Introduction

In part 1 of this series on forecasting future results as the key to investing success, I suggested that reviewing consensus analyst estimates was a smart and prudent starting point. Furthermore, I attempted to illustrate that consensus estimates tend to be accurate enough to help you determine whether a deeper dive into the company is warranted or not. However, I also suggested that it’s imperative to go beyond simply looking at consensus estimates before you make your final investing decisions.

In simple terms, reasonably accurate forecasts are ultimately achieved as a process commonly referred to as research and due diligence. Just as I pointed out in part 1 that consensus estimates would not be perfectly accurate, this same principle applies to all forecasts and/or estimates. We must recognize that the only thing certain about the future is uncertainty. Therefore, we must also accept that investing based on our best forecasts is not a game of perfect, nor does it need to be.

In point and fact, as I stated in part 1 when I evaluated United Technologies, the direction of future growth is just as important as getting the number as correct as possible. In other words, at its most crude level you are attempting to forecast whether the company will be growing or shrinking. If it is growing, you are likely to generate a positive rate of return, and vice versa. Of course, the actual return you eventually will earn will be functionally related to specific growth the company achieves.

Additionally, I believe the best way to accomplish a forecast that is reasonable within an acceptable range of probabilities is by applying both a macro and micro analysis. However, by macro I am not implying attempting to forecast the economy or political events. Instead, I believe that investors should focus on the major macroeconomic trends that identify the possibilities of major future investment opportunities. There are two that quickly come to mind, analyzing and monitoring demographics, and focusing on the potential of technological advancement.

The Macro Approach

Regarding demographics, perhaps the most important factor to recognize is the current distribution of our population. We still have the bimodal powerful demographic forces of the graying of America and the baby boomer generation. Additionally, we also have a rapidly growing economic force associated with millennials which are those people born in the 1980s and 1990s. The Pew Research Center recently defined our current population demographic makeup as follows:

- “The Silent Generation: Born 1928-1945 (73-90 years old)

- Baby Boomers: Born 1946-1964 (54-72 years old)

- Generation X: Born 1965-1980 (38-53 years old)

- Millennials: Born 1981-1996 (22-37 years old)

- Post-Millennials: Born 1997-Present (0-21 years old)”

The point is that these various demographic forces have different spending habits and desires. Consequently, by considering the consumption tendencies of these and other demographic segments will allow us to make better informed forecasts on the future health of several industries that will serve these large and growing markets. We may not be able to generate precise numbers by reviewing demographics; however, we should be able to determine if there’s an opportunity for growth or not.

Of course, three obvious industries would be healthcare, technology and financial services associated with retirement planning. In the most basic terms, thinking about these demographics can help us establish and identify whether a true market would exist for the products and services of the companies we might be interested in investing in.

Once again, this is not a game of perfect. Therefore, I don’t want the reader to be intimidated by what appears to be a complex approach. The central idea is to be essentially correct that there is a large and possibly even a growing market for a given company’s products or services. If you believe there is, then it really comes down to how well the company’s management can execute. You can make these judgments by simply reviewing each company’s quarterly financial reports. This is partially what I mean when I suggest that we can learn from the past. The company’s past achievements in their given market can give us clues as to how well they might do going forward.

The Micro Approach

From the macro, the individual investor needs to move to the micro because ultimately, it is the individual security, or stock selection that produces long-term returns. As I’ve previously discussed in part 1, long-term returns are a function of earnings past, present and future. And, I believe there’s no better way to come up with a reasonable forecast of future earnings than by conducting a thorough and comprehensive fundamental analysis on every company under consideration. However, the focus should be on attempting to determine whether said company possesses the future earnings power to provide you the returns required that are commensurate to the amount of risk you are taking to achieve them.

As an example, years ago, I received a communiqué from MorningStar promoting a new growth stock product they were offering. Keep in mind that they were specifically speaking about growth stocks; however, I believe the underlying principles apply to all stock investing. There are two excerpts from their promotion that I thought succinctly spoke to what I’m discussing in this article, the first is as follows:

“The central question for successful growth investing, as we see it, is this: how long can above-average growth continue? Answer this question correctly, and you can make a lot of money, no matter how much you pay for a company’s stock. Compounding growth is a powerful force. “

The second excerpt talks about companies sustaining and building their moats:

“How can investors spot growth that’s unlikely to fizzle out?

Our answer: focus on the economic moat trend. A company’s ability to shield its business franchise not only protects its current profits, but also its growth prospects. Rather than simply focusing on companies already benefiting from strong competitive advantages–or focusing on companies that already have wide economic moats–we look at companies still building and growing their economic moats. We believe this brand of growth investing leads to high-quality companies that can consistently compound their intrinsic values year after year.

In other words, we buy not only growing companies, but also sustainably growing companies.”

To my way of thinking, MorningStar’s above advice is extremely important when trying to determine the future growth potential of any company you are analyzing. This is where the quality and depth of the management team as well as the strength of the company’s balance sheet would come into play. On the other hand, this is often easier said than done. Recognizing and correctly evaluating a company’s strategic advantage is a difficult task indeed. Furthermore, this is a process and not a one-time act.

