Introduction

This article is a refresh and an update of an article I originally posted in 2015. However, the principles I am presenting are timeless and worthy of being revisited. Moreover, I have updated the supporting examples to more precisely reflect our current market environment.

In part 1 of this series I discussed two important principles. Number 1: be realistic with your yield objective. Number 2: determine how much income your portfolio needs to produce. The central ideas were that in order to be prudent, you should be cognizant and realistic about what the current market environment is offering. And next, your specific objective should be to prudently and conservatively satisfy your own personal needs. I find this a superior approach to simply trying to beat the market or even trying to make the most money you can.

Consistent with this perspective is the importance of having a plan and then exercising the discipline to follow that plan. As the venerable Yogi Berra once said, “if you don’t know where you’re going, how are you going to know when you get there.” So, to answer the question that I am often asked: what is the best way to design or construct a common stock portfolio for retirement? My short answer is always the same – it depends. Because, the truth is, there is no perfect method or strategy for designing a stock portfolio that is right for every individual investor. However, there are principles of sound investing that every investor can follow and apply when designing a common stock portfolio that’s just right for them.

Furthermore, there are general categories that individual investors fall into. Some individuals are young and planning for retirement while other individuals are closer to retirement, and there are some that are already retired. Additionally, each individual investor has different levels of financial resources that specifically apply. To complicate the process even more, individual investors of all types possess unique goals, needs, objectives and risk tolerances. Therefore, the logical secret to designing a successful common stock portfolio is to design one that’s most appropriate for you.

Therefore, the objective of this series of articles is not to attempt to dictate how individuals should design their own stock portfolios. Instead, the objective of this series is to provide information regarding common stock investing strategies and options that everyone can evaluate and ultimately utilize so they can implement and construct a common stock portfolio that’s just right for them.

At the end of the day, it comes down to making the appropriate choices. The most appropriate choices include, but are not limited to, utilizing the most suitable categories of common stocks available as well as the appropriate mix. In one context, the choices approach the infinite, and this can be confusing or even overwhelming. On the other hand, the options can be generally categorized, thereby simplifying the process to a more manageable level.

Of course, individual investors also have the options of either engaging professional help or self-directing their own stock portfolios. This can be done directly by hiring outside professional managers or by investing in packaged products created by professional managers such as mutual funds or ETFs. However, this series of articles is intended for the self-directed individual investor interested in designing and managing their own common stock portfolios.

Stock Selection: What Are the Choices?

On the US stock exchanges alone, individual investors have almost 20,000 individual stocks (companies) to choose from. No matter how diligent you could be, it would be impossible for any individual to conduct a comprehensive analysis on all of them. Therefore, individual investors need a method of separating the wheat from the chaff. Furthermore, this is consistent with my common mantra: “it is a market of stocks and not a stock market.”

One effective way to accomplish that is to break the larger list down into broader categories based on specific characteristics and attributes. In his best-selling book “One Up On Wall Street,” renowned mutual fund manager Peter Lynch presented what he referred to as “The Six Categories.” Personally, I believe that Peter Lynch provided a succinct summary of the broad categories or types of common stocks available for investment consideration.

However, his six categories are very broad, and therefore, within each category there are many additional nuances that investors are best served to recognize and understand. Nevertheless, I believe that Peter Lynch provided an excellent foundation with his presentation of the six broad categories available to investors. To clarify this important distinction further, I turn to Peter Lynch and his own words with the following quote:

“There are almost as many ways to classify stocks as there are stockbrokers – but I found that the 6 categories cover all of the useful distinctions that any investor has to make.”

To provide the reader with a more comprehensive understanding of the six broad categories of stocks that Peter Lynch presented, I offer the following review of each category with a sample FAST Graphs to provide deeper insights. Importantly, since Peter Lynch was primarily referring to the characteristics of six broad types of businesses, I have taken stock prices off most of the graphs. My goal was to allow the reader the opportunity to focus on the types of businesses that Peter Lynch was describing without the bias that volatile stock movements often brings.

Peter Lynch’s Six General Categories

Below I present Peter Lynch’s six general categories with a short description taken directly from his best-selling book “One Up On Wall Street.” Then I present an example or two with brief commentary of my own with the objective of providing a deeper insight into each category and what each offers from an investment perspective. When appropriate, my examples will come directly from what Peter Lynch said. But most importantly, my examples are not recommendations to buy today; instead, they are just offered as examples of the types of companies Peter Lynch was referencing.

Slow Growers

“Usually these large and aging companies are expected to grow slightly faster than the gross national product. Slow growers didn’t start out that way. They started out as fast growers and eventually pooped out, either because they had gone as far as they could, or else they got too tired to make the most of their chances. When an industry at large slows down (as they always seem to do), most of the companies within the industry lose momentum as well. Electric utilities are today’s most popular slow growers.”

