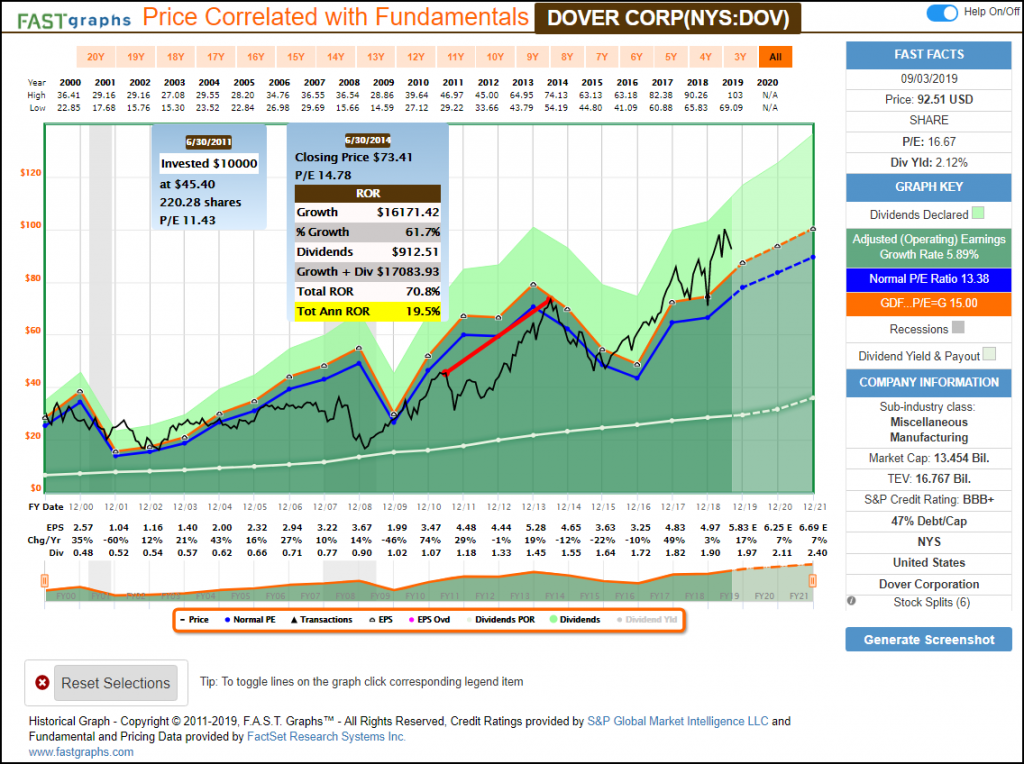

Is Dover Corp. a Cyclical, Growth or Dividend Growth Stock?: July 2011

I included Dover (DOV) because it’s a cyclical stock and I wanted the reader to see the potential pitfalls that a cyclical company can bring regarding capital appreciation. Note that the dividend growth has been excellent, but also note that the stock price fell precipitously over the next 2+ years as earnings entered a down cycle. On the other hand, price has since recovered quite nicely.

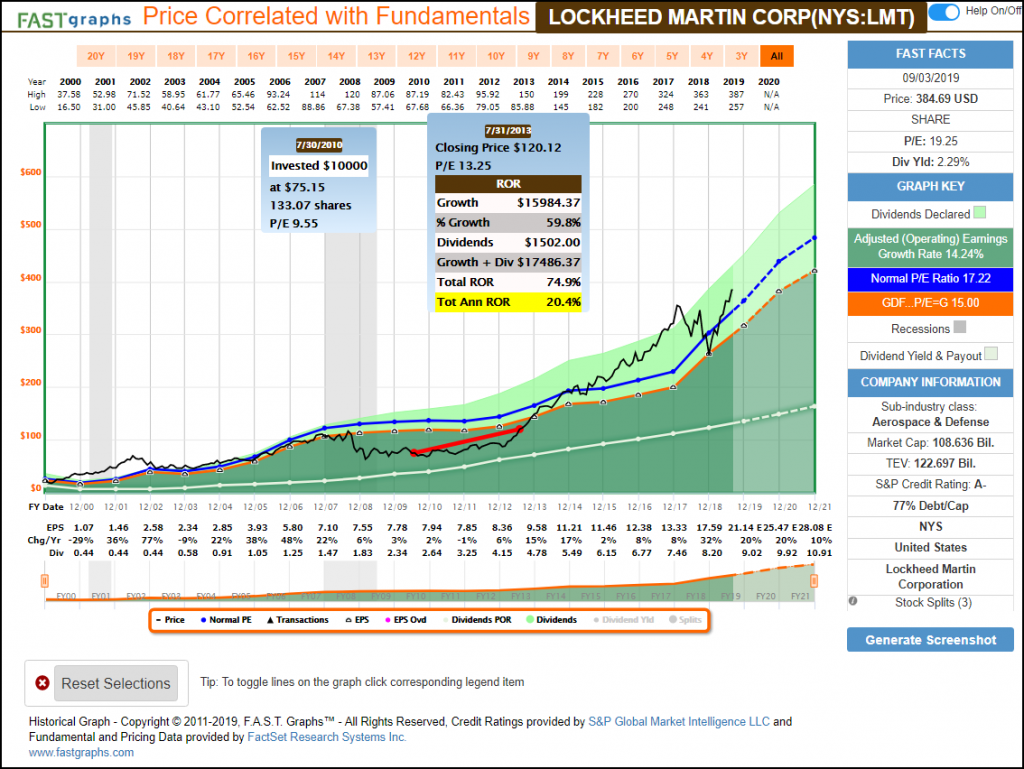

Lockheed Martin Corp: Fundamental Stock Research Analysis: July 2013

The Lockheed Martin (LMT) example does show that the company stayed very undervalued for several years following the Great Recession. However, the reader should also note that earnings growth was very muted during this timeframe. Furthermore, once earnings growth began to accelerate, the stock price accelerated and followed.