A simple example will hopefully clarify what I’m suggesting here. There’s an old Wall Street adage that states that you don’t want to invest in even the best buggy whip manufacturer after Henry Ford came along. In other words, the buggy whip industry was totally disrupted with the invention of the model T Ford and the assembly line. Cars rapidly replaced the horse and buggy. Consequently, buggy whip sales plummeted.

In other words, it’s imperative that the investor/owner continues to monitor, check and recheck a company’s strategic advantage on a continuous basis. Due diligence must be ongoing. Perhaps the good news is that a company’s prospects usually don’t change overnight or in the blink of an eye. Therefore, the diligent investor would have ample time to re-evaluate each company’s prospects as things change.

My approach to conducting research and due diligence at the micro level is rather simple and straightforward. In addition to reviewing financial statements, I like to spend some time on the company’s website. Here I’m attempting to understand what the business does, what products or services it sells, and who its customers are. Again, I’m not trying to make a perfect estimate, instead, I’m simply trying to get a feel for the business.

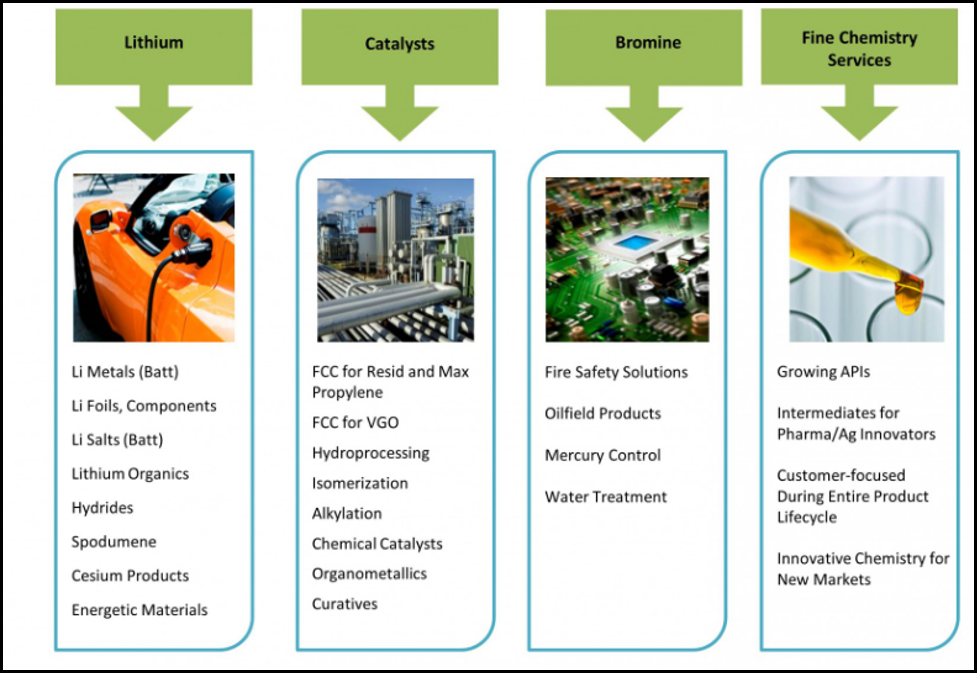

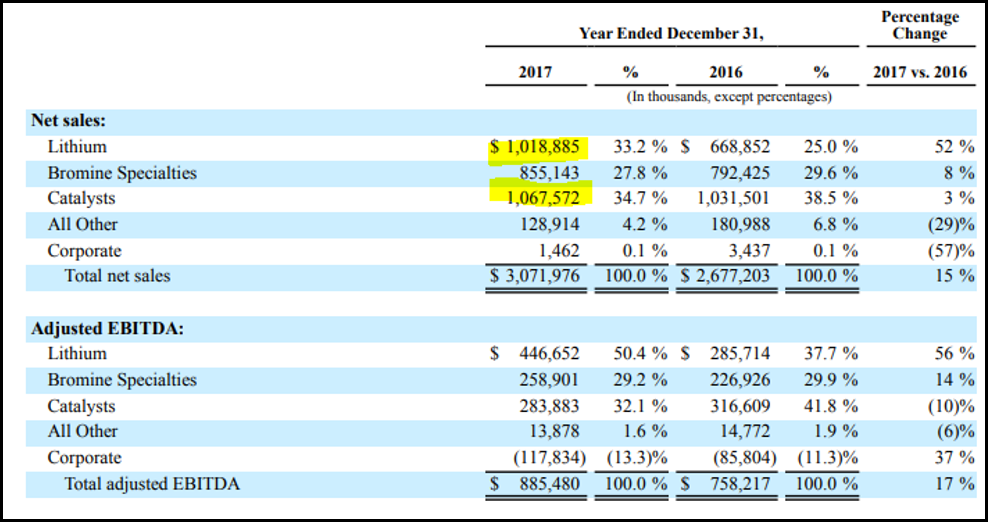

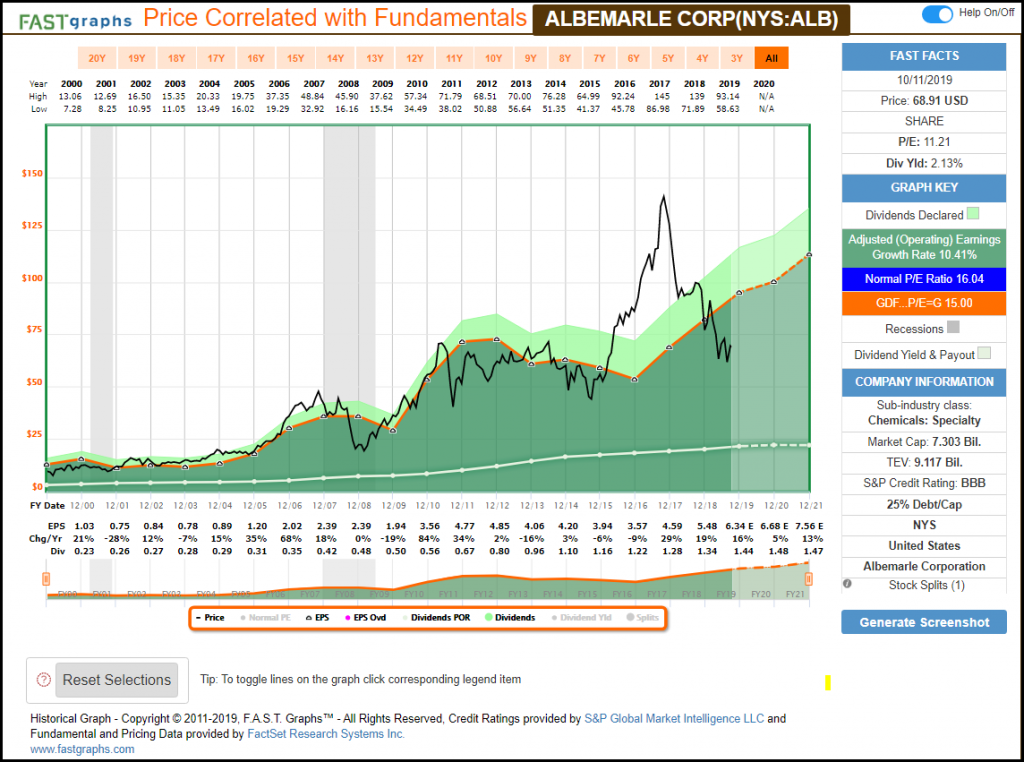

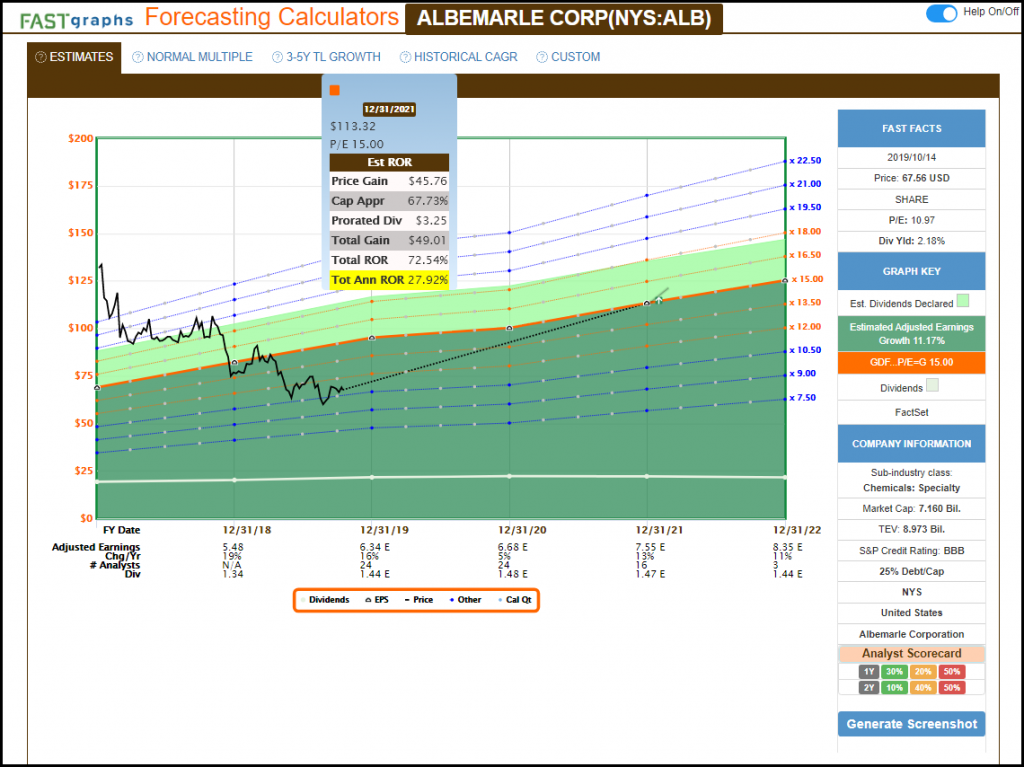

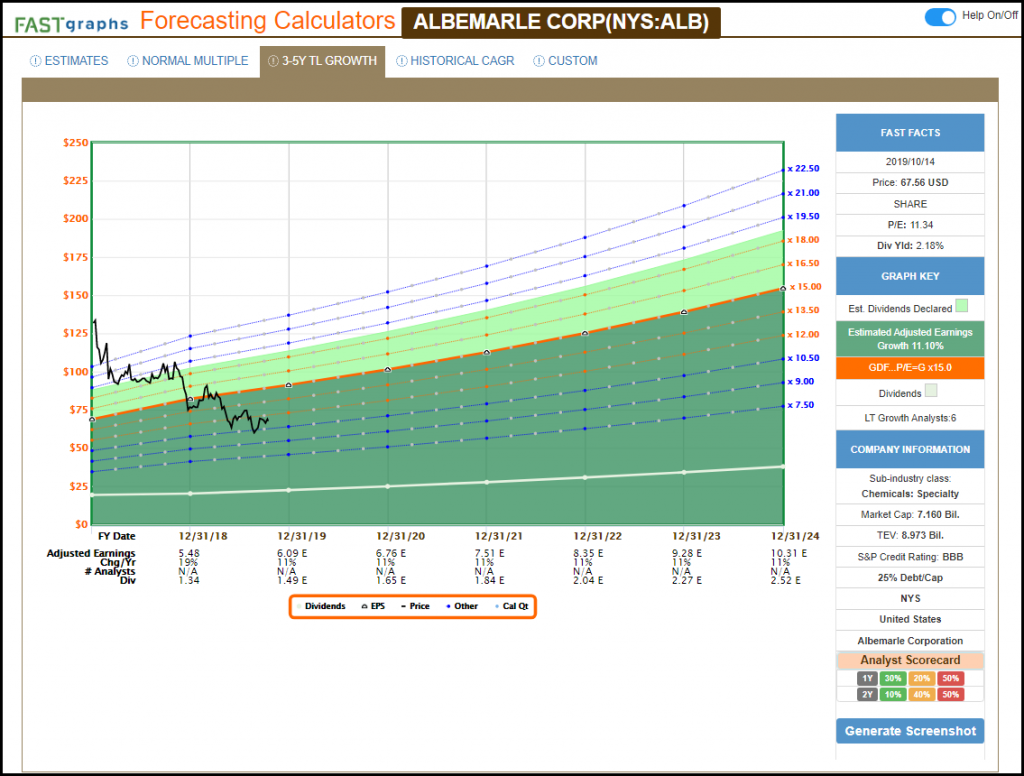

One thing that I do try to determine with every company I examine is exactly what businesses are they in and what contribution does each division or area contribute to sales and earnings, etc. For example, I offer the following slides from Albemarle’s (ALB) recent financial report that discusses their various business divisions, with the second and third slides reporting the contribution that each division makes to the overall business. But most importantly, I can also identify which division (in this case lithium), is growing the fastest.