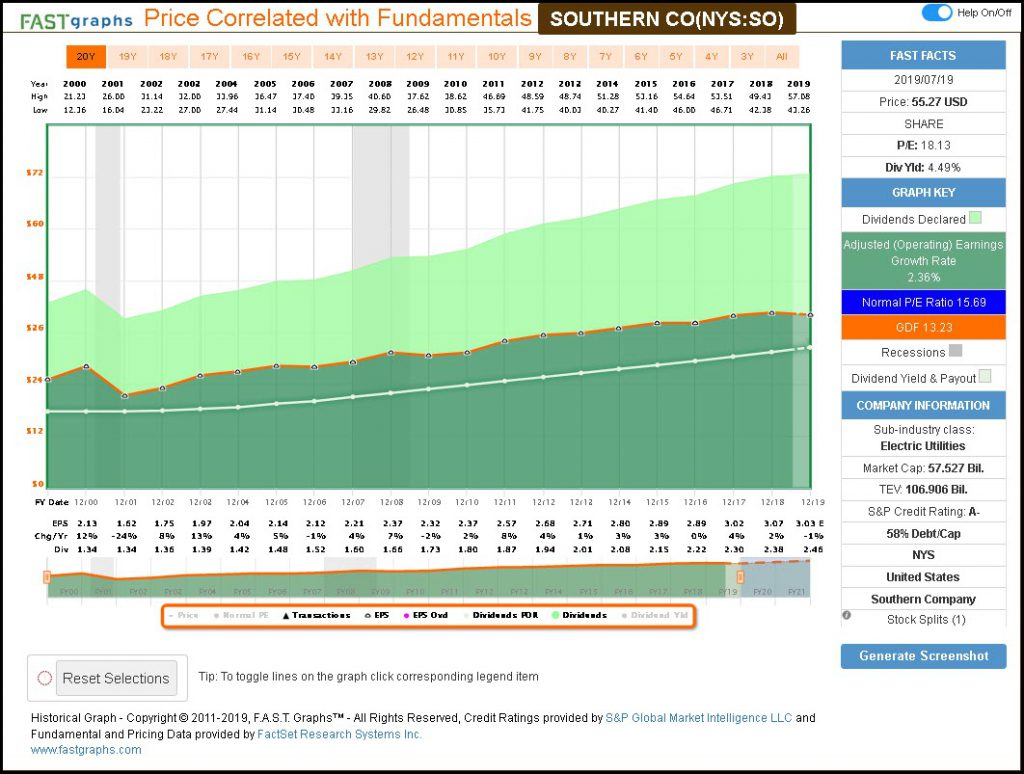

Southern Company (SO): A Slow-Growing Utility

From the following graph, we see a quintessential example of a slow-growing utility that Peter Lynch suggested as a popular slow grower. Long-term earnings growth has averaged only 2.36%. However, the primary attraction to investing in utilities is not for growth; instead, it is for their above-average dividend yields.

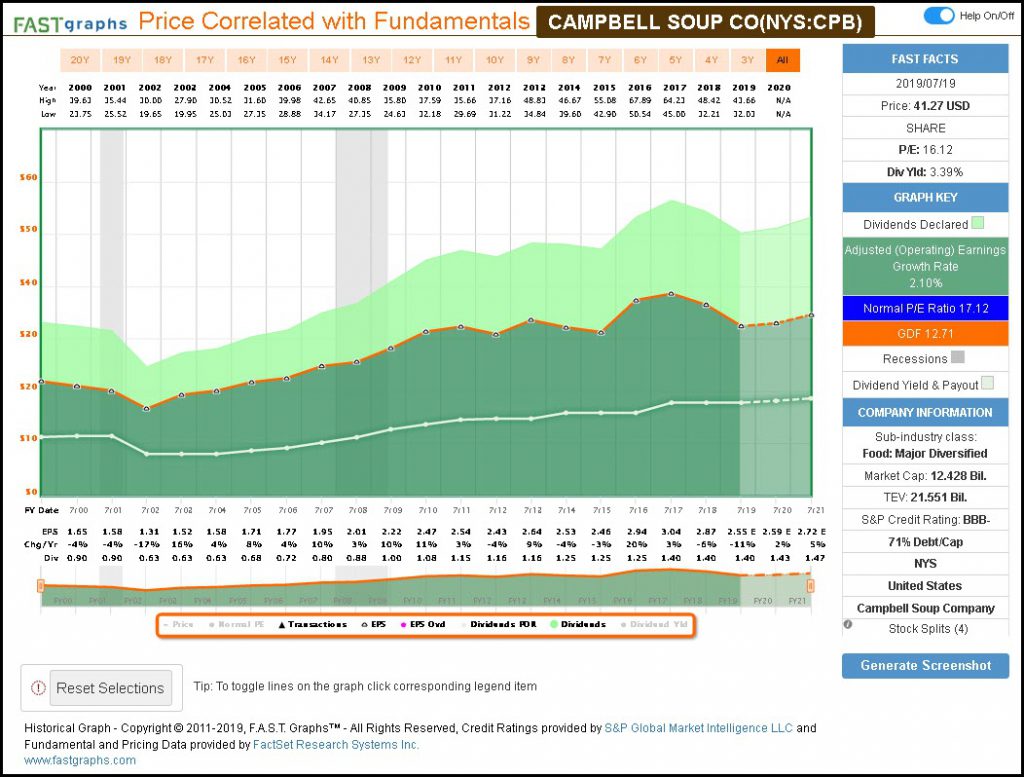

Campbell Soup Company (CPB)

However, not all slow growers are utility stocks. Therefore, I present Campbell Soup as a second example of a slow grower from the consumer non-durables sector. Since fiscal year 2000, Campbell Soup has grown earnings at 2.10%. The company does offer a moderately generous dividend, but its average dividend yield is lower than utilities such as Southern Company typically offer when valuations are sound. Importantly, that previous statement implies that both companies are purchased when valuation is sound.

The Stalwarts

“Stalwarts are companies such as Coca-Cola, Bristol-Myers, Procter & Gamble, Hershey’s, Ralston Purina and Colgate-Palmolive. These multibillion-dollar hulks are not exactly agile climbers, but they are faster than slow growers.”

Stalwarts are an important category for retired investors and dividend growth investors. Many of the Dividend Aristocrats and Dividend Champions are found in this category. However, as Peter Lynch pointed out, stalwarts will not necessarily produce high growth, but most of the companies in this category would be considered blue chips. Nevertheless, quality often comes at premium valuations. Therefore, it can be difficult to find stalwarts at attractive values.

