Introduction

Legendary investor and mentor to many investing greats Benjamin Graham once aptly stated that: “investing is most intelligent when it is most businesslike.” Personally, I agree which is why I refer to what I personally adhere to and practice with my own investing as “business perspective investing.” Stated more directly, I do not believe in speculating in markets by attempting to guess (forecast) where stock prices may or may not go in the short run. Instead, I prefer positioning myself as a long-term oriented shareholder/owner of terrific businesses that I plan to be involved in (own) for many years to come.

Consequently, my personal approach might best be described as a long-term buy-and-hold strategy. Additionally, I believe in building common stock portfolios one company at a time with the primary objective of investing in high-quality at sound or attractive valuations. Since I personally prefer not to utilize index funds or what I call package products (mutual funds, ETF’s, CEF’s annuities, etc.) I am often automatically thrown into the active investor camp in contrast to the passive investor camp.

However, I do not consider investing in an index as passive, nor do I consider building your own portfolio as active. To my way of thinking, active versus passive would indicate the amount of trading that is done within a portfolio. With that said, I do believe it making changes to my portfolios from time to time if necessity dictates. On the other hand, I try to do this as little as possible on the notion that, as Warren Buffett once said: “inactivity strikes us as intelligent behavior.”

Furthermore, I do not consider investing in an index as necessarily passive. An index, just like my own personal portfolio, will from time to time add and subtract companies. Consequently, there is a level of activity within the various indices as well. Nevertheless, the primary reason I choose not to utilize so-called passive investments like an index is because as many regular readers would attest, I am extremely fastidious with valuation. With that said, I cannot bring myself to buy an index because I recognize that there will likely be many businesses within that index that are overvalued at any given point in time.

This leads me to a clarification regarding the title of this article. To clearly understand what I’m suggesting requires adding an additional qualifier to the original title. Instead of simply stating “Passive and Buy-And-Hold Investing Don’t Work Unless!”, I would add the qualifier – unless valuations are in alignment at time of purchase. This supports one of the guiding principles that I have long followed that states: “you make your money on the buy side.” I will be elaborating on this point later in the article.

Why Buy and Hold Will Always Be a Sound Investing Strategy

As an aside, it seems like the debate regarding the merits of the “buy-and-hold” investing strategy is alive and well. I always find these discussions amusing, because I believe that it is such a pointless discussion. In my humble opinion, there is no universal argument or case that can be made to support the buy-and-hold strategy or to negate it.

The only true answer to the buy-and-hold argument is it depends on what and/or when you buy-and-hold. If you buy the right company at the right price, then buy-and-hold is a great strategy. If you buy the wrong company at any price, then the buy-and-hold strategy is a dumb move. Also, if you buy the right company at the wrong price, then buy-and-hold would once again be a bad move.

General Considerations

For example, after the market crash of 2008 it seemed like buy-and-hold bashers came out of the woodwork. These nonbelievers were gleefully pointing to the so-called lost decade to validate their thesis that buy-and-hold was a dumb move. In this era of day trading mania where investors are more inclined to own a common stock for mere minutes rather than years, many pundits and investors alike jumped on the anti-buy-and-hold bandwagon.

One critical point that I want to clearly establish is that buy-and-hold is an investing strategy. Investing strategies, by definition, imply a long holding period. Speculation, on the other hand, implies shorter timeframes where the speculator is attempting to exploit an arbitrage situation. My point is not to debate the virtues of one over the other, my desire is to point out that investing and speculating are not the same thing.

As an investing strategy, there is an “old” adage that supports the virtue of being a buy-and-hold investor: “a portfolio is like a bar of soap, the more you handle it the smaller it gets.” The true investor is looking for a place where they can allocate their capital in order to receive an attractive return on their capital at appropriate levels of risk. The higher the return they attempt to achieve, the higher the risk they’re willing to take, and vice versa.

Another general comment to be made about buy-and-hold as an investment strategy refers to investors who are looking to generate income from their investments. Income investors have the option of either fixed income, i.e., bonds, annuities and CDs, etc.; or income producing equities, i.e., real estate, dividend paying common stocks, etc. Of course, they can invest in these asset classes separately or in packages like mutual funds, MLPs, REITS or ETFs, etc. These investments need to be owned for long periods of time if any meaningful harvesting of interest or dividends is to occur.

