Introduction

On November 22, 2017, I published an article titled: “Cardinal Health: A Dividend Aristocrat the Risk Is Already Priced In.” At that time, Cardinal Health (CAH) was trading at approximately $56 per share and was paying a dividend of $1.81 representing a dividend yield of about 3.1%. Of course, a lot has changed with the world since that article was published.

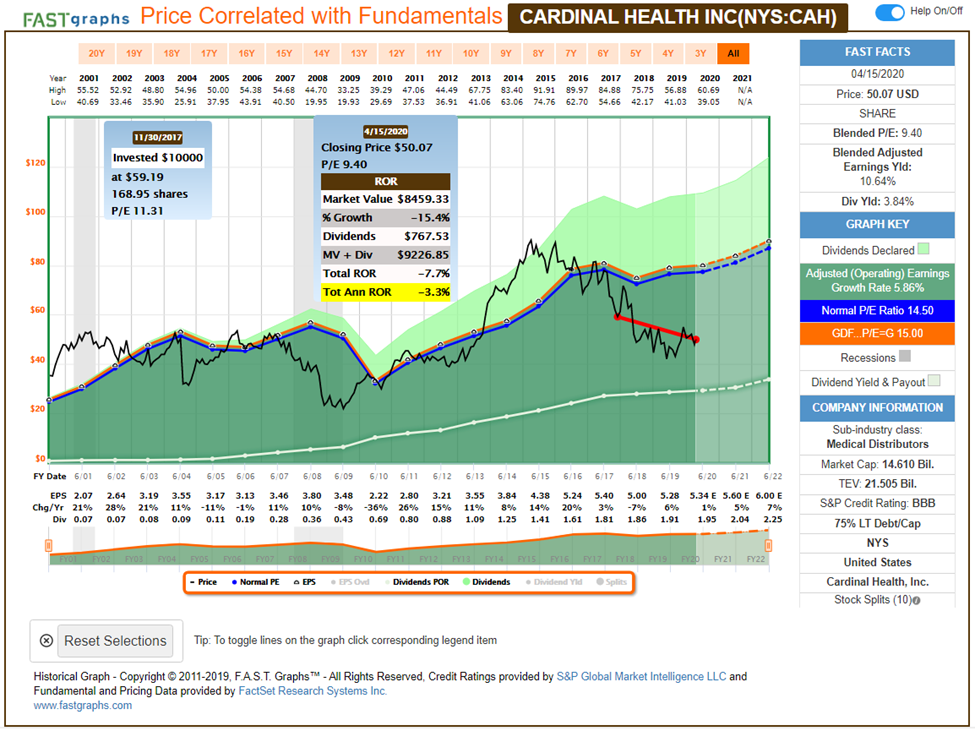

When I posted the original article, I considered Cardinal Health, and I quote “a great business on sale?” In the roughly 2 ½ years since that article was published, the stock price has fallen to $50 per share based on yesterday’s close. The following earnings and price correlated FAST Graph clearly illustrates the results since my original article was published.

Some would consider these results disappointing. However, I am not personally disappointed in the least, because I had invested in Cardinal Health based on my confidence in the company’s dividend and dividend growth potential. So far, Cardinal Health’s dividend has delivered as promised. The following excerpt from my first article articulates my objectives and expectations when it was published – emphasis added is mine:

“To be clear, I believe that Cardinal Health is facing short-term issues that have recently generated weak earnings and cash flows. However, I also believe that the market is currently punishing the company’s stock price more than it deserves. Consequently, I suggest that Cardinal Health is an extremely undervalued and therefore attractive Dividend Aristocrat on sale. Furthermore, I do believe the company possesses above-average long-term growth potential. As a result, I would expect above-average longer-term total returns resulting from growth coupled with P/E ratio expansion. But best of all, Cardinal Health meets my current investment objective because it provides an above-average current dividend yield coupled with above-average dividend growth.

Additionally, it’s also important to point out that my investing strategy and objective is long-term buy-and-hold oriented. As a value investor, I understand that purchasing out-of-favor stocks can often lead to disappointing short-term performance. On the other hand, as a value investor, I also understand that purchasing out-of-favor stocks can lead to enhanced long-term total returns at reduced levels of risk. In other words, my investment horizon is at a minimum 3 to 5 years (a typical business cycle) and preferably forever. As an experienced value investor, I have learned that it takes time for a business to increase its intrinsic value. Frankly, it’s a lot easier to be patient when the business is paying you lavishly while you wait.”

