Introduction

The idea that interest rates directly affect stock prices is a commonly held belief among many investors. There are some that even go as far as to say that the only reason the stock market is up is because interest rates have been artificially kept low by the Fed. With this article, I’m going to apply some commonsense logic to interest rates and their true impact on stock values.

There are many generalities spouted regarding how interest rates affect stock prices. For example, many argue that there is an inverse relationship between interest rates and stock valuations. The argument suggests that when interest rates are high, fixed income investments such as bonds are more competitive and therefore this diminishes stock values. Conversely, when interest rates are low, fixed income is less competitive and therefore stock valuations will rise.

Although there is some validity in the above assertions, historical reality suggests that these relationships only work until they don’t. The reason this is true is because there are many factors that will affect the value of stocks with interest rates being only one.

Another commonly held belief about interest rates and stock values goes something like this: when interest rates go up, the discount rate will increase to reflect the increase in interest rates. Since stocks get their value by discounting future income streams to the present value, the higher discount rate reduces the value of those income streams. Therefore, the stock price will decline because the present value of that income stream is now lower. This theory is typically followed by the notion that when interest rates increase, multiples (P/E ratios, etc.) will decline, which also causes the stock to decline.

There are many variations to the themes presented above, however, they all pretty much ascribe to the theory that there is a direct inverse relationship between valuation and interest rates. Nevertheless, my experience suggests that these theories only work in a perfect market environment. However, the market is very rarely – if ever – perfectly aligned with economic theories.

Additionally, economic and/or investing theory can be applied either generally or specifically. By generally, I’m referring to the effects that things like interest rates would have on the overall stock market or stocks in general and on other macro factors such as inflation and GDP growth, etc. However, I personally tend to be more focused on specific or individual stocks on the theory that it’s a market of stocks not a stock market. In this regard, the effects of interest rates can be significantly different company by company.

The General Or Macro View: Presented By My Friend And Associate Dividend Sensei

Dividend Sensei is one of my partners in The Dividend Kings marketplace service on Seeking Alpha. However, he also authors articles on his own site where he recently presented an article on the macro titled: “The Surprising Truth About Interest Rate Investors Need To Know.” With his permission, I offer the following excerpts where he looked at several interesting aspects regarding the relevance of interest rates as they apply to the market in general.

Dividend Sensei starts out by stating:

“The Surprising Truth About Interest Rate Investors Need to Know”

A popular idea that’s been making the financial media rounds for years is that central bank money printing has inflated asset bubbles around the world and potentially set us up for the mother of all crashes in the next few years.

This is predicated on the notion that interest rates, at their lowest levels in history, have nowhere to go but up, which could pop the unsustainable market bubble we’re now in.

The shocking truth about stocks and interest rates is far different than most in the media know or tell you.

So, let’s look at three crucial facts about the longest and most profitable bull market in history, including what’s likely in store for your portfolio in the years to come.