By examining the financials that ended in December 31, 2017 we see that lithium grew from 25% contribution to 32.2%. Which clearly is the fastest growing division by far.

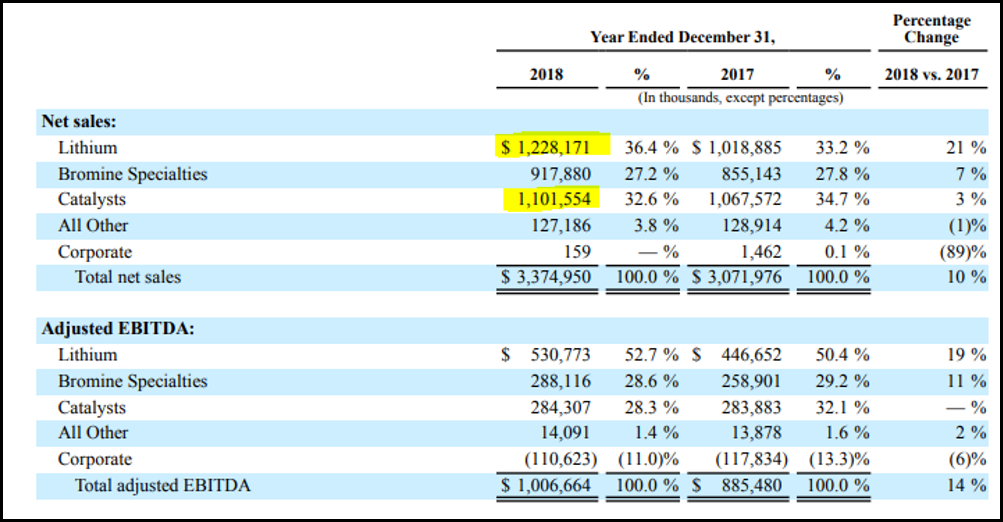

When looking at the year and December 31, 2018, we see that lithium has now become the largest and the fastest growing division in Albemarle. However, we might also note that the rate of change of growth, although still high, has slowed down from 52% to 21%.

With the above information clearly in mind, I can comfortably determine that Albemarle’s lithium business is the main contributor to their recent acceleration in growth. Furthermore, without attempting to put a number on it, I can estimate with confidence that Albemarle’s business will continue to grow going forward as lithium demand should continue to be strong for years to come.

