Introduction on Stock Valuation

When it comes to writing about investing in common stocks, my favorite theme typically revolves around valuation. In fact, I once had a reader dub me “Mr. Valuation.” Which, I might add was very flattering to me. Moreover, in the context of discussing valuation, there are normally three concepts that are included. They are typically fair valuation, undervaluation or overvaluation.

Oh, but would it not be wonderful, if everything about valuation were that simple. In truth, the concept of valuation is much more complex than those three simple notions. Therefore, one of the primary objectives of this article is to broaden the reader’s perspectives and understandings of the incredibly important concept of valuation as it relates to investing in common stocks.

However, before I delve too deeply into this subject, I would like to offer these following positioning statements:

1. Just because a stock is technically trading at fair value, does not necessarily mean that it is a good or attractive investment.

2. Just because a stock is moderately overvalued, does not necessarily mean that it is a poor or unattractive investment.

In truth, there are circumstances where a moderately overvalued stock is a much better investment than a stock that is at fair value. The key, as will be discussed later, revolves around the potential growth of the respective company. At its core, investing at sound valuation empowers you to participate in the results that the business generates on your behalf as a stakeholder. When investing at sound valuation, if the business generates strong growth, the rate of return you can expect will also be strong -and vice versa.

Valuation is a Measurement of Risk and Prudence

Therefore, to summarize, valuation is but one important component of successful stock investing. Furthermore, I would argue that valuation is more relevant to the soundness of the investment than it is to the total return the investment can achieve. Therefore (and I will elaborate more on this later in the article), two companies with vastly different growth rates can technically be fairly valued with the same P/E ratio. However, the potential future performance of each can be materially different as a function of each respective company’s growth potential.

A Conceptual Definition of Fair Value

If you look up the term fair value on sites such as Investopedia or Wikipedia and others, you will discover what I believe are vague and even somewhat esoteric definitions. Therefore, I believe it is important that I offer my own definition of fair value so that the reader can at least be cognizant of the precise concept I am referring to. To me, fair value, as it relates to common stock investments, is manifest when the current earnings yield provided by the company’s profits, adequately compensates me for the risk I am taking by providing both a realistic and acceptable return on my invested capital.

When referencing my definition of fair value, it’s important to focus on the concept “current earnings yield.” There are a couple of reasons why I feel this is both rational and important. First, it’s vitally important to recognize that any cash producing investment is worth a multiple of its cash flow generation (earnings, etc.) greater than one. This principle applies whether there is growth associated with the investment or not.

However, and this is the part that often confuses investors, two companies with significantly different growth rates can both be fairly valued with the same P/E ratio (I will be discussing this more fully in Part 2). Remember, as previously stated, current valuation is a measurement of soundness based on the current earnings yield for each company. In contrast, the future earnings yield (growth) will be a primary determinant of the rate of return you end up achieving in the long run.