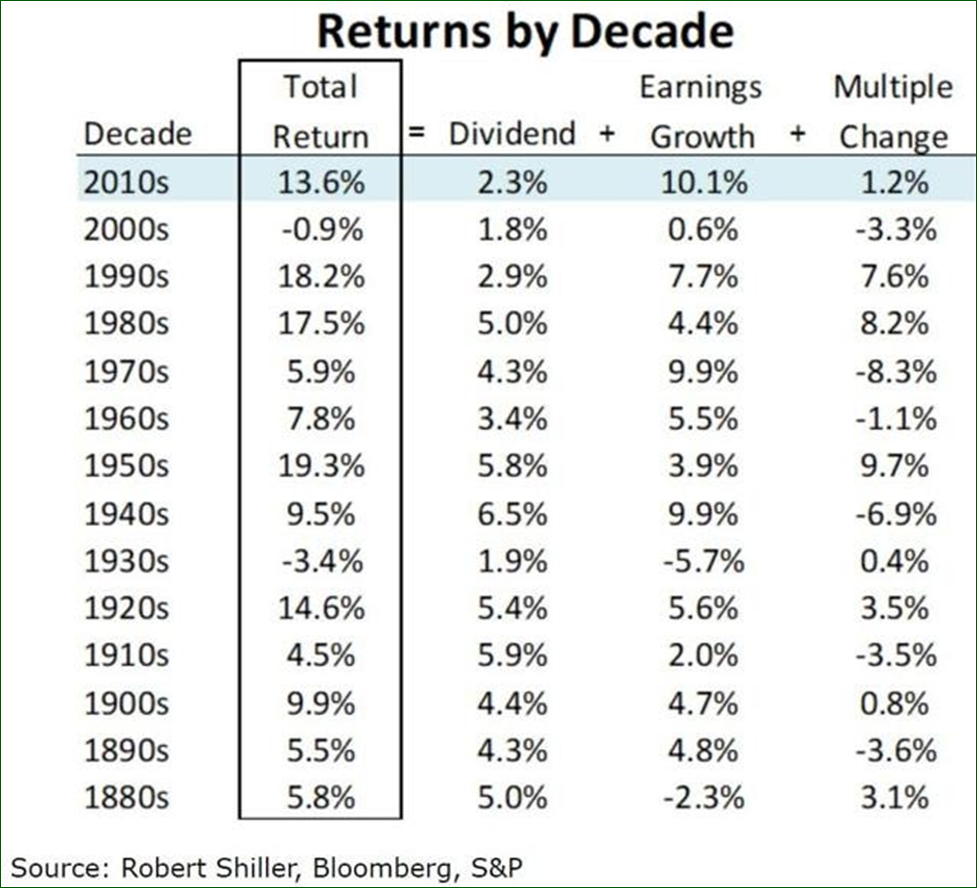

Fact One: The 2010’s Bull Market Was NOT A Result of A Low Rate Bubble

The 13.6% CAGR total returns seen during the previous decade may feel unsustainable but they were actually 88% justified by earnings growth and dividends.

It was the 1980s and 1990s when multiple expansion drove bubbles that eventually resulted in stocks becoming 66% historically overvalued in 2000 (including a forward PE of 27.2 vs 16.3 25-year average).

What about the idea that low rates induced over $5 trillion in buybacks that drove most of that EPS growth? According to Ed Yardeni, using Federal Reserve data, 66% of buybacks offset stock-based compensation.

How much of that 10.2% EPS growth was a result of net buybacks? 1.3% or 12%.

So even if you want to blame the Fed’s QE (plus other central bank QE) for buybacks entirely then low rates and buybacks accounted for just 18% of annual returns over the last decade. 72% of the rally was justified by fundamentals. (Note to readers: the bold emphasis added is mine).

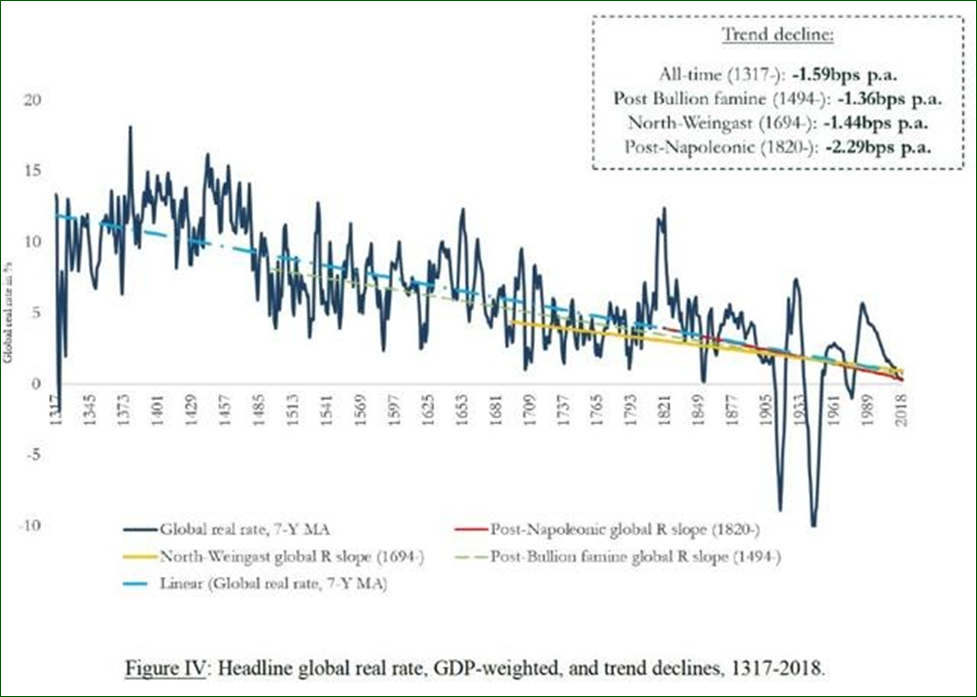

Fact Two: Interest Rates Have Been Falling For Centuries And Negative Rates Are Actually Historically Normal

