Introduction

This is the first in a continuing series where I identify and present dividend growth stocks for an above-average long-term total return objective. Throughout this series I will be illustrating that there are several prudent sources of long-term return and there is also luck or chance. Personally, I suggest that investors strive to build their portfolios based on prudent fundamental realities and not simply invest with the hope that your stocks will rise.

The primary prudent sources of total return that I am alluding to are first and foremost sound fundamental valuation – although attractive undervaluation is even more desirable. The second primary source would be growth defined as the potential long-term rate of change of earnings and/or cash flow growth and dividend growth. When you invest at sound valuation, you position yourself to participate in the growth that the business generates on your behalf.

If you can identify attractive undervaluation, you can expect a secondary source and a potential kicker to total return that I like to call natural leverage. Simply stated, in addition to the operating growth and dividend growth that the company achieves, you are also positioned to get P/E ratio expansion. To clarify, you initially invest in a smaller level of earnings at a lower P/E ratio where the company over time delivers a higher level of future earnings that the market capitalizes at a higher P/E ratio. I metaphorically refer to this as a double-double. In the future you get double the earnings that are valued at double the P/E ratio. Of course, the math does not always work out so perfectly, but I hope you get the point.

Furthermore, I will be presenting stocks that I believe offer the potential for significantly above-average total return. Stated more clearly, I will be looking for dividend growth stocks that I believe can provide double-digit total returns including a growing dividend income stream. But perhaps most importantly, because of the focus on attractive valuation, I believe these future returns can be generated at greatly mitigated (lower) levels of long-term risk.

Moreover, it’s important to distinguish between long-term results versus short-term results. Intelligent value investors understand that investing in unpopular securities is where value is most often found. This is especially true when you are in a bull market like we have been in for the last several years.

Consequently, there are typically reasons why a stock’s valuation is low. The trick is in determining whether those reasons are valid, permanent or temporary. Nevertheless, the intelligent value investor understands that unpopular stocks can remain unpopular for some time, and therefore provide below-average short-term results. On the other hand, unpopular stocks that are erroneously valued can provide exceptional long-term returns based on the sources of long-term return described above.

AmerisourceBergen: Prudent Investment-Interesting Speculation

AmerisourceBergen (ABC) could well be the epitome of a near perfect dividend growth stock. It has a long history of consistent above-average earnings growth, and it has increased its dividend for 14 consecutive years at an average rate exceeding 30% per annum. Therefore, even though its current dividend yield is slightly below market average, its growth yield (yield on cost) potential is significantly above average.

Additionally, the company has a solid investment grade A- credit rating and modest debt to capital of 57%. Although the company is not expected to grow at its historical double-digit rates, it is expected to continue growing at the above average rate of 7 to 9%. Nevertheless, trading at a blended P/E ratio below 12 makes this medical distributor a compelling long-term investment based on significant undervaluation alone. Consequently, AmerisourceBergen looks like an attractive dividend growth stock especially for those seeking an above-average long-term total return.

On the other hand, in addition to the company’s apparent long-term attractiveness, it also appears to be a compelling short-term speculation. Walgreens Boots Alliance already owns a 27% stake in this premier drug wholesaler and medical distributor. Moreover, according to Raymond James analyst John Ransom it might also be a potential acquisition target. This seems plausible considering that competitor CVS has recently merged (acquired) with Aetna and the fact that Walgreens Boots Alliance has not engaged in any significant deals recently. Therefore, Walgreens Boots Alliance may have some incentive or need to catch up.