The many faces of buy-and-hold

With the remainder of this article I will look at situations where buy-and-hold is a great strategy as well as situations where it’s not. For the sake of efficiency, I will present these discussions in graphic form through the lens of the FAST Graphs research tool.

Overvaluation caused the lost decade

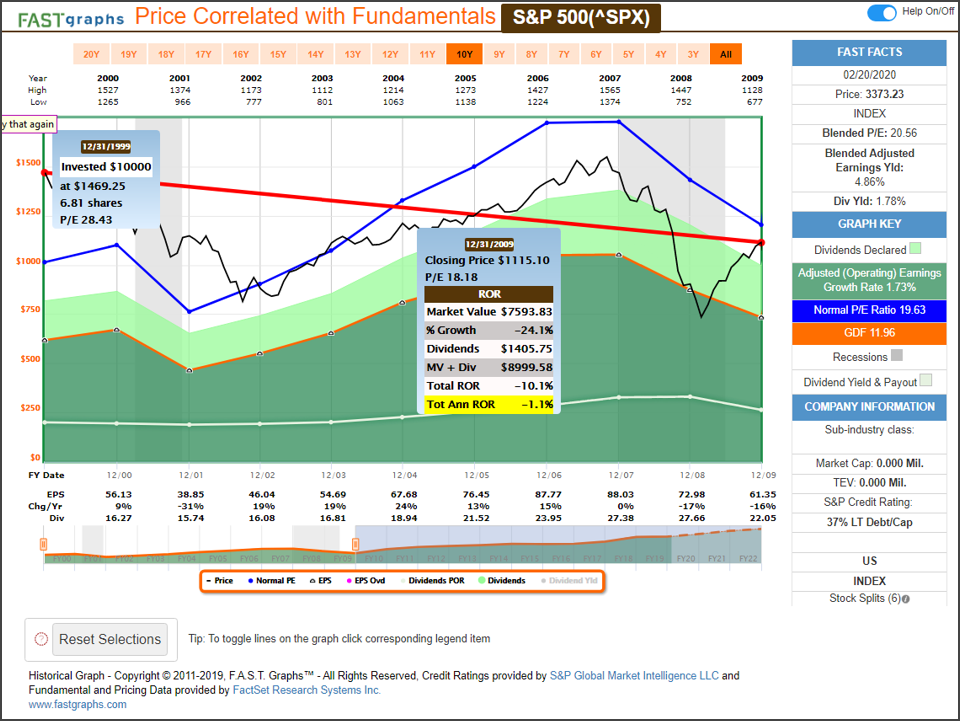

The following FAST Graphs on the S&P 500 show the importance of valuation regarding a buy-and-hold strategy. The first graph plots the S&P 500 stock price correlated to earnings for the period calendar year 2000 through 2009 and the corresponding performance over this timeframe. There are two important takeaways from this graph: 1. Earnings growth for the S&P 500 over this time period was exceptionally low at 1.73% per annum. 2. For the initial starting/year (ending December 31, 1999), the P/E ratio of 28.43 is at a premium relative to the historical fair value reference S&P 500 P/E ratio of 15 indicating excessive overvaluation.

Therefore, it should be clear that the so-called “lost decade” spanning calendar year 2000 through 2009 resulted from the combination of excessive starting valuation coupled with virtually no growth. As a result, investors foolish enough to invest in an S&P 500 index fund at the excessive valuation at the beginning of calendar year 2000 would have seen 10 consecutive years of negative returns (-1.1%) and this included dividend income. In other words, passive investing only works if prudent investors focus on sound valuation and growth potential in the same manner they would when choosing an individual stock.

Not only was buy-and-hold a very poor investment strategy over this timeframe, it should have also been obvious to investors that the market entered calendar year 2000 significantly overvalued. Clearly, both buy-and-hold and passive investing as investing strategies over this timeframe was – as previously stated – a dumb move. But even more importantly, it would have been obvious to value investors that this was a bad time to be investing in the index and an even worse time to be a buy-and-hold investor.