One of the most common beliefs among the financial media is that today a world of negative rates is unprecedented and thus creates dangerous asset bubbles everywhere you look, including in stocks.

But the truth is that long-term rates have been falling not just for decades (since peaking in 1981 at 16% on the 10-year Treasury yield), but for centuries.

(Source: Bank of England)

In fact, the trend in long-term interest rates has been pretty steadily declining for 700 years. That’s throughout a very complex and often disastrous history of wars, money printing and governments borrowing heavily to finance military campaigns.”

However, before I go on presenting Dividend Sensei’s ideas, I want to highlight that this next paragraph may be the most profound and important thing that he says. In it, he points out the importance that productivity has played towards economic growth and prosperity in recent times:

“What explains this nearly Millennium long trend? Most likely because the world’s economy has gotten so much more productive and thus the amount of savings available to the people of the world is much greater.

Factor in more stable governments and economies, and more savings looking for safe places to invest for income (bonds) naturally drives interest rates (the cost of money) lower over time.”

Dividend Sensei then goes on to produce a very interesting fact about interest rates on the macro level:

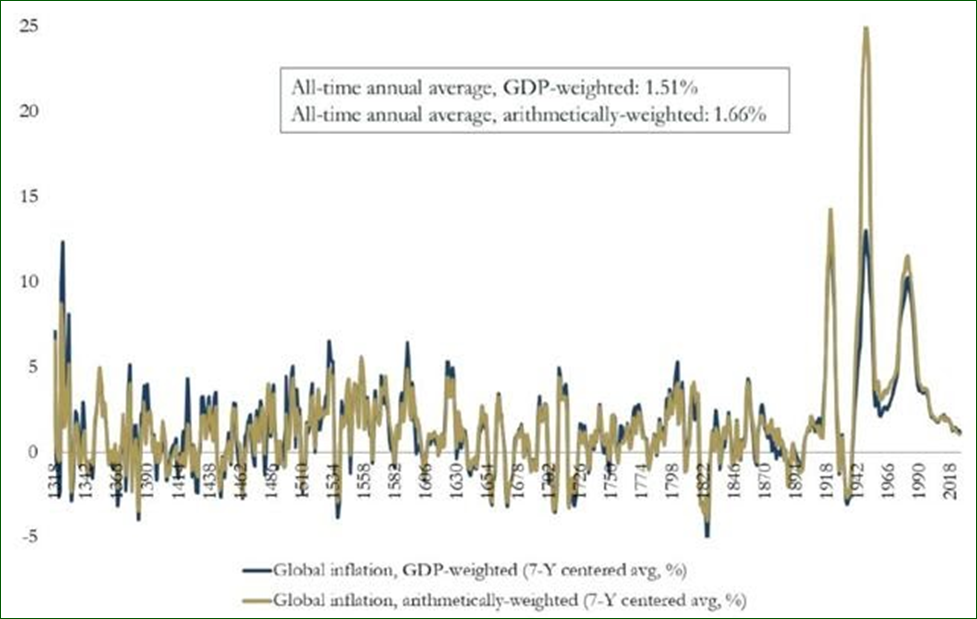

“Another common belief is that the “normal” interest rate is much higher than it is today, and thus long-term rates have nowhere to go but up.

(Source: Bank of England)

Adjusted for inflation, long-term rates have averaged 1.5% to 1.7% over time, and that includes centuries in which long-term rates were in the double-digits. It’s possible that in the future the average inflation-adjusted interest rate might be closer to 0% to 1%, implying 2% to 3% long-term yields on US treasuries might indeed be the “new normal.”

