Introduction

For some time now I have been pointing out that the stock market as measured by the S&P 500 has become moderately overvalued. However, even more to the point, I still believe that to be true even after the price corrections we have experienced recently as a result of the coronavirus. In other words, I believe that stocks remain expensive, and therefore, might represent poor long-term returns going forward.

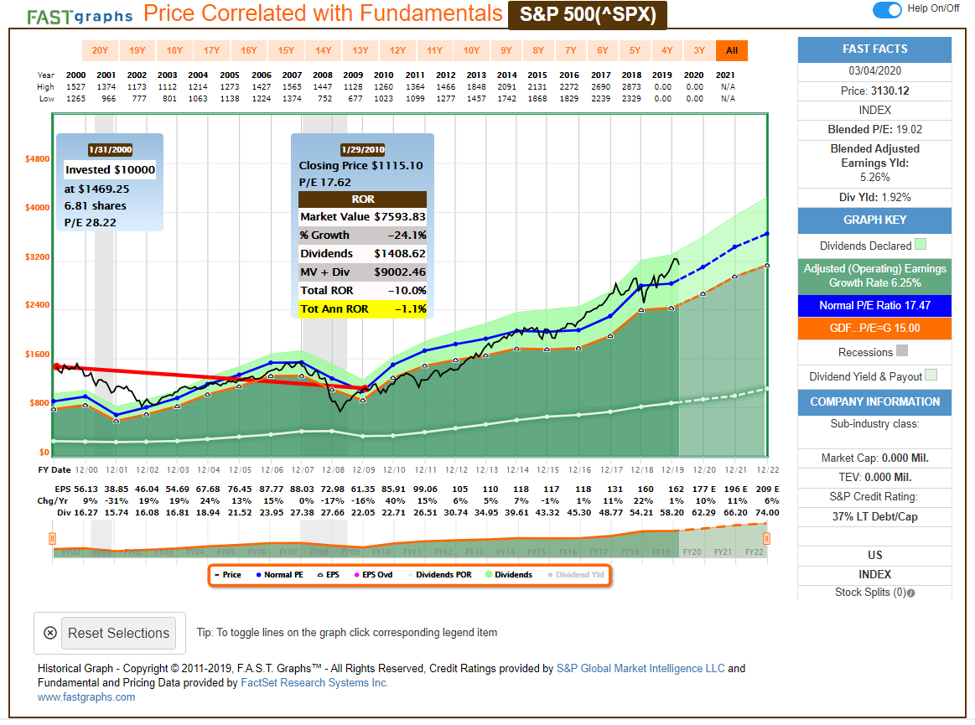

The following earnings and price correlated FAST Graph of the S&P 500 illustrates the veracity of my above statements. The orange valuation reference line on the graph is drawn as a 15 P/E ratio. The dark blue line is drawn as a normal P/E ratio valuation reference line is a 17.47 P/E ratio. As you can see, the market has commonly traded between those two valuation reference lines since calendar year 2000. However, you can also see that the market was overvalued in 2000 where the price was significantly above both valuation reference lines.

As a result, the S&P 500 from a performance perspective resulted in what has been called the lost decade. From January 31, 2000 through January 29, 2010 the total annualized rate of return of the S&P 500 was a -1.1%, and that includes dividends. Although this timeframe also includes both the recession of 2001 and what I call the Great Recession of 2008 – 2009, it should be clear that excessively high valuation was the main cause of poor market performance over this timeframe.

As depicted in the pop-up on the below graph, note the P/E ratio of the S&P 500 was 28.22 on January 31, 2000. As you can see in the FAST FACTS to the right of the graph, the current blended P/E ratio of the S&P 500 is 19.02. Although this is not as high as the market’s valuation we saw in 2000, it is still higher than the historical norm. On the other hand, and to be fair, today’s low interest rates might partially mitigate some of that risk considering that the current dividend yield of the S&P 500 is currently higher than the interest available from a 10 year treasury.

The S&P 500: It’s A Market Of Stocks

Although the S&P 500 is moderately overvalued in the general sense, there are some constituents that are excessively overvalued and some that are undervalued. I think it’s important to recognize that it is a market of stocks and therefore, not all stocks should be looked at the same. Later in the video portion of this article, I will show examples of some excessively overvalued S&P 500 stocks, as well as some that are very inexpensive today.

The S&P Dividend Aristocrats Still Mostly Overvalued

From the perspective of the dividend growth investor, today’s market levels are very challenging. The crème de la crème of dividend growth stocks could be considered the S&P Dividend Aristocrats list. However, with interest rates as low as they currently are, high-quality dividend paying stocks have become overly competitive with fixed income instruments. As a result, demand for quality dividend stocks has driven valuations to extreme highs for most of the best-of-breed dividend growth stocks. I will also provide examples later in the video of just how expensive the Dividend Aristocrats currently are. However, I will also highlight a few that are undervalued as well.

Summary and Conclusions

What I hope the reader gleaned from this article is the undeniable reality that even in the midst of the recent market correction, valuations are still high in the general sense. When valuations are high, investors take on more risk in order to achieve the potential for lower long-term rates of return. On the other hand, regardless of the overall market, there is always value to be found. Choose carefully!

Disclosure: No position.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.