When growth and value are aligned

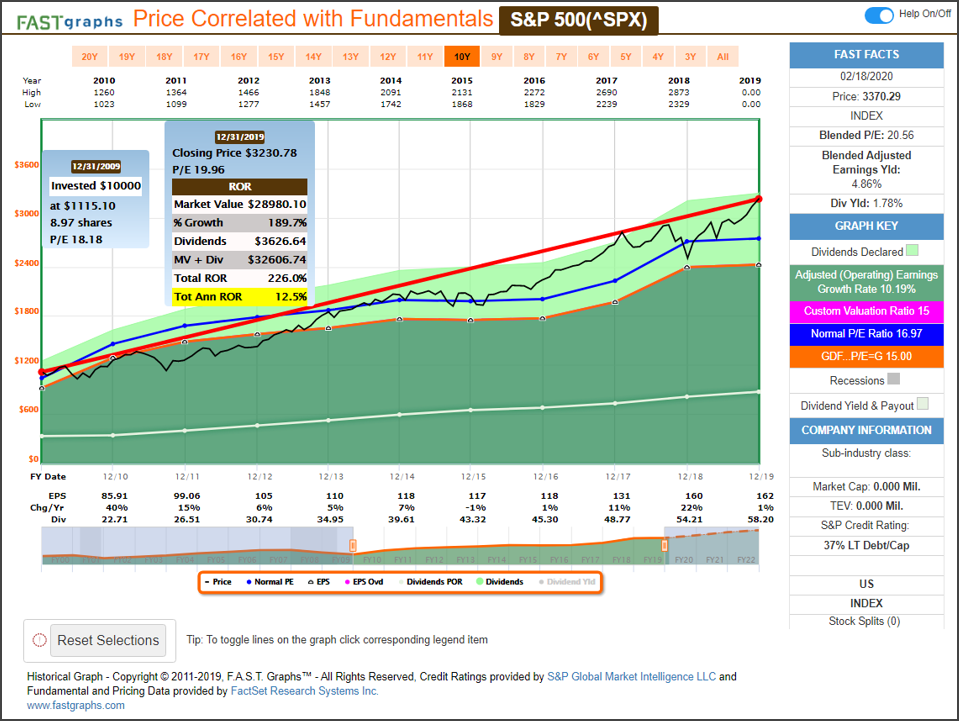

This next graph illustrates the benefit of applying a buy-and-hold strategy to the index when growth and value are aligned. The adjusted operating earnings growth for the S&P 500 over the 10 year timeframe 2010 through 2019 was 10.19%. Moreover, the beginning valuation was moderately high at a P/E ratio of 18.18, however, the ending valuation offered P/E expansion to a P/E ratio of 19.96 by December 31, 2019. Therefore, the result was a total annualized rate of return of 12.5% including dividends paid but not reinvested. Clearly, this illustrates that buy-and-hold was a successful strategy even though beginning valuation was a little high but not excessive as we saw in the first example.