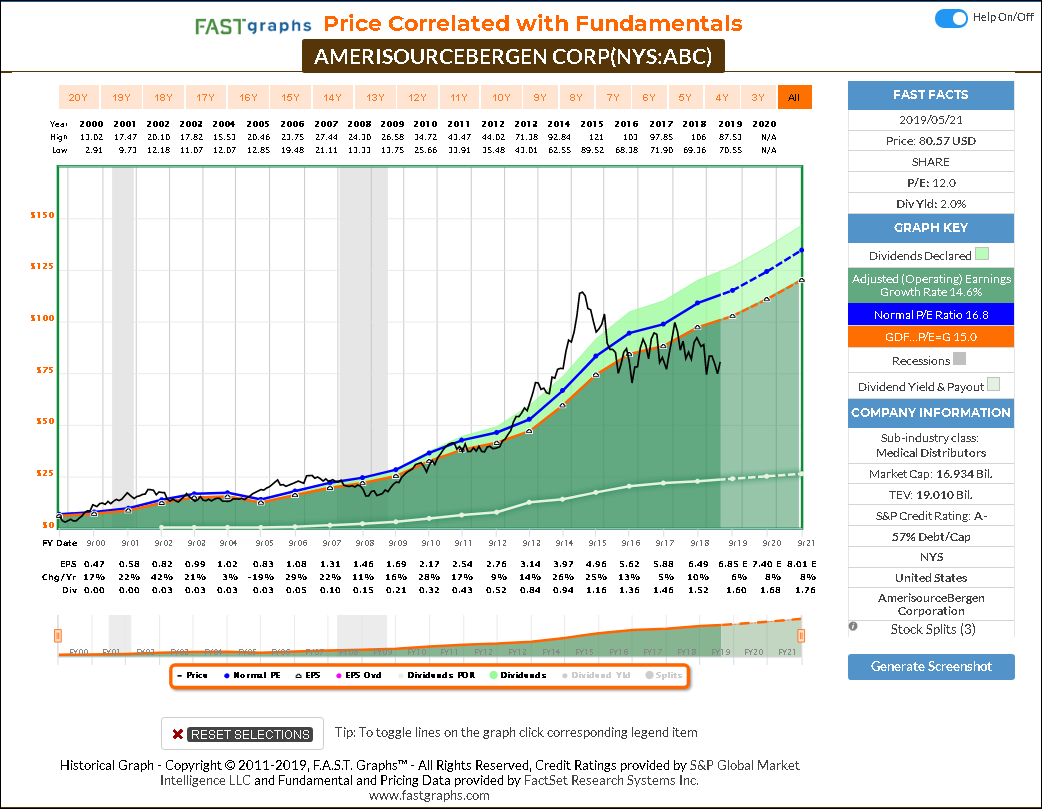

AmerisourceBergen Corp. Compelling Valuation

The following long-term earnings and price correlated FAST Graph on AmerisourceBergen clearly illustrates that the company has not been available at such a compelling valuation since the throes of the Great Recession. This is somewhat understandable considering that healthcare in general is a current political football. However, I believe that investors should also consider that the current political risk is also already priced in. In other words, the current low valuations on healthcare stocks in general appear too attractive to ignore despite the political risks.

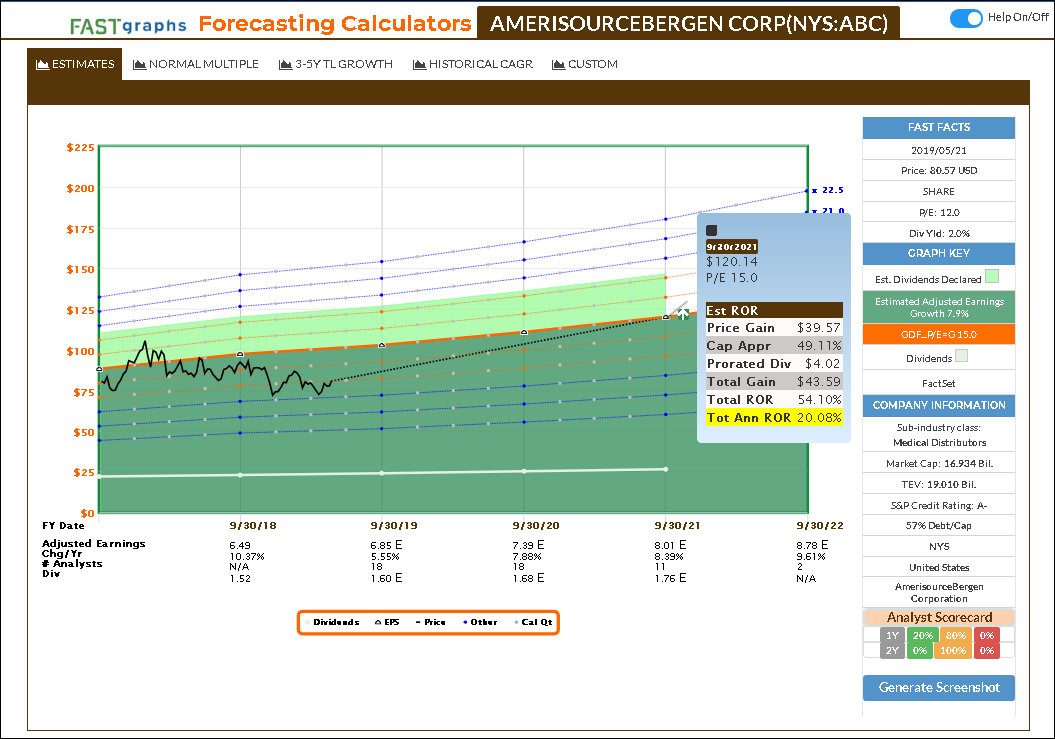

As I have stated many times in the past, I never consider investing in a stock before calculating a specific rate of return expectation. I call this running the numbers out to their logical conclusion. In the case of AmerisourceBergen, if the company did grow earnings at the consensus rate of 7.9% and its P/E ratio expanded from the current 12 to a more rational P/E ratio of 15, its total annualized rate of return out to fiscal year-end 2021 would be slightly over 20%. In other words, the current political risk is already baked into the valuation (price).