Consequently, I also have a comfortable level of confidence that consensus estimates might be reasonable as well. Therefore, I can begin to run “what if” performance calculations so that I have a reasonable expectation of what my future total returns might be your look like.

Once I have spent some time on the company’s general website, I will typically turn to investor services. If you recall from part 1, I pointed out that consensus analyst estimates are heavily driven by company guidance. Analysts will often receive that guidance by attending investor conferences and reviewing company slide presentations. As lay investors, we do have access to those same presentations where we can make our own judgments and estimates. Moreover, I am careful to review these presentations recognizing that the company is endeavoring to put their best foot forward.

A Quick Review of History-Learning from the Past

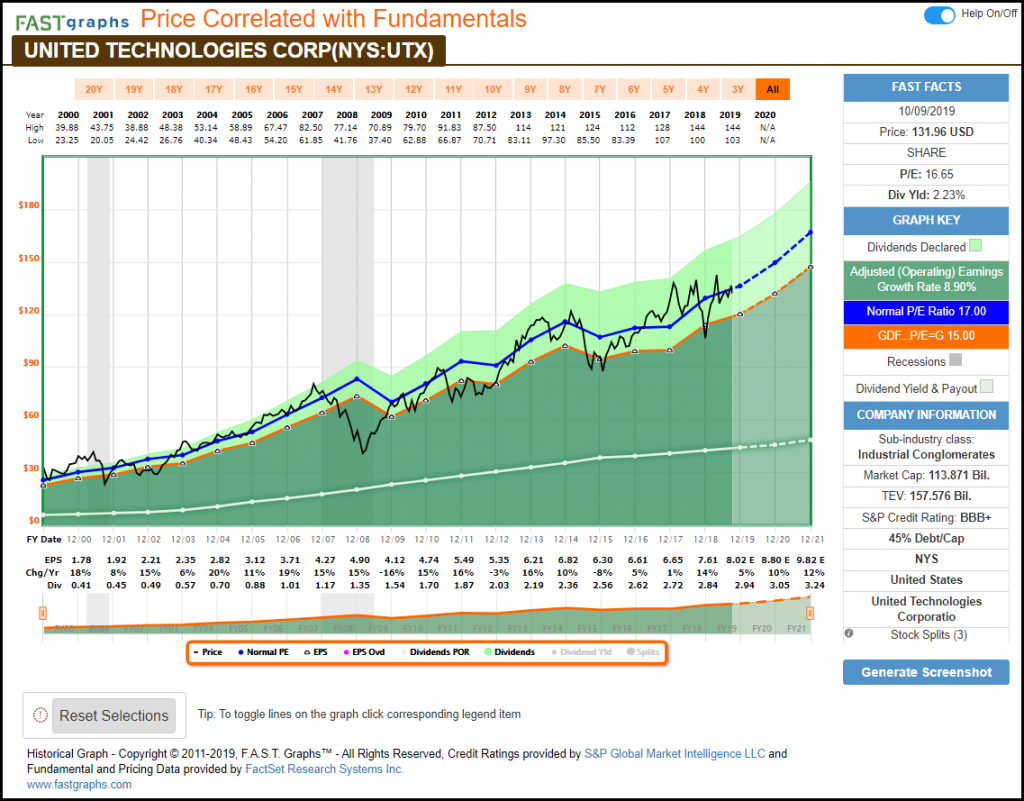

In part 1 of this two-part series we used examples of companies that illustrated the undeniable earnings and price relationship and correlation. Although these articles are essentially focused on the future, there is much that can be learned from the past. So, before we move on to a closer examination of the future, let’s review the past by including United Technologies (UTX), one of our example companies from part 1, and compare it to a company Lockheed Martin Corporation (LMT) with a stronger history of earnings growth.

United Technologies Corp.: Semi-Cyclical Moderate Growth

The primary reason that forecasting future growth is so important is because it will be the generator of the returns you will earn as a shareholder. Higher growth produces a larger future income stream which in turn will translate into more dividends and a higher total return. This applies whether you are investing at fair value are not. However, when you do invest at fair value, you are very likely to earn returns that are correlated to the growth achievement that the company produces.