OK, so maybe real interest rates haven’t been super high in the past and might not be where we return to. But surely trillions in negative-yielding debt is crazy right? Unprecedented and dangerous and a huge risk for a future crash correct? “

Finally, Dividend Sensei produces a third fact that many investors either are not aware of or have not considered:

“Fact Three: Low Rates Can Eventually Induce Bubbles And You Should Avoid FOMC/Bubble Thinking

Just because long-term interest rates might remain lower forever doesn’t necessarily mean that stock investors are off the hook when it comes to valuations.

There is more to Dividend Sensei’s article and his complete work can be found here.

It Is A Market Of Stocks: The Micro View:

With the remainder of this article and the accompanying FAST Graph video I will be discussing the effects that interest rates have had on several Dow Jones’ stocks over the past two decades which include our last two recessions.

The general theories that I presented in the introduction to this article are ones that I ascribe to – all things being equal. However, with economics, all things are hardly ever equal. In other words, in a perfectly rational economic environment with everything equal, an inverse relationship between stock values and interest rates would make perfect sense and probably hold true in the real world.

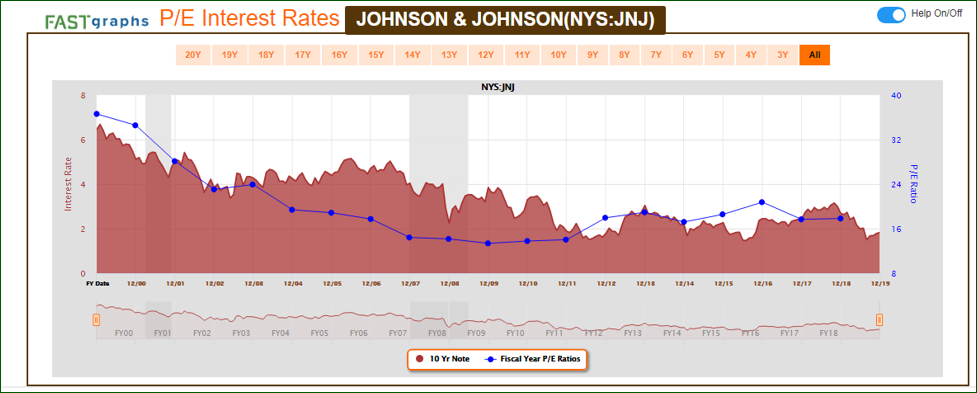

Therefore, and in order to be able to test that theory, I developed a “P/E Interest Rate” graphic that graphed the 10-year treasury note and then the year-end P/E ratio relative to those interest rates for each individual company. Understand that I was expecting to see the two metrics move in opposite directions or inversely. In other words, when interest rates were rising, I expected to see the P/E ratio of the individual stock dropping – and vice versa. At least, that’s what the theory that’s been described so far in this article would suggest.

However, if you look at the following P/E ratio correlated to interest rate graph on Johnson & Johnson (JNJ) you see just the opposite of what should be expected. Both interest rates (the burgundy shaded area) since the beginning of calendar year 2000 and the year-end P/E ratios (the dark blue line) of Johnson & Johnson have moved downward almost in lockstep. This defies economic theory and begs the question why?

