Introduction

This is a follow-up to my first article in a continuing series where I will be identifying and presenting dividend growth stocks for an above-average long-term total return objective. My first article in this series covered AmerisourceBergen, a leading medical distributor that I presented as significantly undervalued. However, I offer this follow-up to illustrate that the entire sector and subsector is currently out-of-favor and undervalued. Consequently, this represents a case that is more sector-related than company-specific.

Most importantly, the primary issues causing concern throughout this sector are politically related. There are also concerns about lawsuits related to the opium epidemic. However, these issues are based on fears about things that might happen but have not yet happened. Consequently, the future fundamentals for each of these companies are currently expected to remain positive going forward. As a result, and based on those fundamental future expectations, the stocks would be considered extremely cheap offering above-average upside. Therefore, as long as earnings do in fact continue to manifest, that would be a true statement.

On the other hand, if the future does bring significant health care reform to include limits and restrictions on pharmaceutical prices, the future earnings and cash flows of these companies could change negatively. Therefore, prospective investors should be aware of these risks but at the same time recognize that these risks may already be priced in. Nevertheless, it’s up to each individual investor to decide for themselves whether they are willing to take that risk or not.

Sources of Long-Term Return

Throughout this series, I will be illustrating that there are several prudent sources of long-term return and there is also luck or chance. Personally, I suggest that investors strive to build their portfolios based on prudent fundamental realities and not simply invest with the hope that your stocks will rise.

The primary prudent sources of total return that I am alluding to are, first and foremost, sound fundamental valuation – although attractive undervaluation is even more desirable. The second primary source would be growth defined as the potential long-term rate of change of earnings and/or cash flow growth and dividend growth. When you invest at sound valuation, you position yourself to participate in the growth that the business generates on your behalf.

If you can identify attractive undervaluation, you can expect a secondary source and a potential kicker to total return that I like to call natural leverage. Simply stated, in addition to the operating growth and dividend growth that the company achieves, you are also positioned to get P/E ratio expansion. To clarify, you initially invest in a smaller level of earnings at a lower P/E ratio where the company, over time, delivers a higher level of future earnings that the market capitalizes at a higher P/E ratio. I metaphorically refer to this as a double-double. In the future, you get double the earnings that are valued at double the P/E ratio. Of course, the math does not always work out so perfectly, but I hope you get the point.

Furthermore, I will be presenting stocks that I believe offer the potential for significantly above-average total return. Stated more clearly, I will be looking for dividend growth stocks that I believe can provide double-digit total returns, including a growing dividend income stream. But perhaps most importantly, because of the focus on attractive valuation, I believe these future returns can be generated at greatly mitigated (lower) levels of long-term risk.

Moreover, it’s important to distinguish between long-term results versus short-term results. Intelligent value investors understand that investing in unpopular securities is where value is most often found. This is especially true when you are in a bull market like we have been in for the last several years.

Consequently, there are typically reasons why a stock’s valuation is low. The trick is in determining whether those reasons are valid, permanent or temporary. Nevertheless, the intelligent value investor understands that unpopular stocks can remain unpopular for some time, and therefore provide below-average short-term results. On the other hand, unpopular stocks that are erroneously valued can provide exceptional long-term returns based on the sources of long-term return described above. But most importantly, if the stocks in question are truly undervalued, then the exceptional long-term returns are also achieved at significantly mitigated levels of risk. Low risk and high return equals investor nirvana.

Medical Distributors and Drugstore Chains: Low Multiples of Earnings And Cash Flows

The following summary illustrates the low multiples of earnings and cash flows that these medical distributors and drugstore chains can currently be purchased at. Additionally, note that these low multiples translate into high levels of earnings and cash flow yields (the inverse of P/E ratios and price to cash flow ratios).

FAST Graphs Screenshots of the 4 Research Candidates with Performance Calculation Estimates