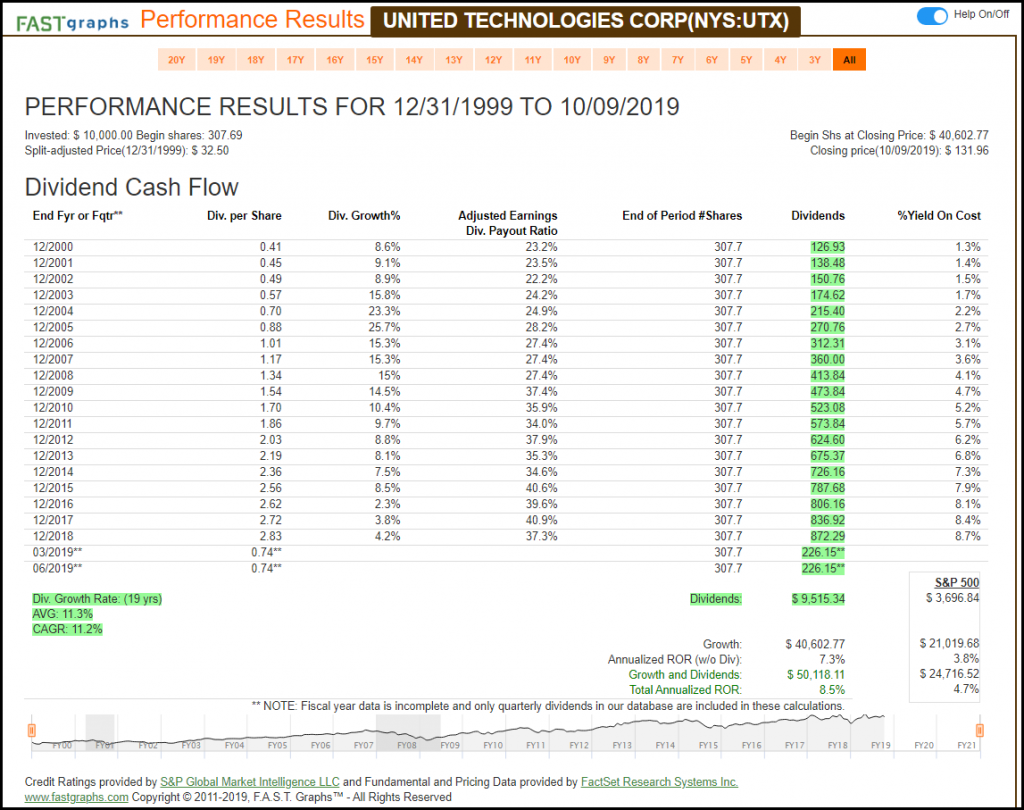

In the case of United Technologies, you can see from the graphic below that the company has grown earnings at 8.9% per annum since calendar and fiscal year 2000. Furthermore, you also note that earnings growth is what I would call quasi-cyclical with occasional periods of flattening or slight drops. On the other hand, the dividend record is very consistent (the white line on the graph). You might also note that the stock was slightly overvalued at the beginning of this timeframe, but only slightly.

Consequently, it should be no surprise that your total return performance of 8.5% correlated very closely with the company’s 8.9% earnings growth rate with only a slight adjustment due to valuation. You should also note that dividend growth averaged slightly over 11% per annum, and even though this is higher than the growth rate, it is certainly related.

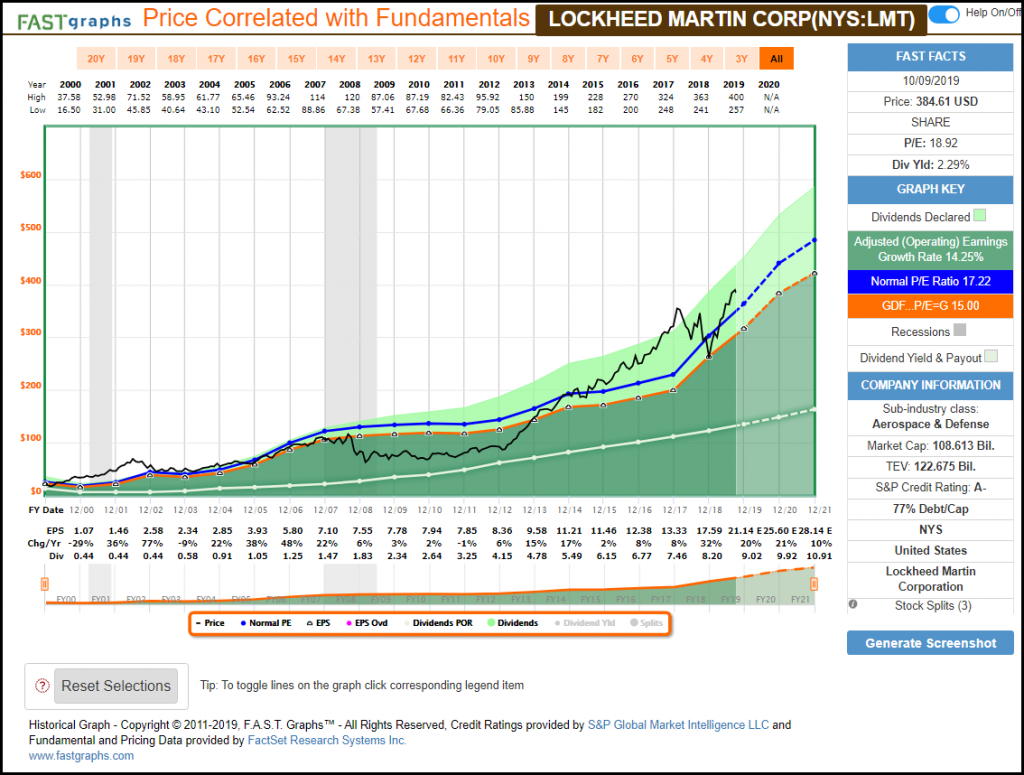

Lockheed Martin Corp.: In a Similar Industry but Higher and More Persistent Growth

In contrast to United Technologies’ moderate growth achievement, Lockheed Martin has grown earnings at over 14% per annum since 2000. Additionally, Lockheed Martin also has a very consistent record of dividend growth (the white line on the graph).