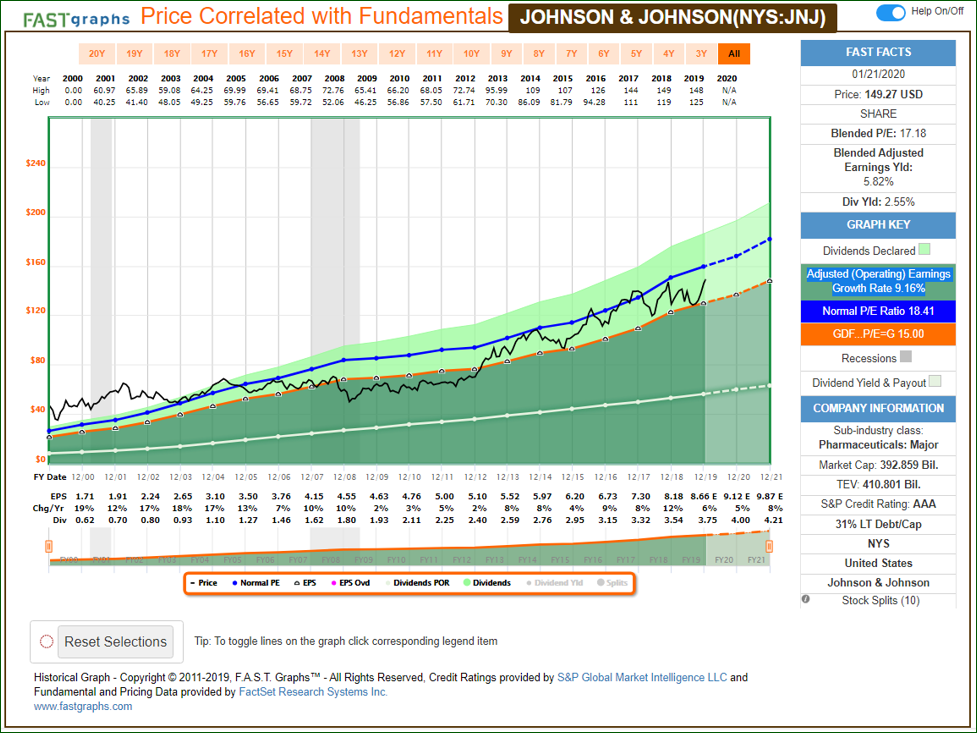

In order to answer the question of why, all you need to do is look at the earnings and price correlated graph to discover that valuation eclipsed the interest rate relationship. However, this also defies conventional wisdom, because, Johnson & Johnson’s P/E ratio over these last two decades was highest in calendar year 2000 at precisely the same time that interest rates were highest. Clearly, other factors were at play, and those other factors dominated the effect that interest rates should have had.

The Real Drivers Of Long-Term Stock Prices

The intrinsic value of a common stock and its subsequent long-term performance will be functionally related to the specific operating results that the individual company achieves. Generalized exogenous factors such as the level of interest rates might be a minor determinant of what the company’s operating results achievements might eventually be. However, that is far from saying that the company’s performance is determined by the level of interest rates. They may be a minor contributing factor, but they are hardly a major factor.

Nevertheless, there are many who believe that stock prices are being artificially inflated because the Fed is artificially keeping interest rates low. To that point, I would also add that the government can apply influencers to economic growth or stability, but they do not drive or control the economy in general, or more to the point, the results of specific companies.

Moreover, in addition to interest rates, government can also apply influence through tax policy (levels of taxation), and with strict or lax regulatory policy. Each of these things can make it harder (less profitable) or easier for individual businesses to make money. However, it is the actual attractiveness of the products and services that each individual business provides that are the major drivers of their growth and future success.