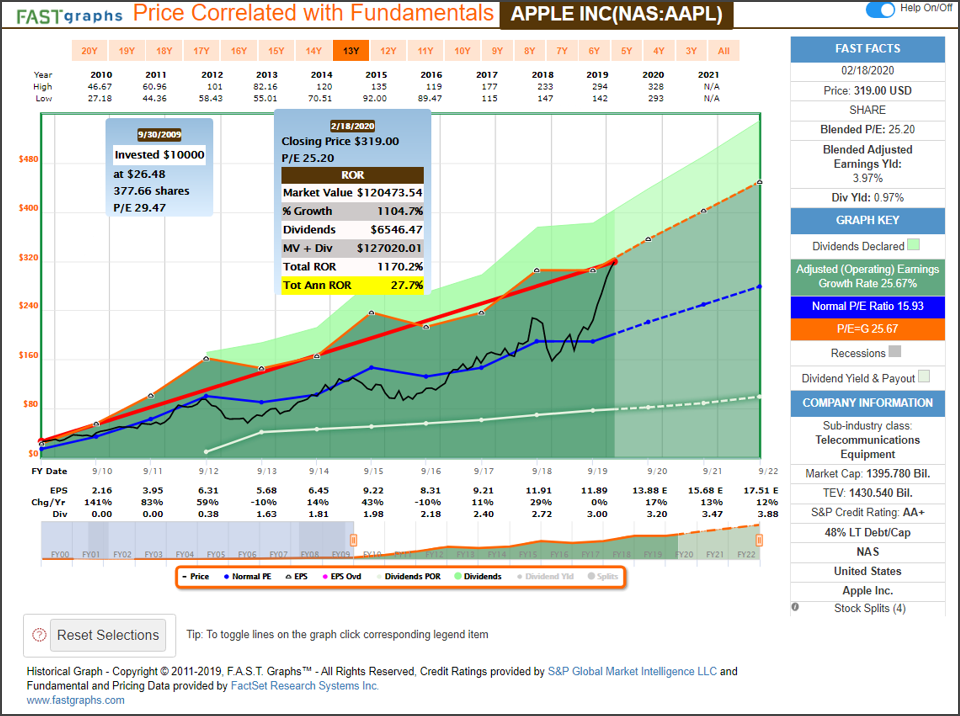

The next series of graphs portrays three companies over the timeframe 1999 to current, that illustrate how effective a strategy buy-and-hold can be. At varying degrees, each of these companies possess extremely consistent and strong earnings growth, and each was reasonably valued at the beginning date of this time period. Our first choice, Apple Inc. (AAPL), provides an example of a pure growth stock that morphed into a strong dividend growth stock.

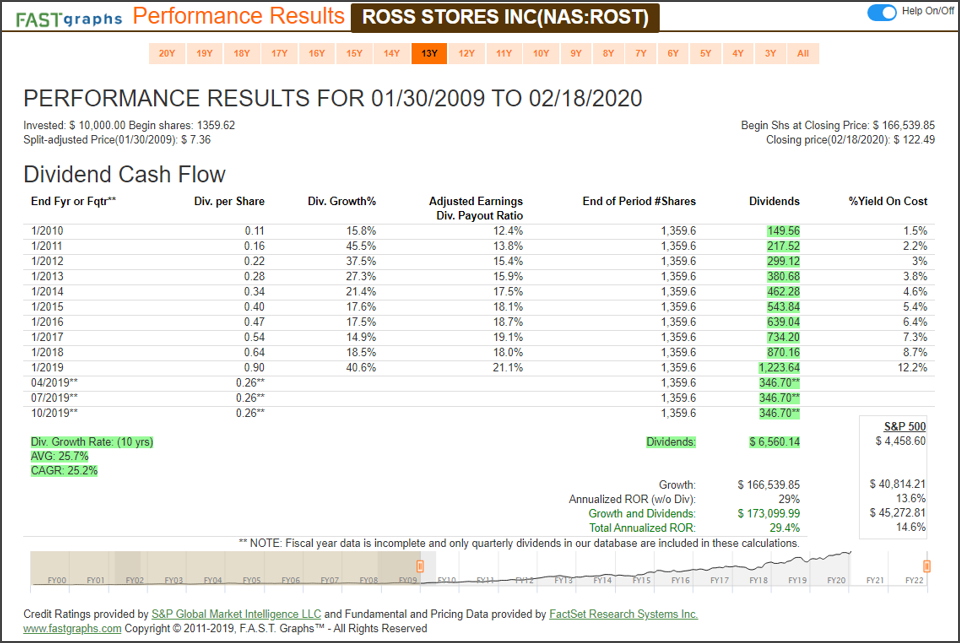

My second choice, Ross Stores (ROST), provides an example of a growth stock with a dividend component. Note that I calculated performance from my starting date to my fair value reference line (the orange line) on the graph. However, Ross Stores, as good as performance would have been had the stock only traded at fair value, it was even better as a result of it currently being overvalued as illustrated in the performance graph that followed.

My third and final choice, Ameriprise Financial Inc. (AMP) provides an example of a dividend growth stock where valuation was attractive at the beginning and undervalued at the end of the timeframe. Nevertheless, despite its low ending valuation buy-and-hold turned out to be a great investment strategy for shareholders in Ameriprise Financial Inc. This once again illustrates how powerful buy-and-hold as an investment strategy is when valuation and growth are both aligned.

Each of these examples provide undeniable evidence that a buy-and-hold investing strategy works extremely well when the right companies are originally purchased at the right valuations. I offer this as compelling evidence that the buy-and-hold strategy, done right, is a great and prudent way for people to invest.

When Buy-And-Hold Is A Bad Idea

However, with the following examples I illustrate when buy-and-hold is a bad idea. The primary point is that you can’t simply make a general or universal statement that buy-and-hold is an effective strategy or not. The truth always depends on valuation and the success (growth) of the investment purchased.