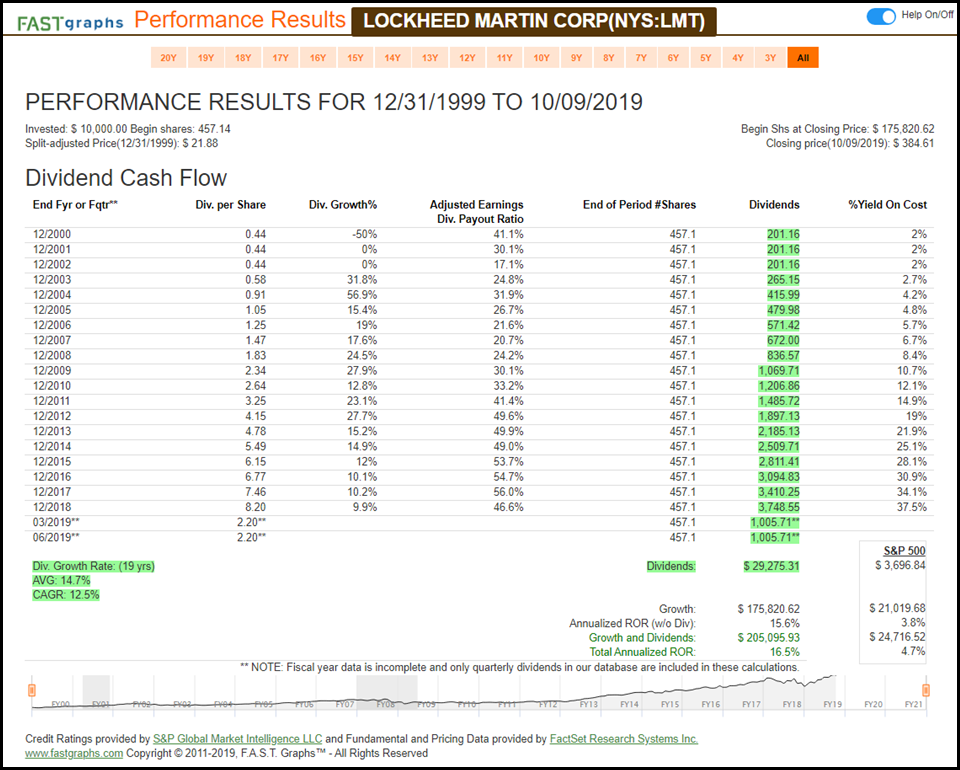

Therefore, when we review the performance of Lockheed Martin Corp, we discover that shareholder returns were very highly correlated with the company’s faster earnings growth rate achievement over this timeframe. But perhaps even more importantly, we also see a significant advantage in total cumulative dividends earned. Moreover, we see that the dividend has grown on average at 14.7%, which is very closely correlated to the company’s earnings growth rate achievement. The reason why forecasting the future is so important is because the company’s operating growth rates will be the primary drivers of your future returns as evidenced by these two examples.

Starting with Consensus Analyst Estimates

As a review, let’s revisit what was discussed in part 1 regarding starting out with consensus analyst estimates. There tends to be a lot of controversy when talking about the consensus estimates from leading analysts following a given company. Most of the controversy deals with people’s opinions about the accuracy, or lack thereof, of analysts’ published expectations. In my opinion, these criticisms fail to recognize that estimating a company’s future earnings is not, and cannot, be an exact science.

Since estimates are forecasts, much of the facts that analysts are dealing with or are attempting to calculate are mostly unknowns. However, as I stated in part 1, estimates should not be mere guesses, instead, they should be reasonable projections based on all the factual data the analyst can assemble, coupled with reasonable projections of the future. Nevertheless, at the end of the day, forecasts are “guesstimates” and most importantly need to be continuously re-evaluated and updated.

Consequently, when I am utilizing analyst estimates to evaluate a business, I always think in terms of ranges and probabilities rather than precise numbers. In other words, if the consensus of leading analysts says they expect the company to grow earnings at a rate of 15% over the next five years, I translate that to mean something, for example, like a range of perhaps 12% to 17%. Again, I’m not trying to be perfect nor do I need to be.

Moreover, when running my numbers to their logical conclusions, I will always run a best case, worst case and my most reasonable case scenario. These “what if” scenarios allow me to assess risk more clearly. Therefore, I believe that I can make sound decisions that are neither overly optimistic nor overly pessimistic. Furthermore, by having a range of probabilities, I am more likely to have actual numbers fall somewhere within my range, than I am if I had tried to hang my hat on an absolute number. Although I still may be mildly disappointed at for example 12% versus 15% growth, I’m at least not overly-surprised because I considered the possibility.

There are other points to consider when reviewing analysts’ forecasts. First, the leading analysts are trained to do their job, and therefore, in theory at least, they should be more qualified than the untrained layman. Again, that doesn’t mean that they will give me perfect information, but I’m at least hopeful that they have conducted a thorough examination of the company’s fundamentals before offering me their forecasts.