Amazon and Interest Rates

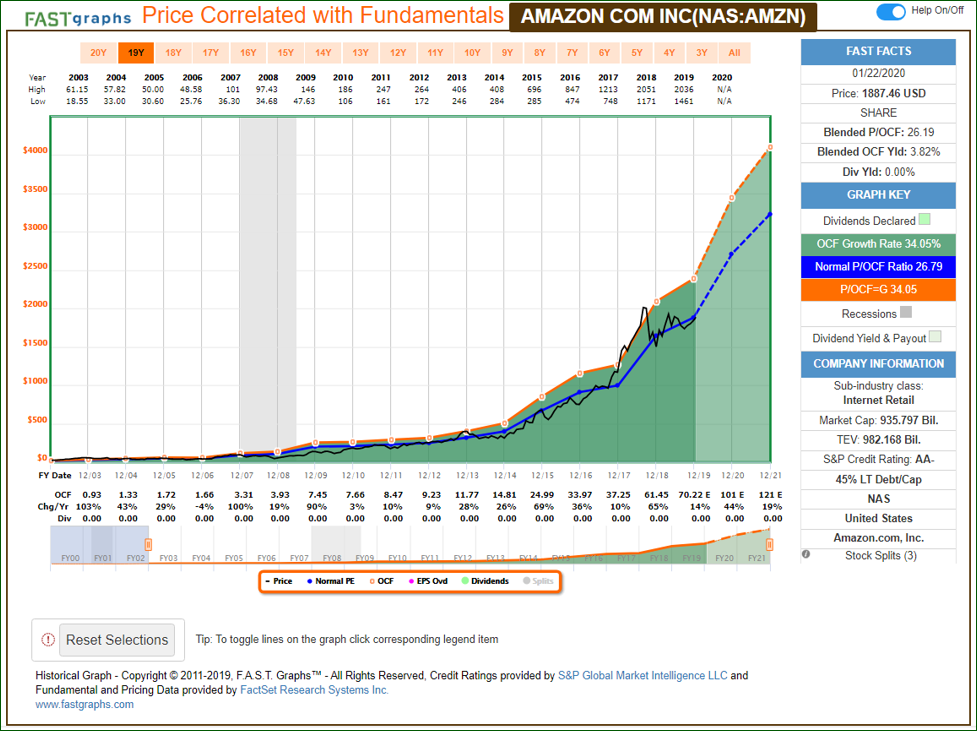

For example, I would argue that interest rates had very little to do with the success of Amazon (AMZN) as a growth stock. Since 2003, Amazon has grown their operating cash flows at an annualized rate of 34%. The operating cash flow and price correlated graph below illustrates that Amazon’s operating results drove their stock price higher over this timeframe. When you compare that to the average company as depicted by the S&P 500, clearly illustrates that Amazon generated its own unique returns independent of general economic activity.

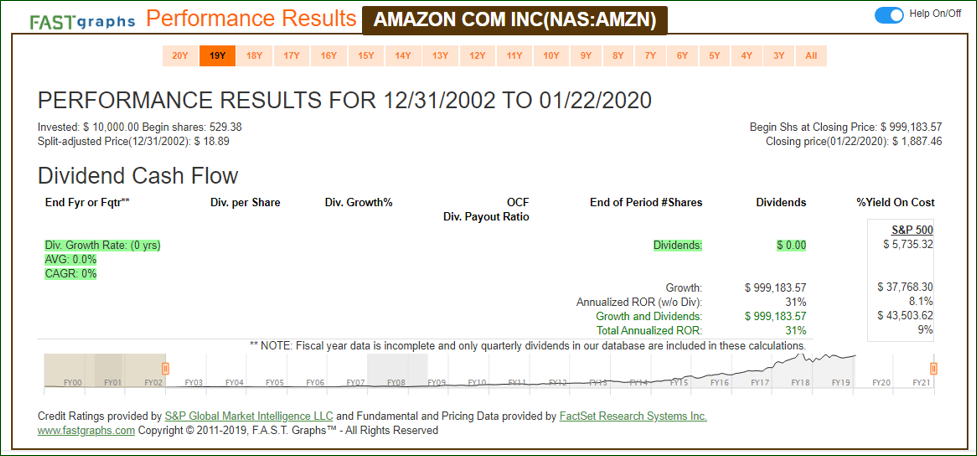

In correlation with that growth of cash flow, Amazon shareholders earned just under $1 million of growth for every $10,000 they invested since 2003. Nevertheless, even though Amazon has 45% long-term debt to capital, I would argue that interest rates played but a very minor role in the company success.