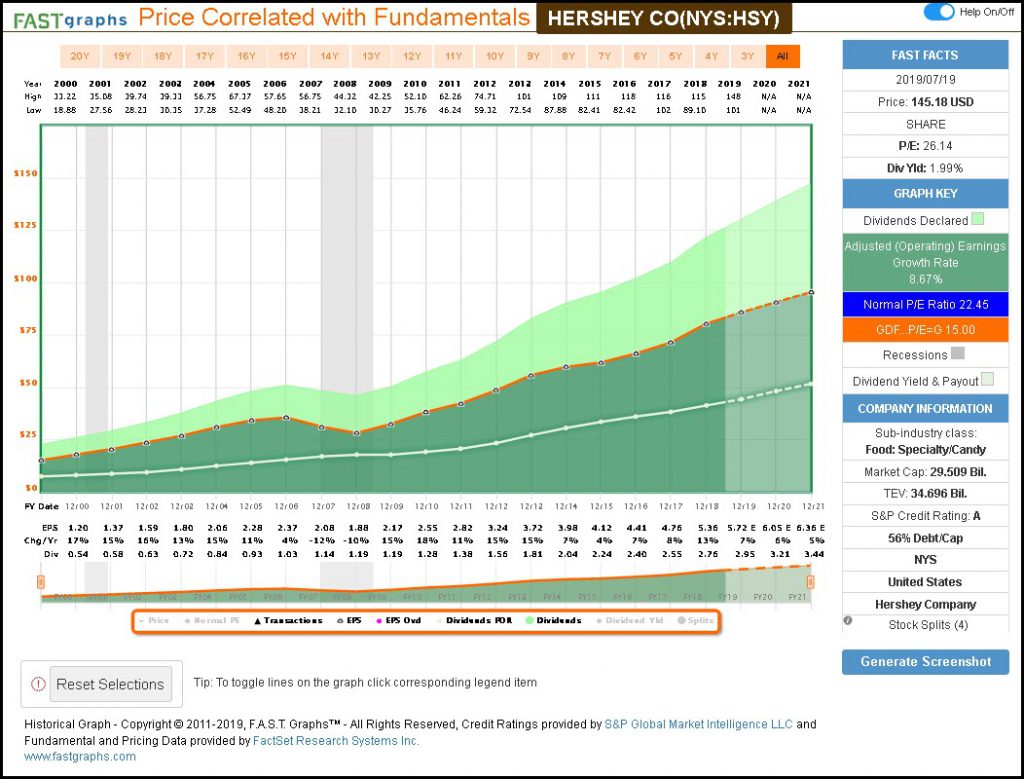

Hershey Company (HSY)

Hershey is a blue-chip dividend growth stock with the above-average earnings growth of 8.67%, and above average dividend growth of 9.5%. However, Hershey did freeze its dividend in 2019 during the Great Recession. Although this is one of my favorite dividend growth stocks, I do want to point out that I consider Hershey extremely overvalued currently. Nevertheless, it is a classic example of a Peter Lynch stalwart.

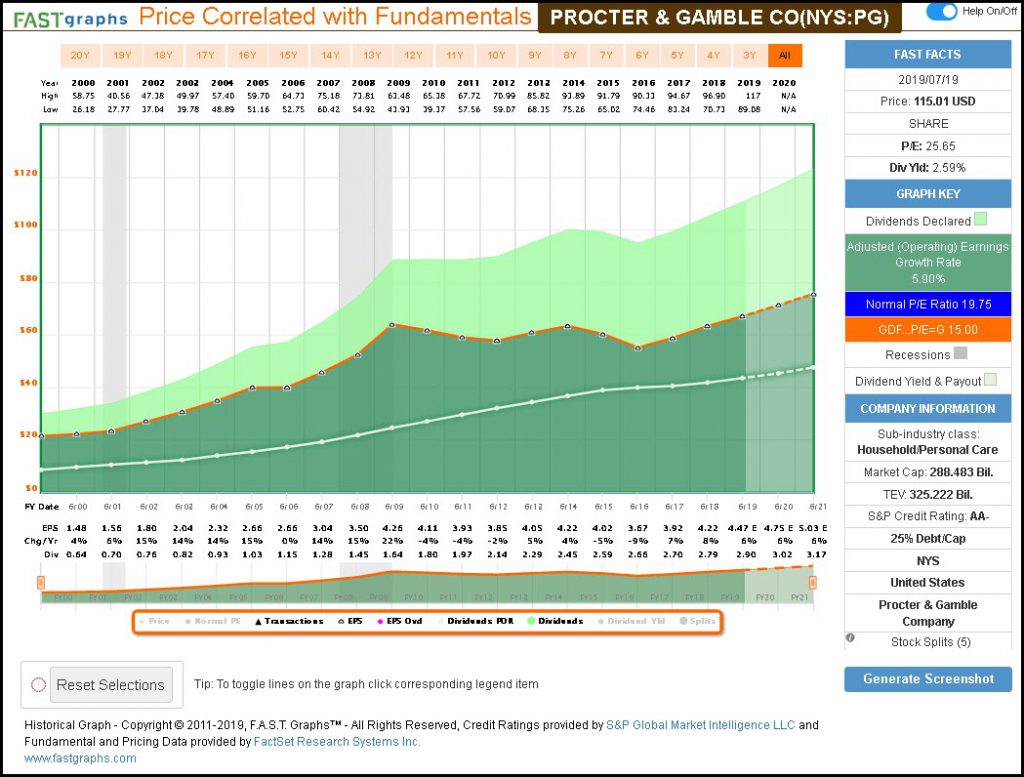

The Procter & Gamble Company (PG)

The blue-chip stalwart Procter & Gamble has grown earnings at 5.9% since fiscal year 2000. Although this qualifies it as a faster grower than the slow growers presented above, the reader should note that growth has been slowing in recent years. Although not depicted, growth over the last decade or so would place Procter & Gamble in the slower grower category comparable to what we saw with Campbell Soup. This is important because investors should be aware that companies can move from one category to the next, especially as they get larger, as is the case with Procter & Gamble.