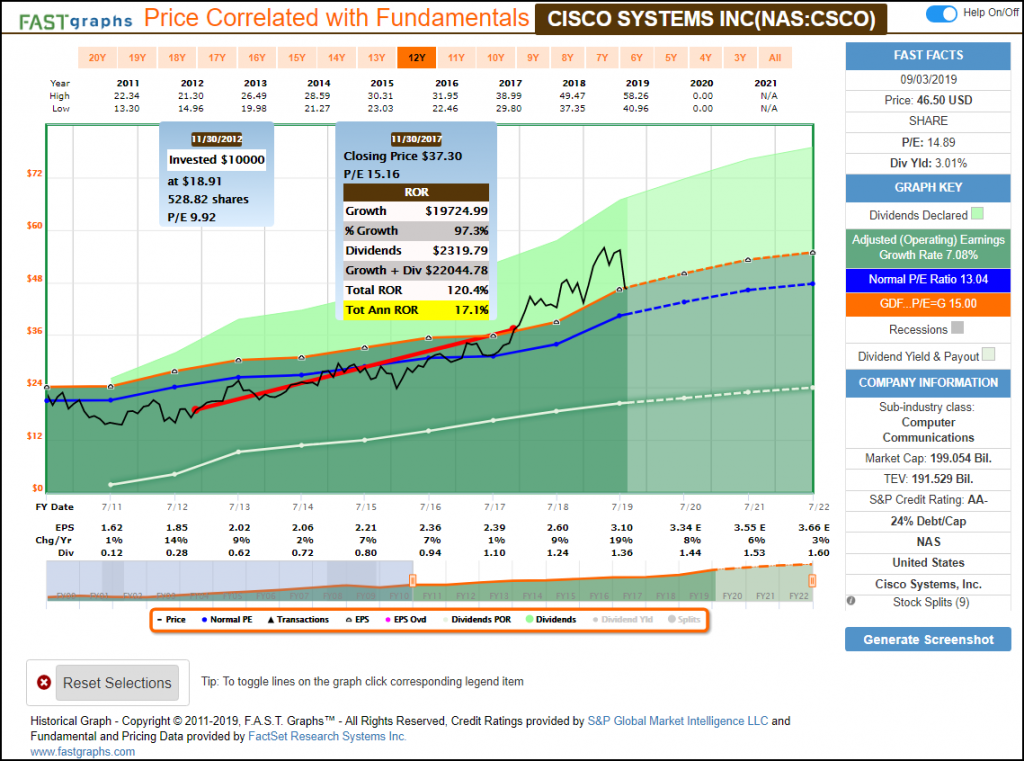

Cisco: Switch To This Undervalued Dividend Growth Stock To Boost Your Portfolio: November 2012

Cisco (CSCO) performed exceptionally well for the 5 years it took following my article before the company’s price fully reverted to the mean. However, what is not shown below but will be in the video is just how crazy the market can be at times, and how damaging it can be to returns in spite of excellent operating performance. You won’t want to miss it.

FAST Graphs Analyze Out Loud Video

Although a picture is worth a thousand words, a video utilizing a live interactive graph is worth many more. Consequently, in the following analyze out loud video I will expand on covering the amount of time necessary for a stock to revert to the mean. Furthermore, as a bonus I will also utilize several of these examples to illustrate the opposite and more nefarious results (or lack thereof) that overvaluation causes.

Summary and Conclusions

The key takeaway that I am attempting to convey to the reader is the inevitability of price moving towards alignment with fair value. Moreover, this principle applies when a stock is overvalued, as well as it does when it is undervalued. However, the precise timing when this may occur is uncertain. On the other hand, the faster a company grows its business (earnings, cash flows revenues, etc.) following the purchase the less time it takes for the stock price to move back to alignment. This factor also will impact investor sentiment which tends to be a short-term oriented concept. In other words, if a company is reporting excellent earnings quarter after quarter sentiment that might’ve once been negative will rapidly turn positive. Nevertheless, as suggested, this might take more than one quarter to take effect.

I also hope that investors recognize and picked up on the idea that good returns can occur while the stock is on its journey to fair value. In other words, you don’t have to wait until the full recovery occurs to enjoy excellent total returns (capital appreciation plus dividend income). When you can find a great company on sale you can significantly enhance your returns and lower your risk. Buying low and selling high (if selling ever occurs) is the prime directive of all common stock investors. But most importantly, don’t underestimate the potential power and benefit of investing in a great stock on sale. You not only get the growth of the company, but you get leverage without the risk of borrowing anything.

Disclosure: Long AAPL,IBM,MDT,AFL,CSCO

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.