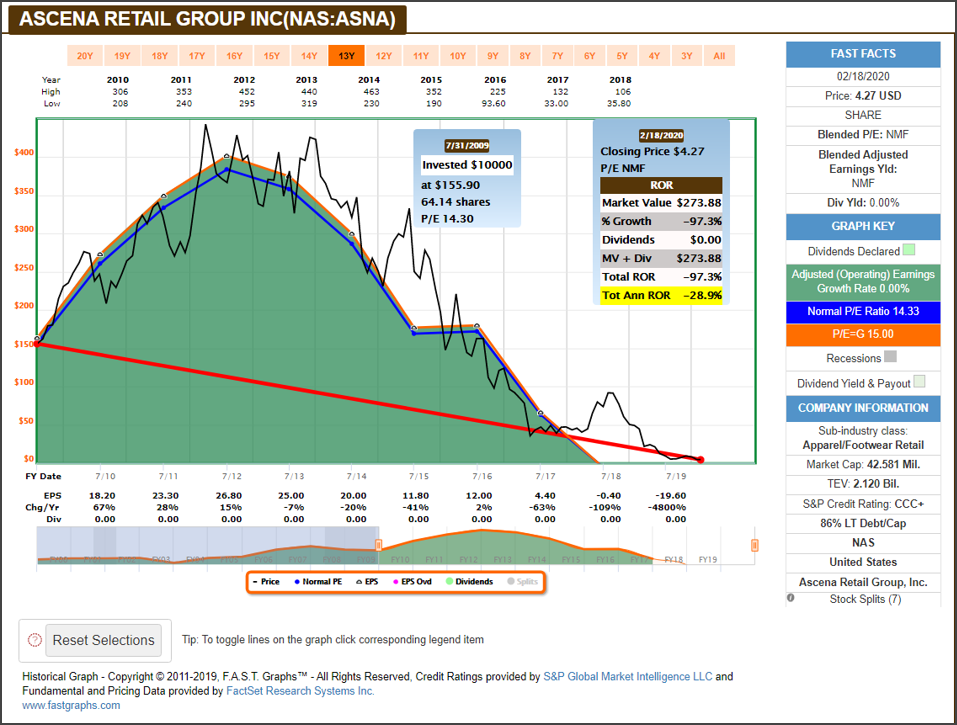

Ascena Retail Group (ASNA)