I believe there are two important takeaways from what I stated above that I would like to cast a bright light on. Number one, my primary rationale for investing in the stock was based on my view of the company’s fundamentals. In general, not precisely, the company’s fundamentals have delivered as I expected. The dividend has grown from $1.81 in 2017 to its current rate of $1.95. Consequently, my dividend income has been increasing each year – which was my primary objective.

Number two, I think it’s important to mention that the 2 ½ year holding period is approximately half of what I would consider an appropriate holding period of 5 years or more. What I’m suggesting here is that I clearly understand that stock price action is totally unpredictable. Additionally, it is also very volatile, as indicated by the jagged nature which it has displayed since November 2017 as seen in the above graph.

In contrast to the very nervous looking price action, Cardinal Health’s earnings have advanced nicely and so have their dividend. The orange line on the above graph depicts earnings, and the white line the dividend. Clearly, these are both more consistent and more predictable than trying to guess where the price might go over the short run.

Another reason why I’m not disappointed in Cardinal Health’s performance thus far relates to how well the stock has held up during this horrible black swan event instigated by the coronavirus pandemic. Interestingly, yesterday, April 15, 2020, Zacks Investment Research featured Cardinal Health as their “Bull of the Day.” Zach cited the company’s Q2 earnings results as one reason they featured it as follows:

“Q2 Earnings Impress Investors

Cardinal reported strong fiscal 2020 second quarter results back in February, with its top and bottom line beating the Zacks Consensus Estimate. Total revenue jumped 5% to $39.7 billion, and earnings came to $1.52 per share. Earnings were significantly boosted thanks to the company’s generic pharmaceuticals portfolio performance.

Cardinal’s two business segments, Pharmaceutical and Medical, generated revenue of $35.7 billion and $4 billion, respectively. Investors were pleased with the results, and CAH stock surged 11% the day of the earnings release. Management also raised its full-year 2020 adjusted EPS guidance to a midpoint of $5.30 per share, up from the previous midpoint of $4.97.”

However, given the current circumstance we find ourselves in, I was more excited to read some additional reasons why Zacks was featuring the stock as follows:

“Like other healthcare stocks, CAH is now on many investors’ radar because of its medical equipment supply segment. The company serves as a personal protection equipment (PPE) supplier to hospitals nationwide, and as long as the COVID-19 pandemic persists, demand for these products will remain high.

CAH also offers potential investors value. It only trades at a 9X forward multiple, well below its peers (22X) and the broader market (16X).And, CAH boasts a nearly 4% dividend yield and holds the title of Dividend Aristocrat, having increased its shareholder payout for more than 30 consecutive years.

If you’re an investor searching for a healthcare stock to add to your portfolio, make sure to keep CAH on your shortlist.”

Cardinal Health: FAST Graphs Fundamentals Analyze Out Loud Video

In the following video I will review Cardinal Health from a fundamental perspective based on future expected earnings growth’s potential to raise the stock price and the company’s operating cash flow and free cash flow supporting their dividend going forward.

Summary and Conclusions

As I indicated earlier, Cardinal Health has not produced strong capital appreciation results since I published my first article in November 2017. However, the company has grown its dividend each year as expected and has performed admirably during our recent/current bear market or flash crash. The company’s personal protection equipment segment is seeing increased demand as a result of the pandemic. Consequently, the company has proven to be a very defensive holding during this crisis.

But perhaps most importantly, I think it’s important to reiterate that I consider the holding period since November 2017 to be too short to judge my recommendation by. Nevertheless, we are halfway to what I would consider a minimum holding period, and it will be interesting to see how this recommendation ultimately pans out. Currently, I still consider the company attractively valued with an above-average dividend yield that appears safe. Time will tell. Caveat Emptor – and do your due diligence.

Try FAST Graphs for FREE Today!

SUBSCRIBE to our YouTube Channel

Click here for our Research Articles

Disclosure: Long CAH.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.