As the Wall Street Journal suggested in an article by Charley Grant on May 20 titled: “Everyone Hates Health-Care stocks. Buy Them Anyway.” The article’s byline stated, “relatively attractive valuation and defensive properties could make this sector shine.” I consider this sound advice especially when you understand that these healthcare stocks do not really need to grow very much to generate strong future returns. The point is that even a no-growth business is worth a reasonable multiple of earnings and cash flows, typically in the neighborhood of 14 to 16 times earnings. Consequently, today’s low valuations have already priced in the risk and suggest that high-quality healthcare stocks are attractive.

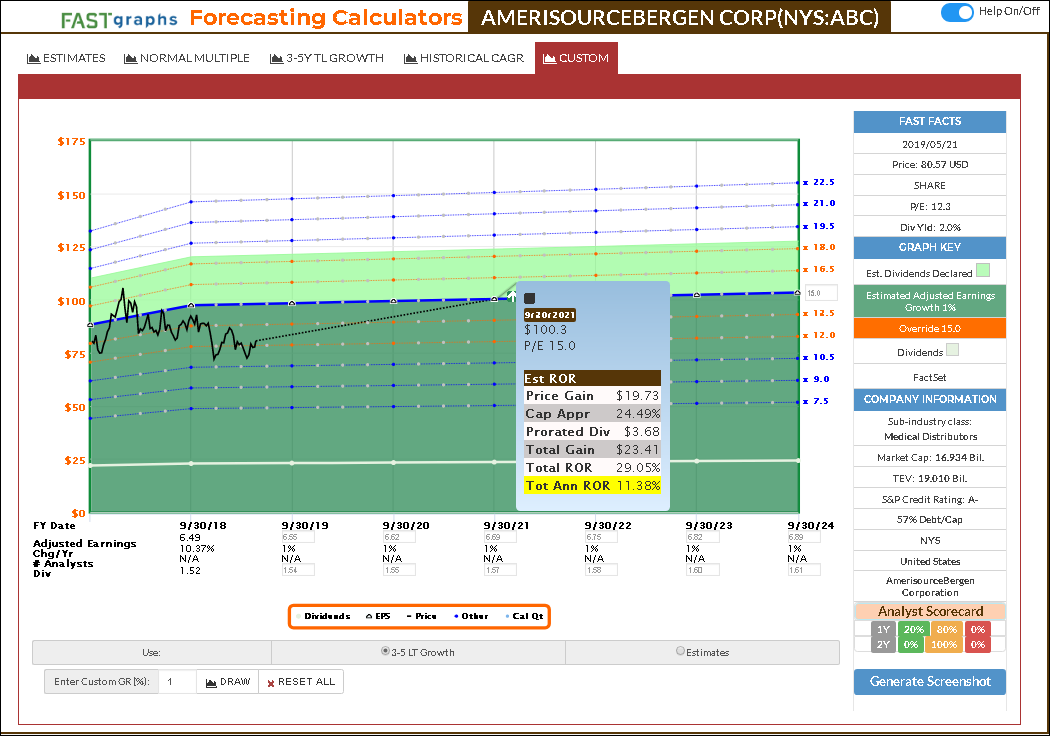

To illustrate how an undervalued stock doesn’t have to grow in order to be a good investment, I present the following “Custom” forecasting calculator where I have overridden the consensus estimates. The following Custom forecast calculator illustrates the return potential on AmerisourceBergen assuming the company only grows at 1% (significantly below consensus) and trades at a rational 15 P/E ratio. Even under that draconian scenario, AmerisourceBergen could still potentially generate double-digit returns over the next couple of years. As I often say, valuation matters, and it matters a lot. But perhaps more importantly, low valuation can mitigate a great deal of risk.

How Reliable are Consensus Estimates on AmerisourceBergen?