Also, investors should recognize that most of these analysts all attend the same investor conferences and conventions. Therefore, they are all viewing and hearing the same investor presentations put on by various companies’ management teams. In theory at least, prudent management teams (operating officers) of a publicly traded company are best served to provide guidance that is lower than their actual expectations in order to be able to beat guidance when earnings are finally reported. As a rule, yes, Mr. Market tends to punish companies that miss analysts’ estimates by lowering its stock price, and reward companies that beat analysts’ estimates by raising its stock price. This at least applies over the shorter run.

To summarize my points regarding investors using consensus analyst estimates as a starting point before conducting their own due diligence, I believe it’s a very rational approach. If used properly, analyst estimates represent an efficient screening tool or process that can prevent the investor from wasting a lot of time conducting an unnecessary due diligence effort.

If analyst estimates do not support a company’s current valuation, there’s no need to dig deeper until price comes into alignment with forecasts, thereby offering an acceptable rate of return (earnings yield) that compensates the investor for the risk they are assuming. However, I will also add that the investor might want to spend some time divining whether (or not) the current estimates are reasonable or not, before either abandoning a more comprehensive research effort or moving forward.

Compounding Is Discounting Future Revenues in Reverse

Most prudent investors consider the art of discounting future revenues back to the present value as an effective method of estimating fair value, or what I like to call True Worth™. The formula for calculating discounted present value (DPV) is a very complex looking mathematical formula. However, I do not want to use complex formulas in this series of articles. Instead, I want to focus on the process and essence of the principle behind forecasting.

Discounting future values is based upon the principle of the time use of money. In theory, a dollar in your hand today is worth more than a dollar you might have to wait several years to get. This is simply the old a bird in the hand is worth two in the bush axiom. Therefore, when looking at future revenues, cash flows or earnings, the rational investor puts more value on a dollar today by discounting the value of potential future dollars. Therefore, the higher the discount rate used, the more the future value of any revenues are reduced. In other words, the bigger the discount rate, the greater you are shrinking the value of future dollars by.

However, you can also look at the same time use of money principle in reverse. Compounding today’s dollars into future dollars is the same concept of discounting future dollars to the present value, only working in reverse. Therefore, keep in mind and recognize that higher future growth rates produce bigger and therefore more valuable income streams.

Furthermore, you can look at the future growth rate (the compounding rate) as the inverse of the discount rate. Since we are now working in reverse, the higher the growth rate that you use in your compounding equation, the larger the future stream of revenues (dollars) will be.

I have always preferred compounding to discounting, because I find it easier to think about. With compounding, I can estimate a future value based on the expected growth rate I estimate and run those numbers to their logical conclusion. Therefore, I can easily calculate the fair value or price I should pay today for those future dollars based on rates of return that I would be willing to accept.

The FAST Graphs Estimated Earnings and Return Calculators allow me to easily make these calculations and, with its override function, run various “what-if” scenarios. Therefore, I can calculate best case, worst case and my most reasonable case scenarios. In my opinion, the discipline of calculating various future values of a dollar’s worth of earnings that I intend on buying today, over a reasonable range of possibilities is the best way I have found of demystifying the concept of estimating fair current value. Admittedly, this may not be an exact science, but it’s a whole lot better than just pure guessing.

FAST Graph Analyze out Loud Video 3M Company: Covering My Research and Due Diligence Process

With the followingAnalyze out Loud Video I am going to summarize how I conduct my own research and due diligence utilizing 3M (MMM) as my example. I am not going to get into detail on 3M specifically, instead, I am just endeavoring to illustrate the process that I utilize. Furthermore, this is my approach and others might do this differently. Nevertheless, all research and due diligence processes are about trying to understand the business and its future potential as thoroughly and effectively as you can.

Summary and Conclusions

The primary purpose of this article on the importance of forecasting the future results of a business is offered to illustrate the conceptual validity of forecasting earnings (and every other metric) as the key to long-term investor success. Although I did introduce a few rudimentary methods of forecasting earnings, my primary objective was to highlight the important role that forecasting future earnings plays in the investment process. As a general statement, the more detailed job of forecasting is about conducting a comprehensive fundamental analysis of the company under consideration.

In summary, one of the most efficient ways I have found to accomplish this task is by going to the company’s website and then into the company’s investor relations area. In most cases you can find investor presentations where the company details its past accomplishments and provides guidance regarding their future expectations. These are the same presentations given to the analysts that are making forecasts. Of course, the company is always putting their best spin on the information; nevertheless, a lot of facts can be gleaned from this process.

Additionally, as I illustrated in the video, I subscribe to research services that allow me to dig deeper into the company’s potential. The point being that just like any job, it’s always easier when you have the right tools. However, in the world of finance there are plenty of tools available for investors to choose from. At the end of the day, the key is to do all you can to know and understand the business as you are positioning yourself as a shareholder in. Knowledge is truly power.

Just as we have seen in the video portion of this article, the company’s stock price will track its earnings in the long run, therefore, it can only logically follow that future earnings will drive future stock prices. Consequently, I will end this article by paraphrasing the sage advice offered from none other than Ben Graham’s Mr. Market metaphor. Ben taught us that investors should not focus on the whims of Mr. Market. Instead, he suggests that the investors are better off concentrating on the operating performance of their companies and on receiving dividends.

Disclosure: Long UTX,MMM

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.