4 Examples: Above Average Growth, Low Growth, Average Growth and High Growth

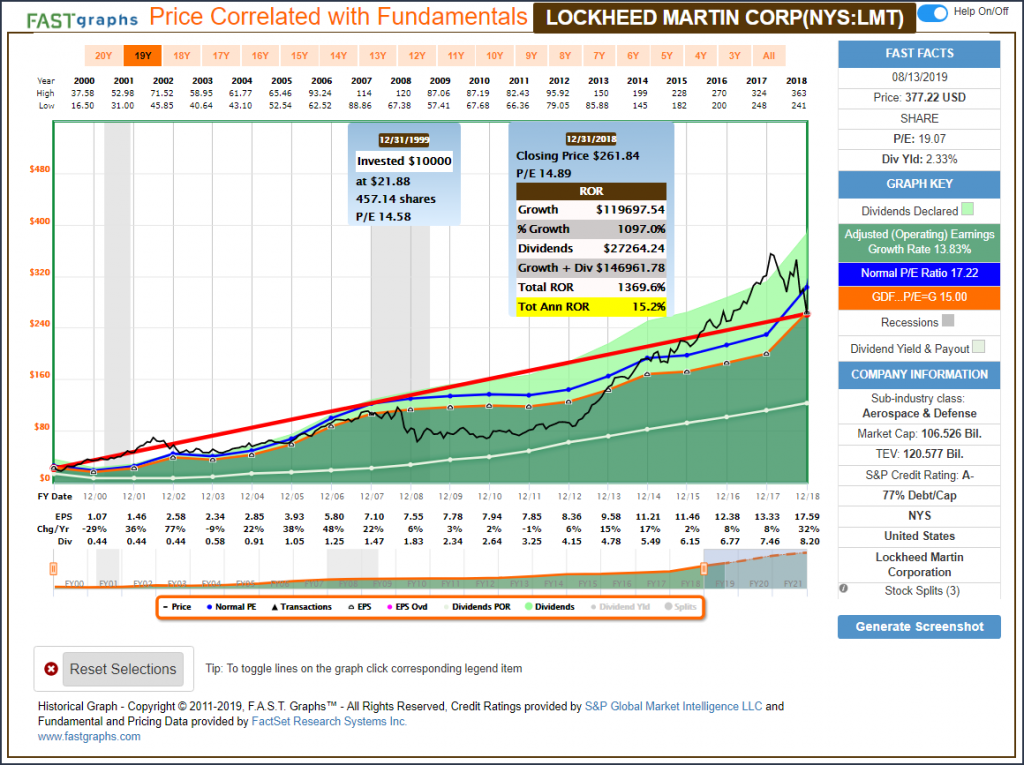

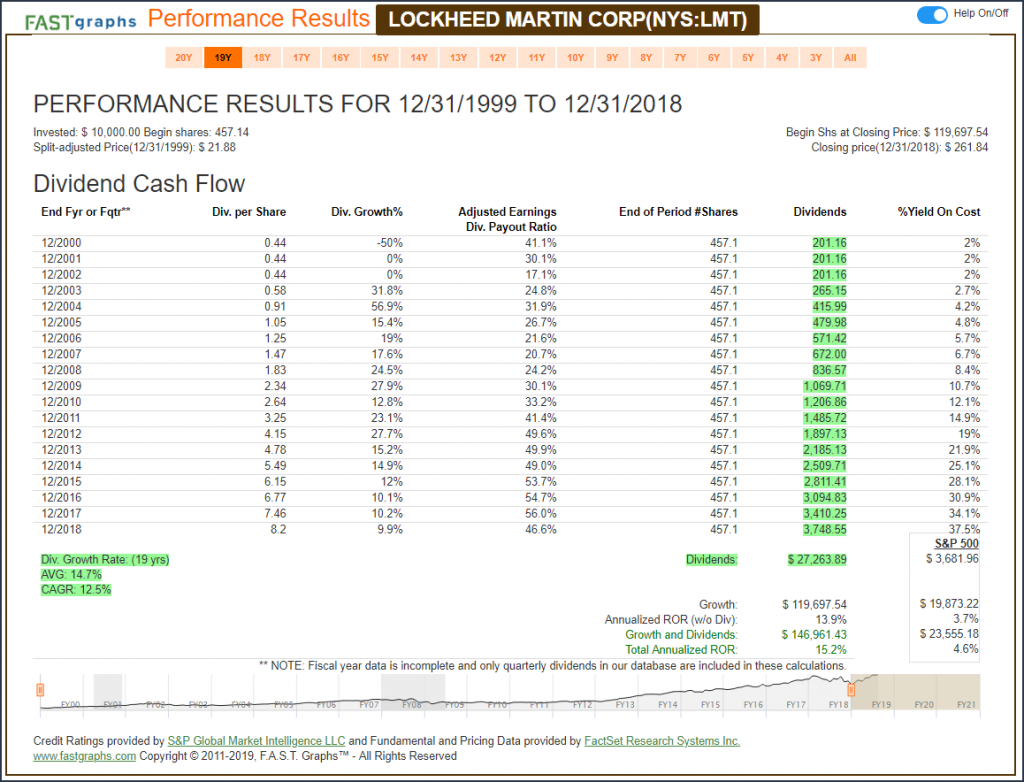

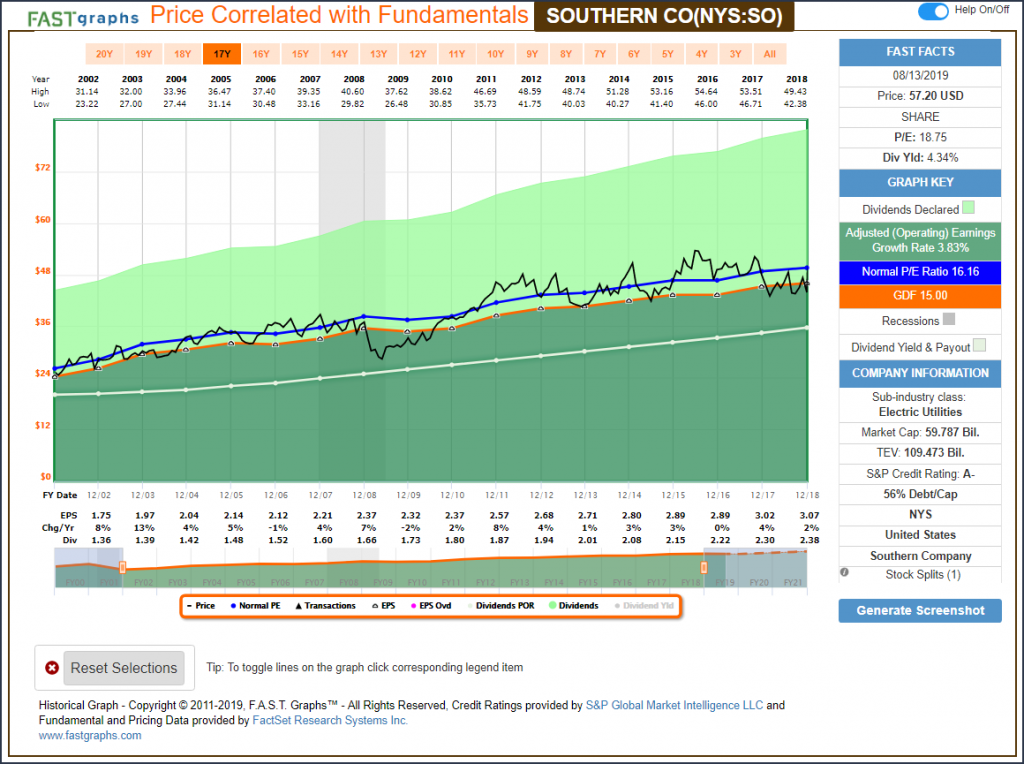

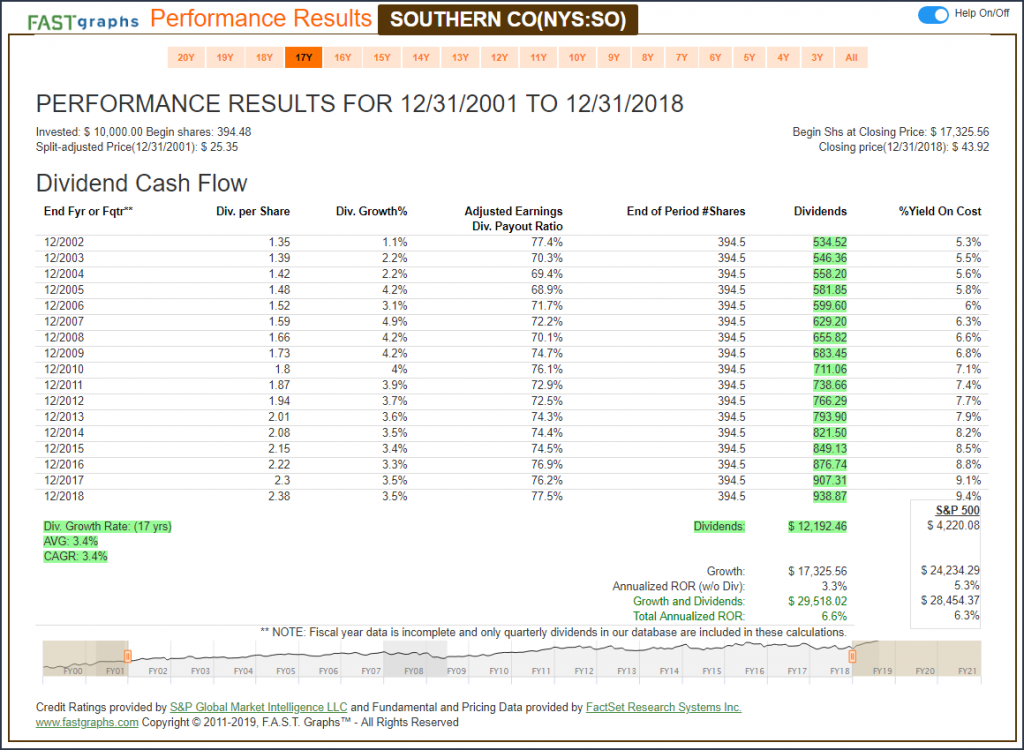

Below, I present 4 historical examples that clearly illustrate the principles presented above. Each example was calibrated so that they can be measured on a fair valuation to fair valuation (apples to apples) basis. Importantly, I would ask that the reader notice that the first 3 examples all are presented at the same fair value P/E ratio of 15 (The relevance of the 15 P/E ratio will be elaborated upon in Part 2).

However, the reader should also note that even though they all had the same initial fair valuation calculation (starting P/E ratio 15), each of them provided shareholders significantly different levels of capital appreciation, total cumulative dividend income and ultimately different total annualized rates of return. This is a key and important message that this article is attempting to portray.