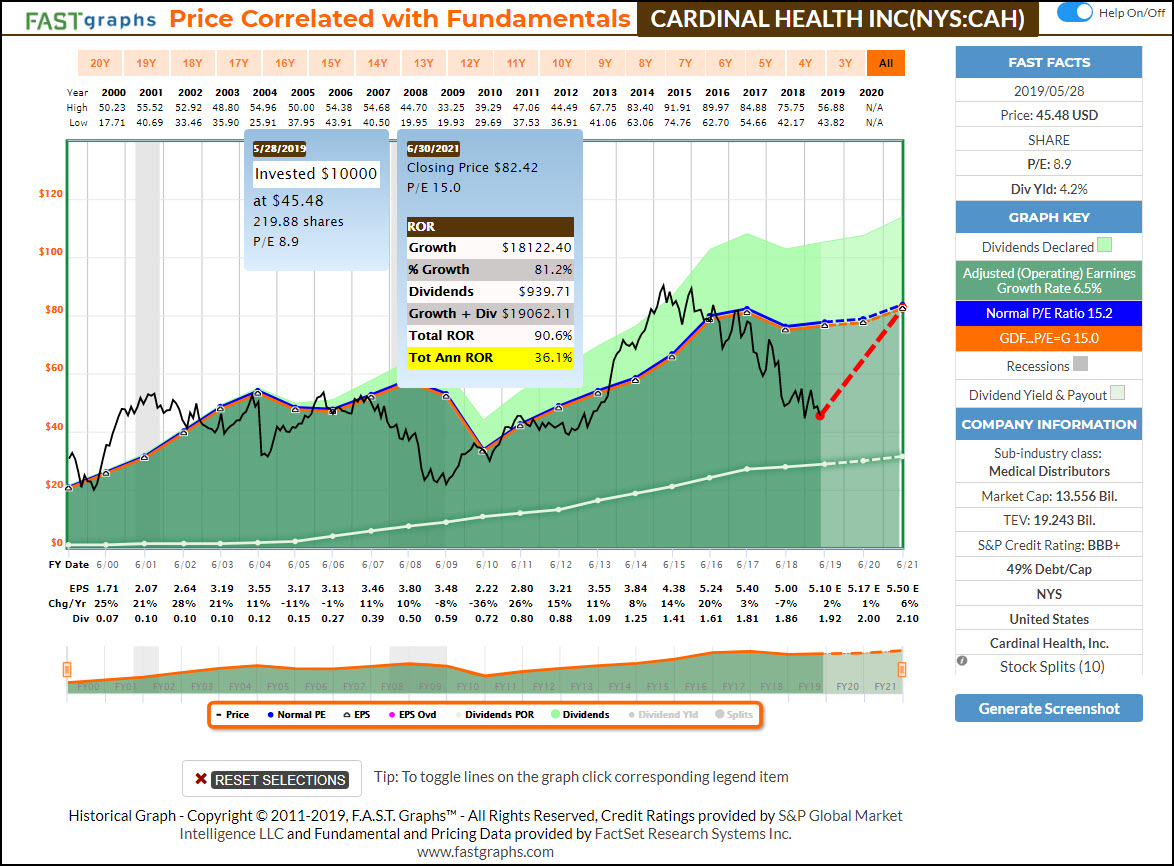

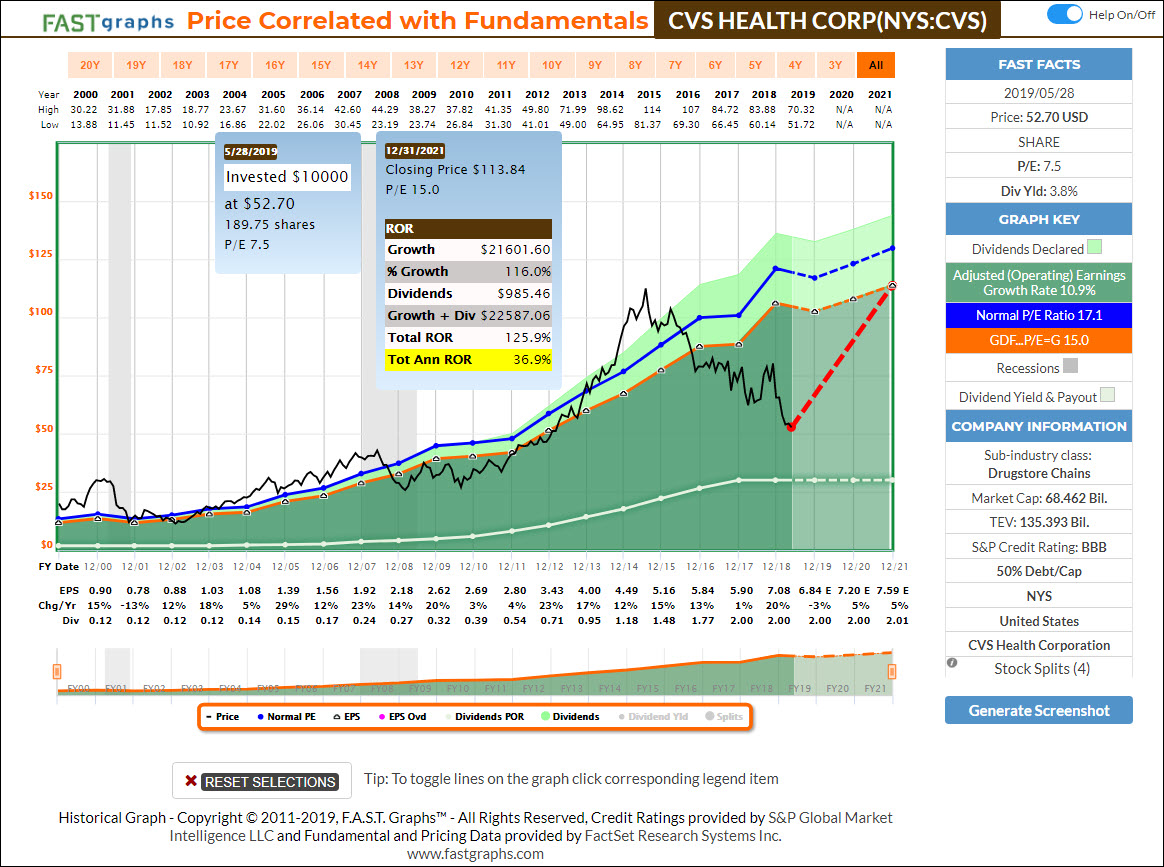

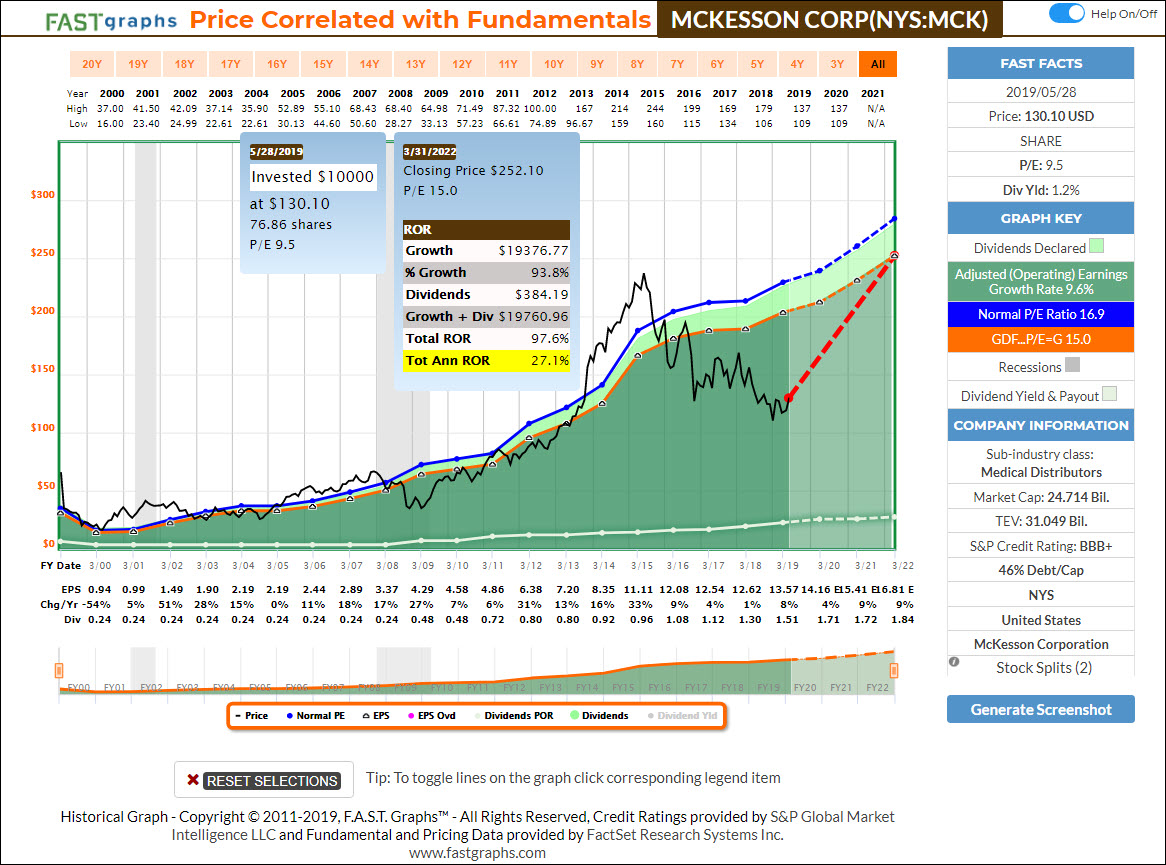

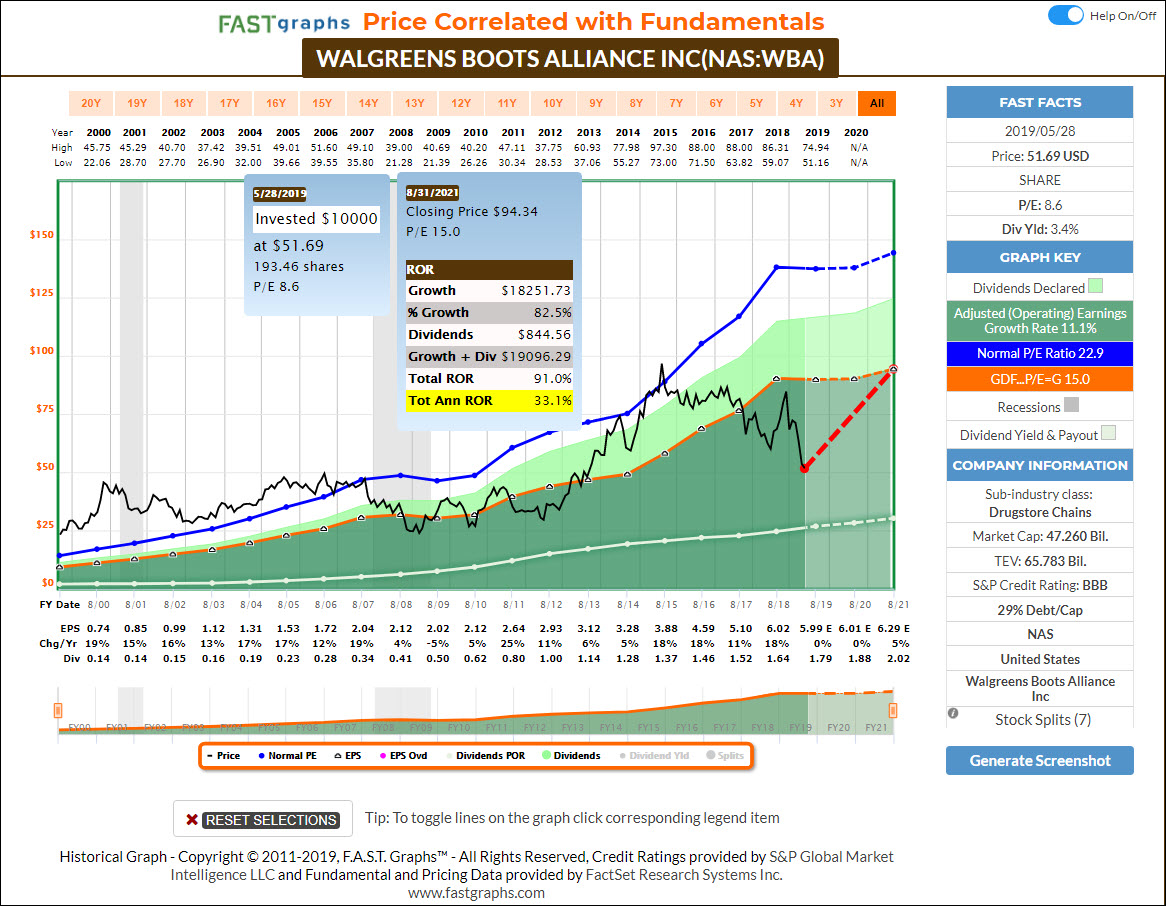

The following long-term earnings and price correlated FAST Graphs tell several important stories about each of the four medical distributors and/or drug chains. First notice the long-term relationship and high correlation between the companies’ adjusted operating earnings (the orange line on the graph) and its monthly closing stock price (the black line on the graph). Price follows earnings, and when it gets disconnected, it inevitably reverts to the mean. Consequently, long-term historical evidence suggests that as long as the orange earnings line continues to advance as forecast, that stock price should logically revert to the mean. Utilizing the calculator function, I provided the estimated total annualized rate of return (Tot Ann ROR) on each of the companies. (Note: that these returns are a result of the sources of long-term return discussed above.)

Cardinal Health Inc (CAH)

CVS Health Corp (CVS)

McKesson Corp (MCK)

Walgreens Boots Alliance (WBA)

FAST Graphs Analyze Out Loud Video:

Summary and Conclusions

My primary purpose for presenting this follow-up article to my AmerisourceBergen article is to illustrate that the undervaluation found in these subsectors are industry related. In other words, the concerns relate to issues affecting the entire sector and not specifically related to each of the individual research candidates.

However, and I consider this critically important, the rate of return forecasts presented on the screenshots and in the video are rational and highly likely as long as the earnings (the orange line on the graphs) manifest within reason according to the estimates. The orange line on each of the graphs represents a fair-value 15 P/E ratio. Clearly, the long-term evidence supports the reality that whenever the price deviates from that valuation it inevitably reverts to the mean, and typically very quickly. Consequently, these research candidates do provide extremely attractive long-term rates of return for the prudent value investor. However, continuous monitoring of the political and legal climate threatening these companies is imperative. Caveat emptor.

Disclosure: Long CAH,CVS,MCK,WBA

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.