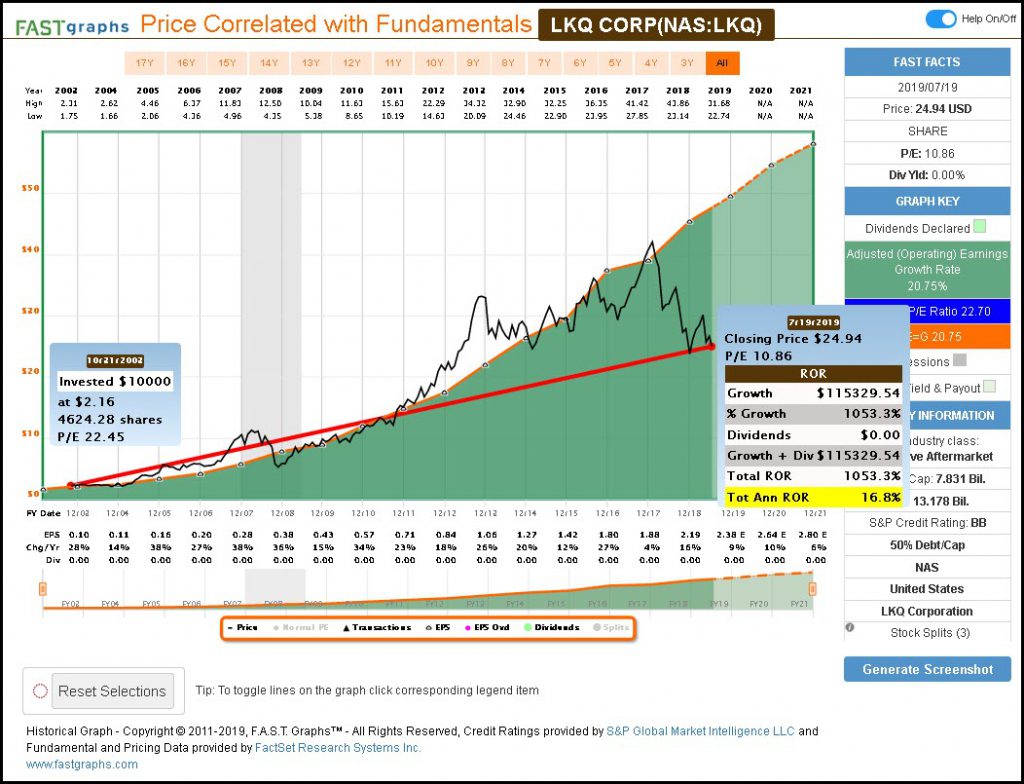

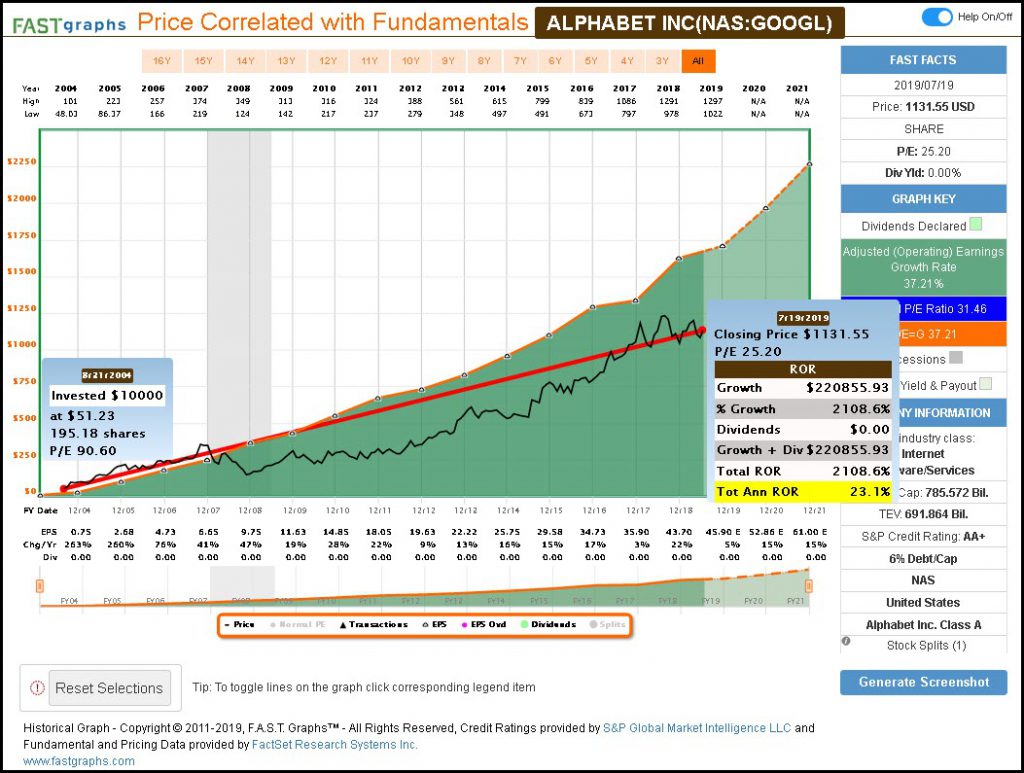

The Fast Growers

“These are among my favorite investments: small, aggressive new enterprises that grow at 20 to 25% year. If you choose wisely, this is the land of the 10-40 baggers, and even the 200 baggers. With a small portfolio, one or 2 of these can make a career. Fast-growing company doesn’t necessarily have to belong to a fast-growing industry. As a matter of fact, I’d rather it didn’t.”