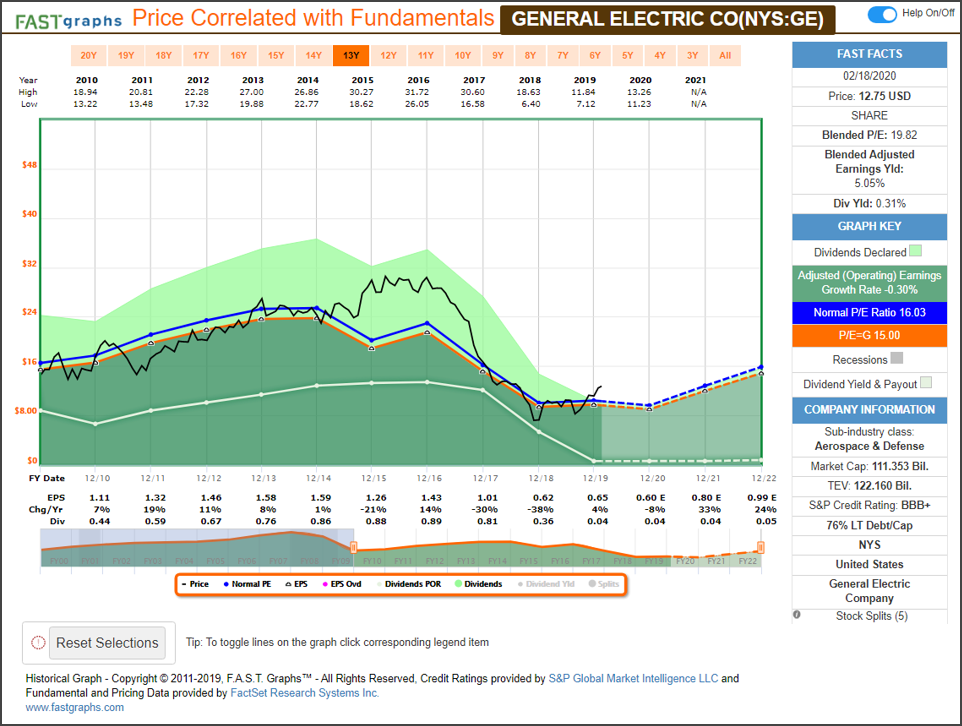

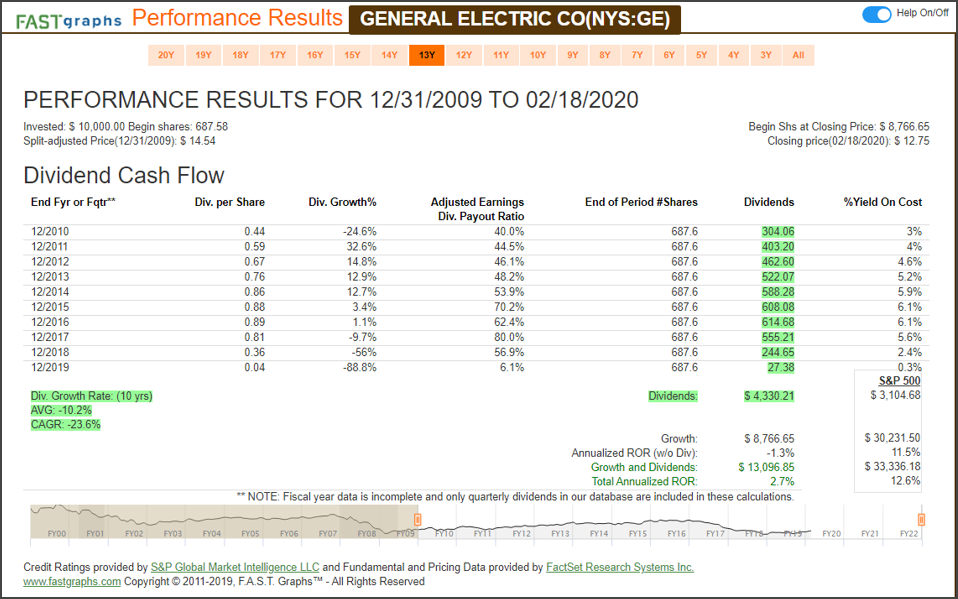

General Electric (GE) Earnings and Price Correlated Graph Followed With Performance