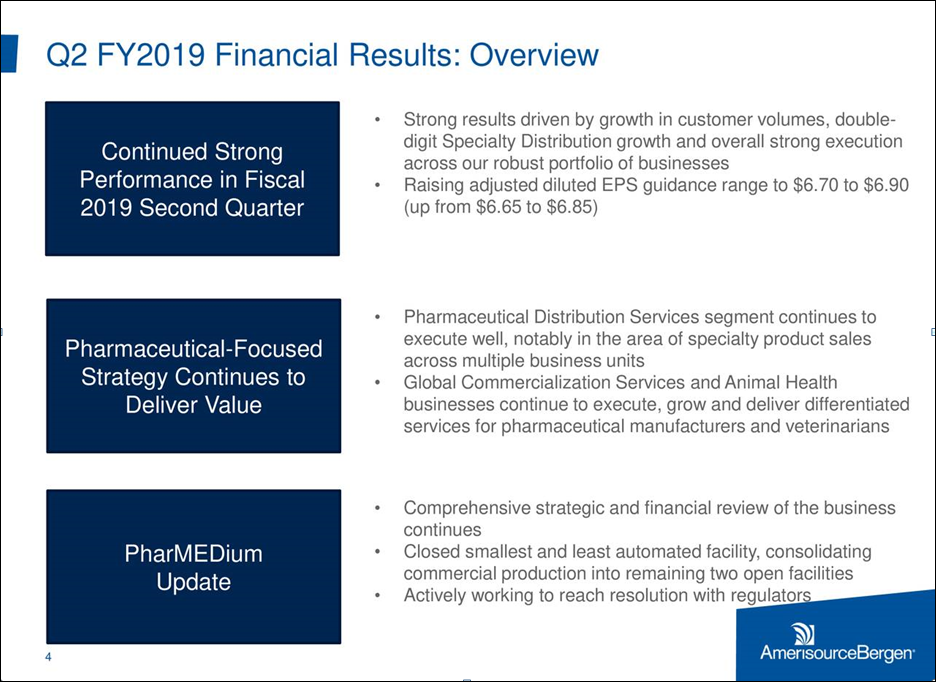

As I often state, as investors we can only invest in the future and not the past. However, it also logically follows that it is implicit upon us to base our decisions on a prudent and reliable forecast of what the future might bring. Consequently, I believe it makes sense to start by reviewing the consensus estimates of the leading analysts following the company. However, it is also important to realize that consensus analyst estimates are quite often derived and aligned with company guidance. The following slide from AmerisourceBergen’s recent earnings report provides their fiscal 2019 (ending in September) guidance for adjusted diluted earnings of $6.70 to $6.90. The reader should note that this guidance is consistent with the consensus estimates of 18 analysts presented in the forecasting calculator above.