Although Peter Lynch did not mention any fast growers by name, I offer the following examples to illustrate the powerful returns possible with fast growers. Each of the three examples presented below met his criteria of a “10 bagger” or better. LKQ could classify as a “small aggressive newer enterprise that has grown at 20% a year,” but Google is currently a behemoth as a result of its extremely high historical earnings growth thus far.

With these examples, I did include monthly closing stock prices in order to calculate their historical performance. Therefore, I will let the F.A.S.T. Graphs and the calculated performance results on each stand on their own. The key points the reader should focus on are the historical earnings growth rates and the long-term returns that each have produced. However, it should also be noted that neither of these fast growers pays a dividend and all the return has resulted from capital appreciation over time.

LKQ Corp. (LKQ)

Alphabet Inc. (GOOGL)

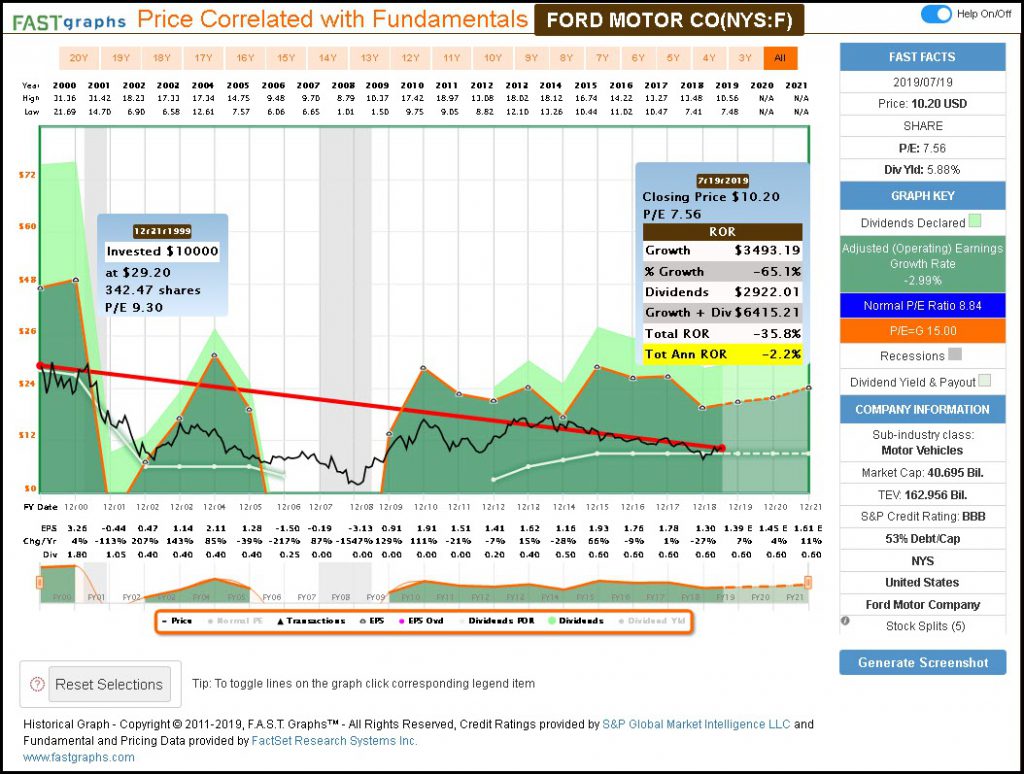