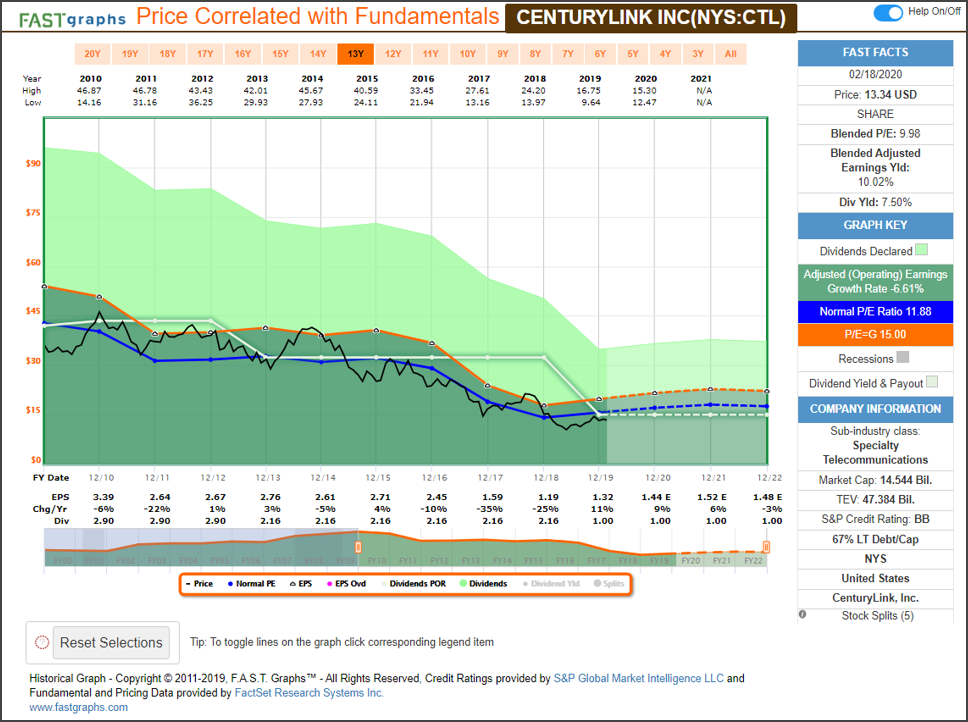

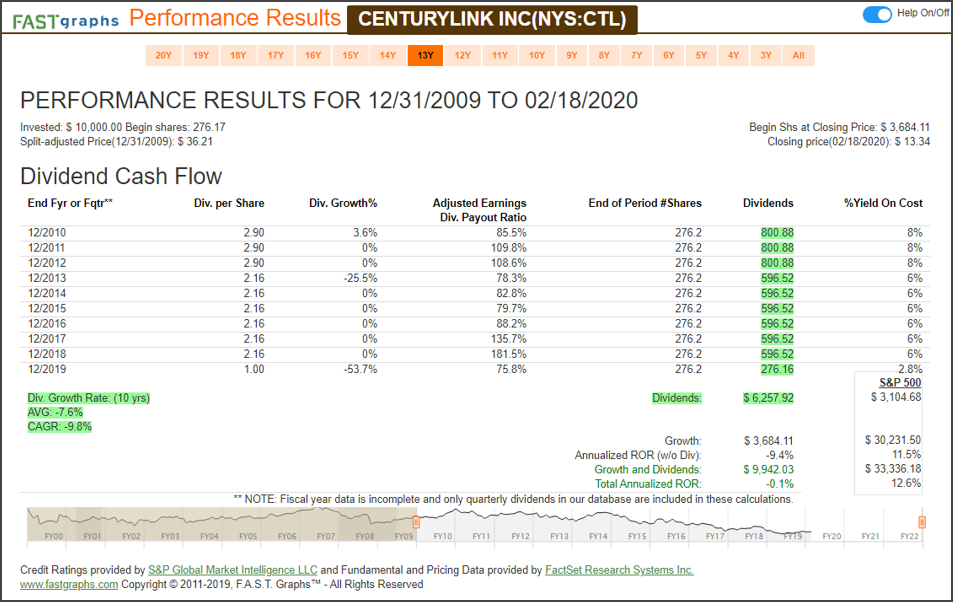

CenturyLink Inc. (CTL) Earnings and Price Correlated Graph Followed With Performance

The following FAST Graphs Analyze Out Loud Video elaborates on the points expressed in this article:

Conclusions

The main premise behind this article was to illustrate how the general arguments regarding whether buy-and-hold is a good strategy or not are frankly ridiculous. The validity of buy-and-hold as a sound investing strategy is predicated on many factors. Some of the primary ones are what you buy-and-hold and the price at which you buy-and-hold it at. As the examples above illustrate, you can’t just buy-and-hold anything, furthermore, you can’t just buy it at any price either. For buy-and-hold to truly be an effective strategy, it must be done right. However, when done right it is a terrific way for people to invest their capital.

A secondary premise behind this article was to illustrate the profound and fundamental difference between true investing and speculating. Buy-and-hold is an investing strategy that implies the appropriate holding time period, which is a hallmark of any strategy called investing. Speculation on the other hand is usually associated with shorter timeframes where some element of arbitrage is applied. Whether speculators will admit it or not, there is more risk associated with this tactic than there is with sound fundamental investing practices like buy-and-hold.

The final premise behind this article was to further illustrate that passive investing (index investing) is also an investing strategy that can be good or bad – depending. Consequently, it really comes down to what suits the individual investor. Do they prefer taking charge of their own investment portfolios or are they more comfortable leaving it to professional managers like those that build index ETF’s and mutual funds. Nevertheless, there are good times and bad times to invest in indices as well.

At the end of the day, the practical application of a well thought-out and disciplined buy-and-hold strategy has proven itself and really needs no defense. In the long run, buy-and-hold will be more tax efficient and less costly than more active strategies. This is not to say that more active strategies can’t be profitable, it simply means that they’re more difficult, costly and riskier to execute effectively. However, if you do build your own portfolio and practice a buy-and-hold long-term strategy, that does not simultaneously make you an active investor. Nor as described earlier does investing in an index necessarily mean that your investments are passive.

Disclosure: Long AAPL,AMP

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.