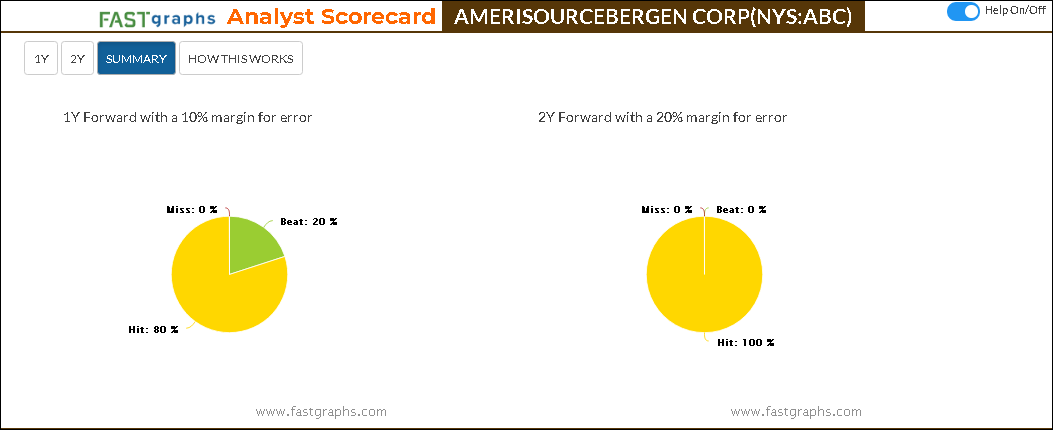

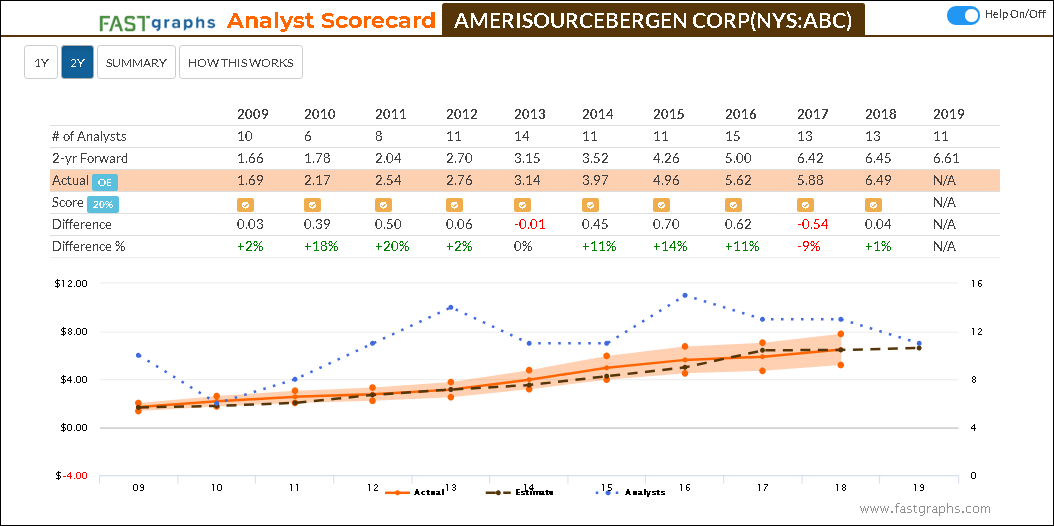

Furthermore, the following Analyst Scorecard illustrates that leading analysts have an excellent track record of forecasting AmerisourceBergen’s earnings in advance. As seen in the following screenshots, analysts have been extremely accurate with their forecasts when they have been made exactly one year or two years in advance of the actual financial reports. Consequently, this provides me some confidence that consensus estimates are a reliable starting point towards providing a reasonable future earnings expectation on this blue-chip dividend growth stock. Therefore, I am enthusiastically motivated to continue conducting a comprehensive research and due diligence process on AmerisourceBergen because I believe the potential is worth my while.

Amerisourcebergen: Thesis for Growth And Success

According to MorningStar: “Business Strategy and Outlook by Soo Romanoff, Updated Apr 08, 2019,

AmerisourceBergen has developed a pharmaceutical platform addressing the comprehensive sourcing and distribution needs of manufacturers and providers. With 20,000 employees and an electronic inventory platform, the company is equipped to ship more than 3 million products a day worldwide. The global scale and sheer pharmaceutical volumes enable the company to negotiate competitive prices, and it can efficiently provide access to a vast portfolio of drugs. The core business, roughly 96% of revenue, is focused on pharmaceutical distribution, and the balance of revenue is attributable to acquired businesses. AmerisourceBergen handles roughly a third of the drugs sold in the United States and has created an extensive footprint into physician-administered products, with key anchor customers within communities. Further, the company operates efficiently in a highly regulated environment, which provides some insulation.”

Furthermore, I believe that regardless of whatever happens to healthcare delivery politically in the future, that AmerisourceBergen will still be positioned as a viable long-term business.

AmerisourceBergen’s confidence in their future growth was presented in their most recent earnings report as follows:

FAST Graphs Fundamentals Analyzer Out Loud Video: AmerisourceBergen

In the following analyze out loud video I’m going to run AmerisourceBergen by the numbers looking at numerous cash flow and earnings metrics. In addition to looking at valuation, I will also be looking at dividend coverage and safety. There is more than one way to skin a cat, and certainly more than one way to value a business. However, no matter how you evaluate AmerisourceBergen, I believe the conclusion is the same. This is an extremely high-quality dividend growth stock that is currently available at a very attractive valuation.

Summary and Conclusions

I believe that AmerisourceBergen is an extremely high-quality dividend growth stock that is currently an attractive total return investment based on low valuation and above-average potential growth of earnings and dividends. Consequently, I also believe that the political risk associated with medical companies in general and AmerisourceBergen specifically is already priced in.

Furthermore, the possibility that Walgreens Boots Alliance may make a play for the remaining shares in the company they do not already own, provides an interesting and reasonable short-term speculation. AmerisourceBergen is certainly cheap enough at current levels for Walgreens to make an offer above current valuation and still purchase the shares at a sensible valuation. However, I don’t believe the acquisition needs to occur in order to make AmerisourceBergen an attractive long-term dividend growth investment.

Finally, and as always, I suggest that investors conduct their own comprehensive research and due diligence. Caveat emptor.

Disclosure: Long ABC.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.