Lockheed Martin Corp. (LMT): Above-Average Growth

Southern Company (SO): Low Growth

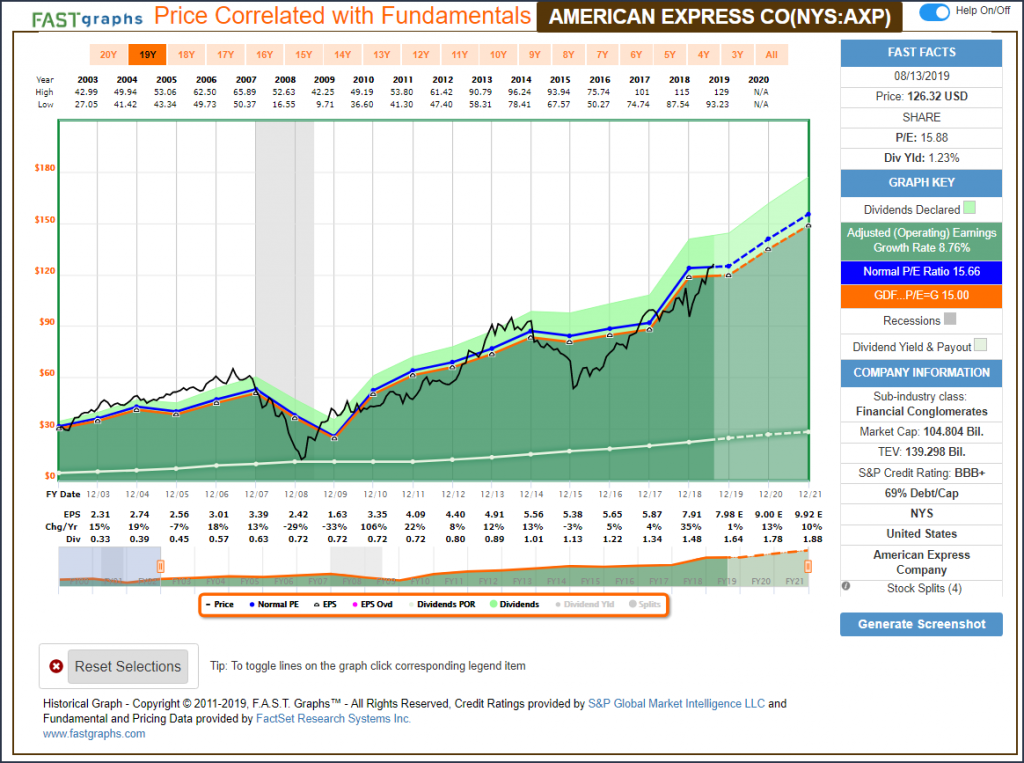

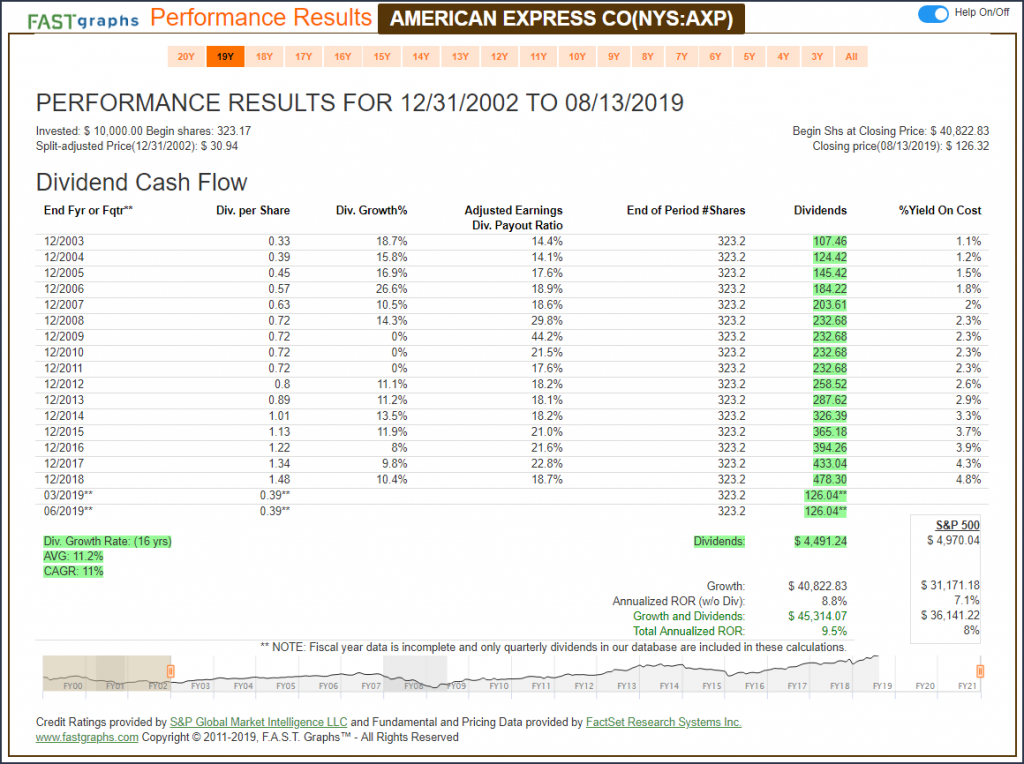

American Express (AXP): Average Growth

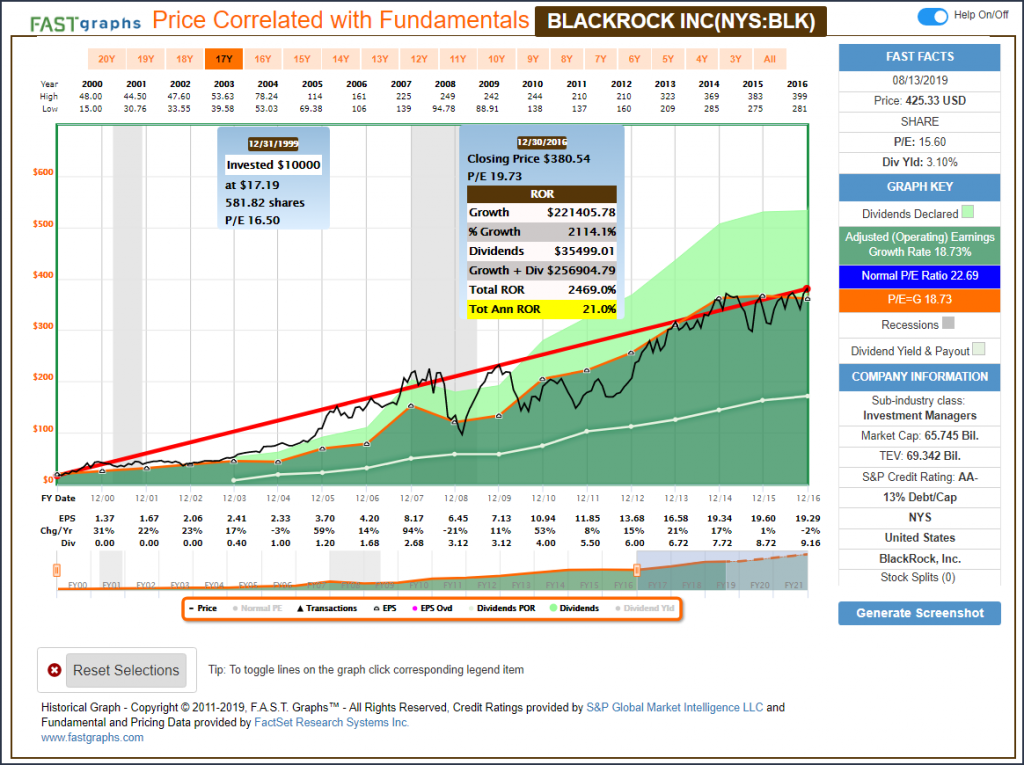

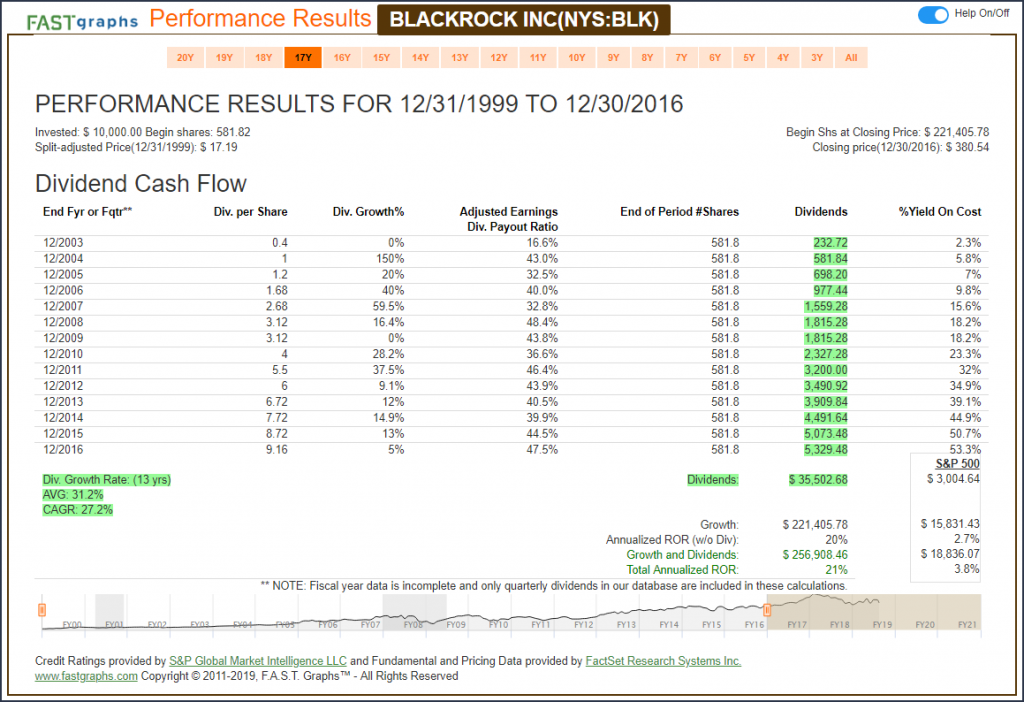

BlackRock Inc. (BLK): High Growth

FAST Graphs Analyze Out Loud Video:

Although the above examples provide insights into the importance of valuation, the following video will provide a greater understanding of the nuances of valuation.

Summary and Conclusions

With this article, I have primarily covered the principles of valuation and earnings growth working in conjunction to generate reasonable and achievable rates of return at controlled levels of risk. My primary objective was to illustrate the importance of fundamental valuation as a measurement of soundness and risk control. Additionally, although attractive fundamental valuation will contribute to total return, it is not a guarantee of high returns.

However, sound valuation in conjunction with the future operating performance that the stock you invest in achieves will be the key factors that generate long-term results. Whether they end up being high, average or below average will be a direct result of how well the business performs. To me this is a quintessential understanding of the prudence and importance of focusing on valuation.

Therefore, the important takeaway is that if you find or discover a business that you truly believe in, and where you admire the management, you want to be sure that you put yourself into a position to participate fully in all that the business offers you. If you overpay, you will get less than the business produces, but if you are lucky enough to find a bargain, you will gain more than the business produces. At the end of the day, investing at sound valuation is about prudence and common sense.

Although I provided some initial clues in the above video with this article, I will be elaborating more fully on why a current fair value P/E ratio of 15 applies to most companies. In part 2, I will be more fully discussing the relevance of the 15 P/E ratio as a fair valuation standard and as a function of the earnings yield it represents.

Disclosure: Long SO.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.