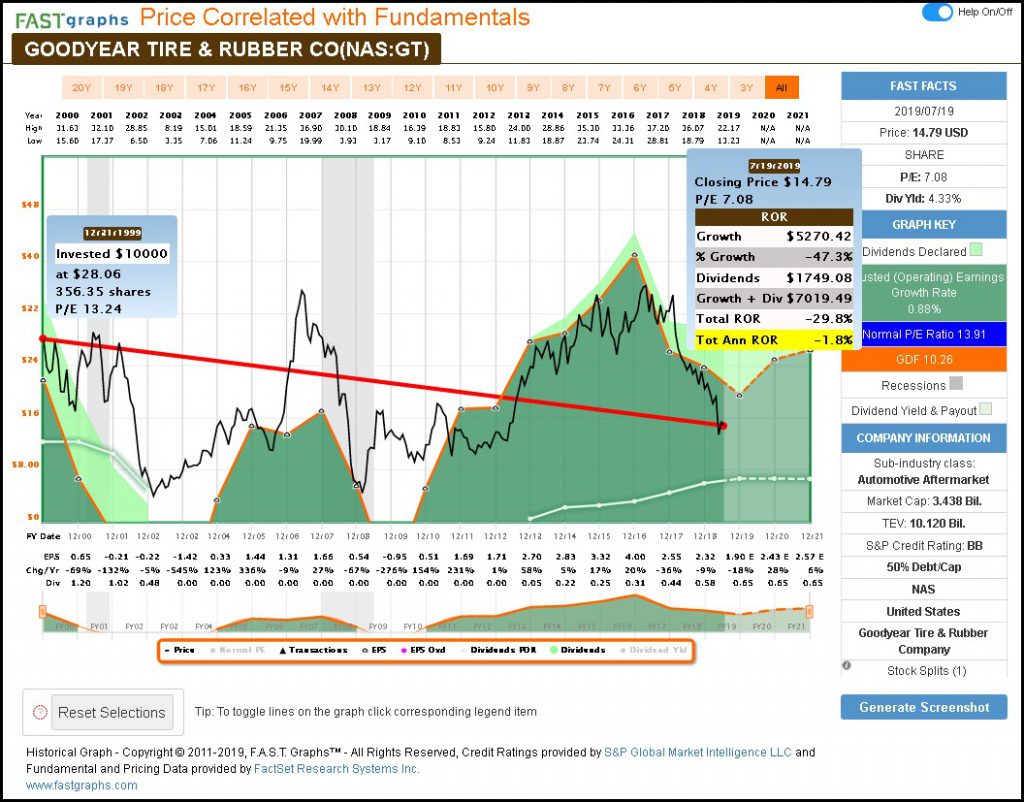

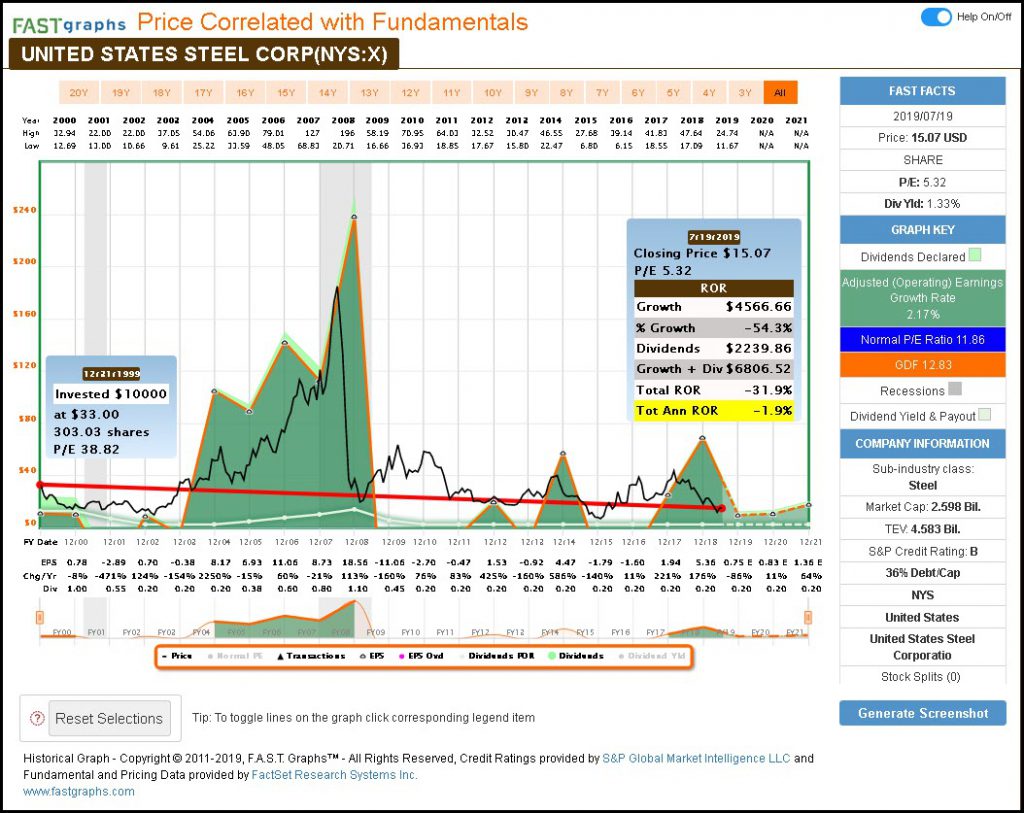

The Cyclicals

“A cyclical is a company whose sales and profits rise and fall in regular if not completely predictable fashion. In a growth industry, business just keeps expanding, but in a cyclical industry it expands and contracts, then expands and contracts again. The autos and the airlines, the tire companies, steel companies, and chemical companies are all cyclicals. Even defense companies behave like cyclicals, since their profits rise, and fall depends on the policies of various administrations.”

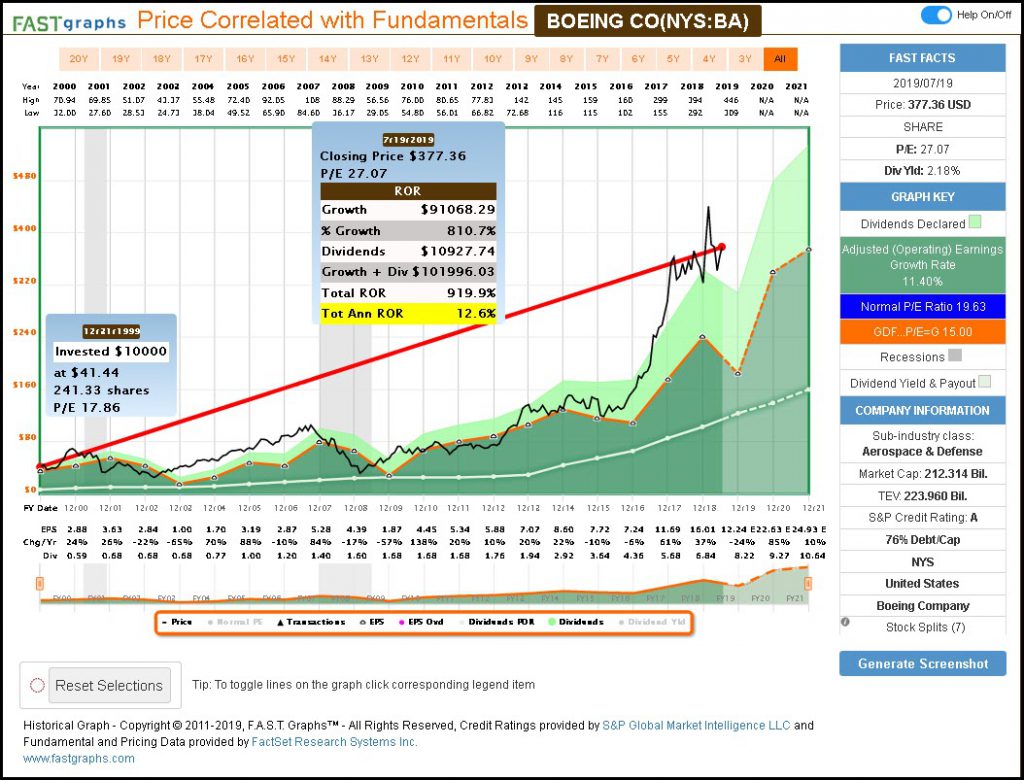

When examining the following graphs on well-known cyclicals in the autos, tire and steel sector, we see classic examples of what Peter Lynch meant when he said, “profits rise and fall in regular if not completely predictable fashion.” The associated performance reports of each of these first three examples illustrates the unpredictable nature of investing in them.

I also included Boeing as a defense company to illustrate how they behave like cyclicals. However, most defense companies I have examined are a lot less cyclical than the autos, tire and steel which are deep cyclicals. As a result, the dividend income stream from most defense companies is often more predictable than their semi-cyclical earnings results. But most importantly, this illustrates how diverse companies can be within each of these 6 broad categories.

Ford Motor Company (F)

Goodyear Tire & Rubber Co. (GT)

United States Steel Corp. (X)

Boeing Co. (BA)

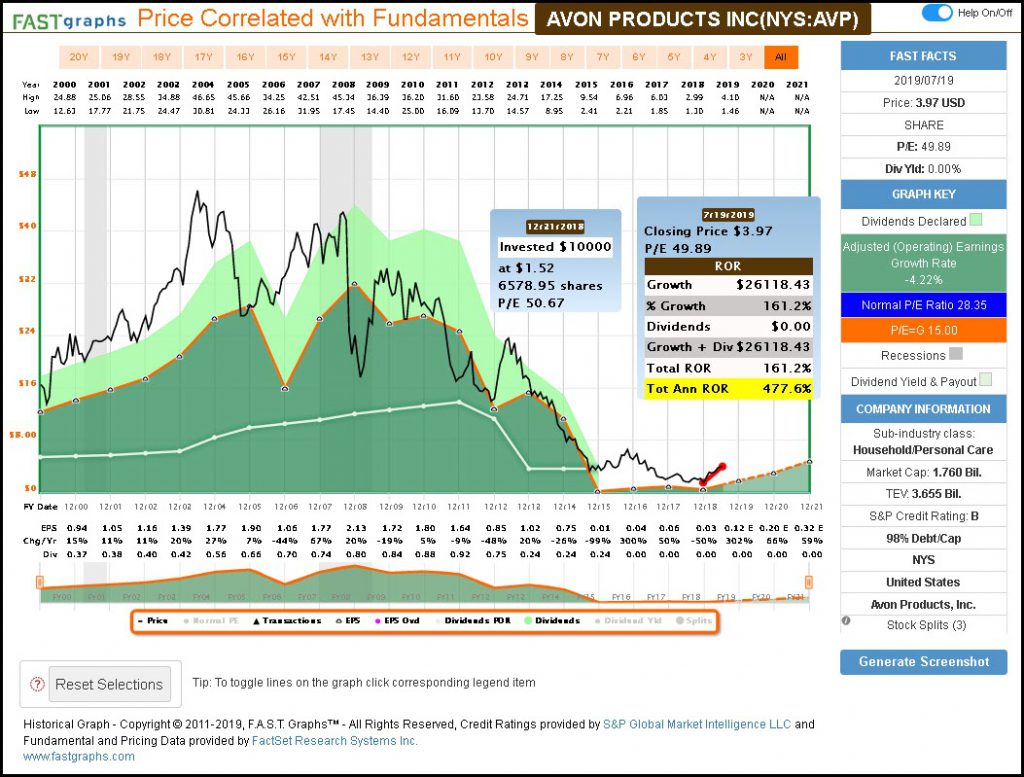

Turnarounds

“Turnaround candidates have been battered, depressed, and often can barely drag themselves into Chapter 11. These are slow growers; these are no growers. These aren’t cyclicals that rebound; these are potential fatalities. Turnarounds stocks can make up lost ground very quickly… The best thing about investing in successful turnarounds is that of all the categories of stocks, their ups and downs are least related to the general market.”

Avon Products Inc. (AVP)

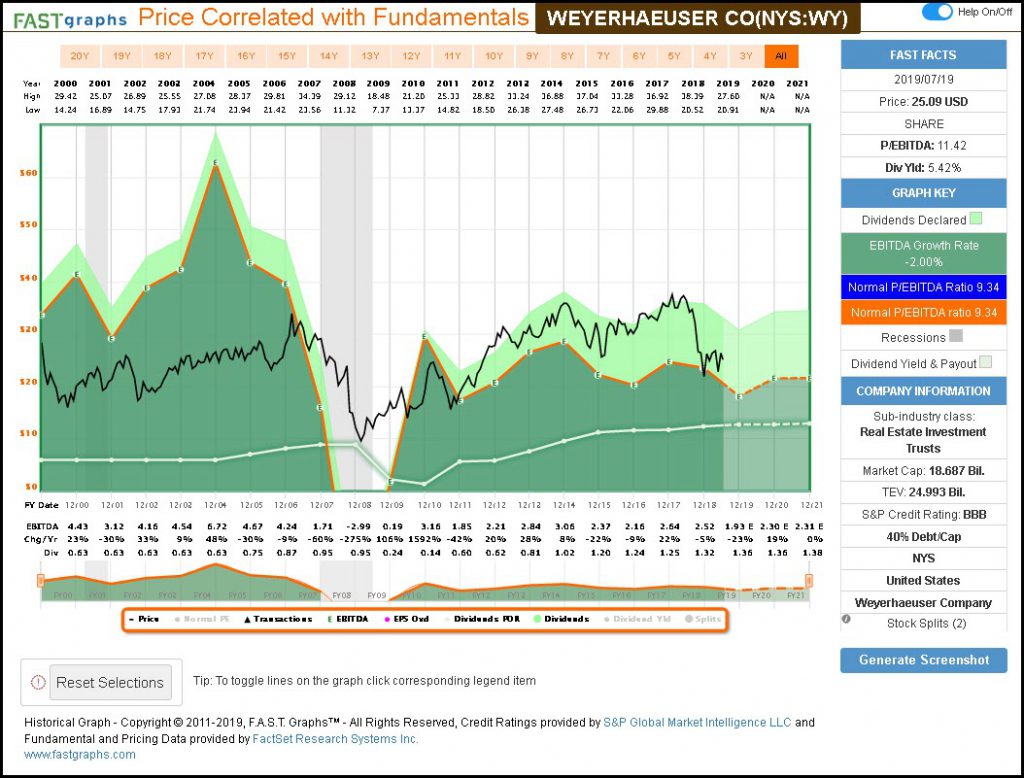

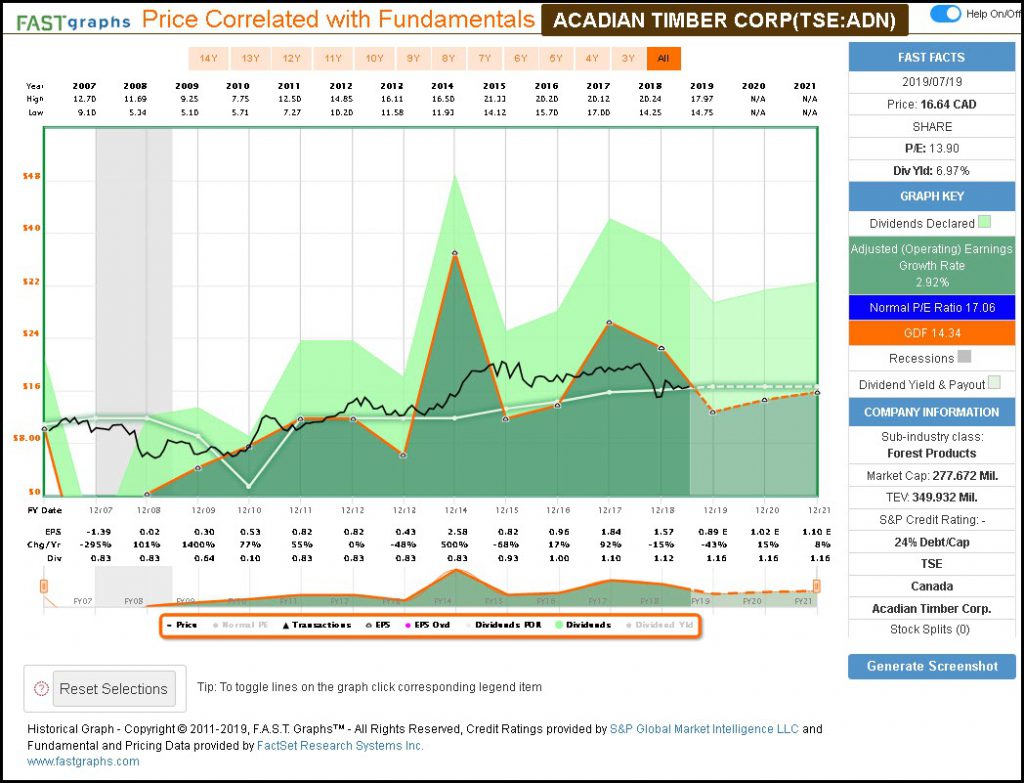

The Asset Plays

“An asset play is any company that is sitting on something valuable that you know about, but that the Wall Street crowd has overlooked. The asset play may be as simple as a pile of cash. Sometimes its real estate.”

Frankly, I had difficulty trying to find examples of asset plays. I think the following two examples would qualify. However, I am not convinced that asset plays any more than deep cyclicals or turnarounds have a place in a prudent and conservatively managed retirement portfolio. In my view, these three categories fall more into the speculation category than the investment category.

Weyerhaeuser Co. (WY)

Acadian Timber Corp (TSE:ADN)

FAST Graphs analyze out loud video: A Dynamic Review Of Peter Lynch’s 6 Categories

In the following video, I will take advantage of the dynamic nature ofFAST Graphs in order to more fully evaluate Peter Lynch’s 6 categories. I am confident that the video will provide deeper insights into the categories of stocks that are appropriate for common stock retirement portfolios.

Summary

Hopefully, it is obvious to the prudent dividend growth investor that not all the 6 general categories of stocks described by Peter Lynch would be appropriate. Personally, I think the prudent dividend growth investor should reject asset plays, turnarounds and most deep cyclicals. However, there are some moderately cyclical companies with great dividend records that could be included in the selection process. Companies like Caterpillar or Boeing (referenced in this article) are just a few examples of what I call moderately cyclical or semi-cyclical companies in contrast to deep cyclicals.

In closing, it is my opinion that retired investors or investors planning for a portfolio to fund their retirement needs should stick with companies that possess the following characteristics: safety, quality, consistency and dividend growth. Since retired investors have less time, and no longer have income from their jobs, they need to be sure that their money works hard for them as they did to earn it in the first place. Slow growers could work if their yields are high enough, stalwarts to include Dividend Aristocrats, are the most obvious and logical source. Fast growers could be utilized selectively; since today’s fast growers often become tomorrow’s dividend growth stocks. However, cyclicals, turnarounds and asset plays seem best left to speculators.

In part 3 I will be discussing diversification strategies. In other words, I will be providing insights into the appropriate number of stocks to hold.

Disclosure: Long SO,PG,LKQ

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.