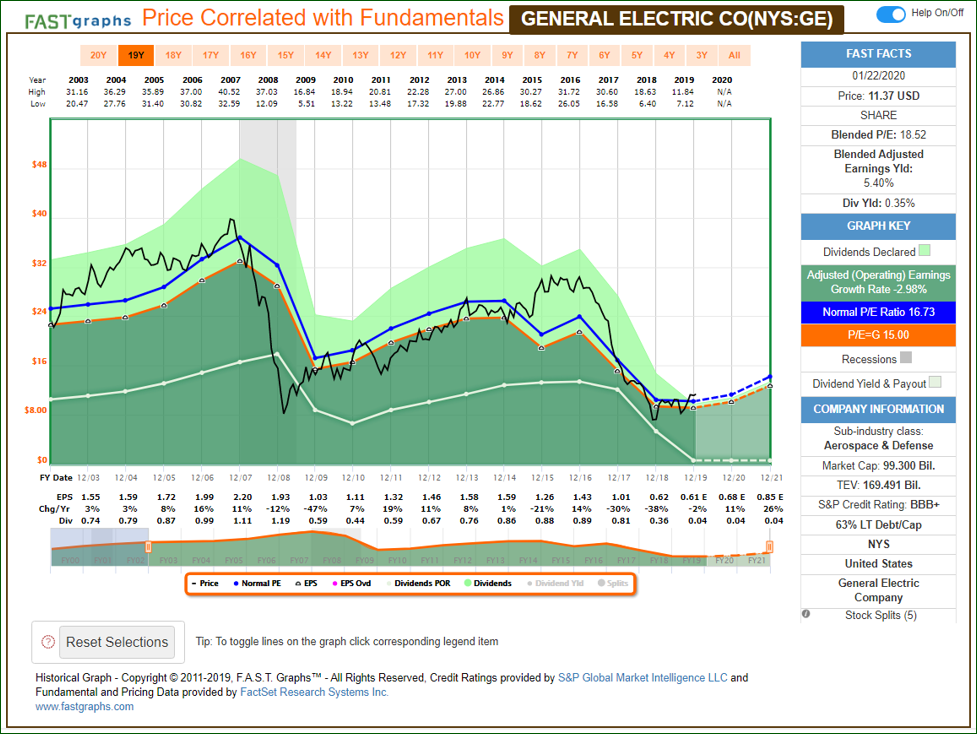

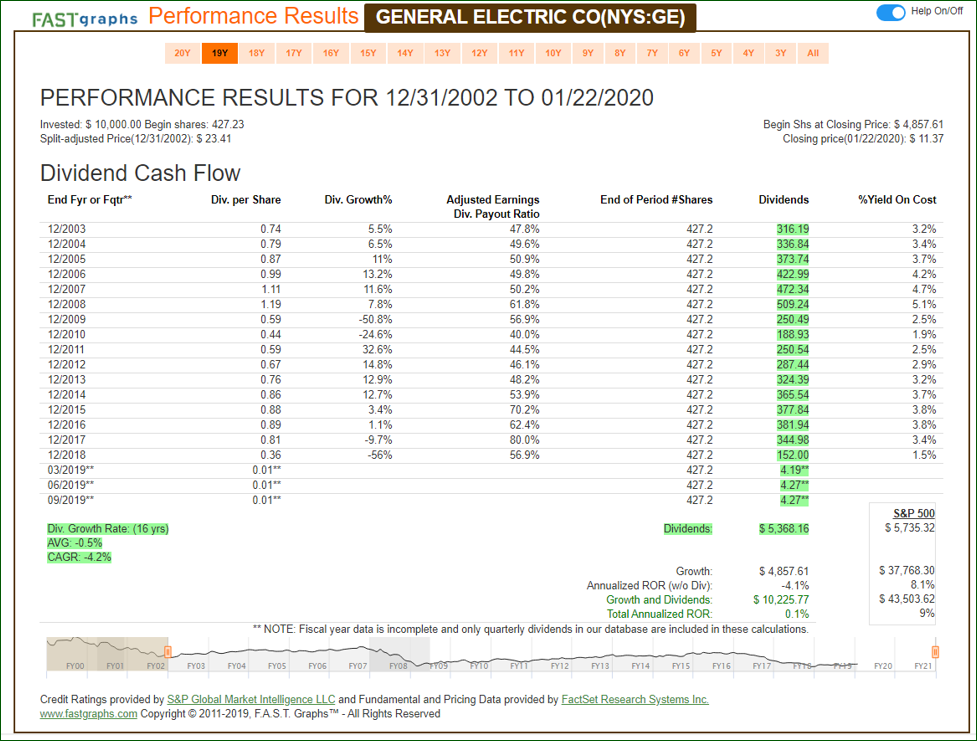

General Electric and Interest Rates

In contrast to the incredible success of Amazon, General Electric (GE) produced entirely different results as a business and returns to shareholders. Just as I pointed out with Amazon, I do not think interest rates had much to do with General Electric’s lack of success. Both companies featured here, were operating in what I would describe as a perfect interest rate scenario. Amazon grew in that environment, while General Electric shrunk.

The value of General Electric’s stock in the associated returns to shareholders have been abysmal since 2003 despite interest rates. However, as an unrelated aside, long-term shareholders would have broken even thanks to General Electric’s dividends even though they were cut no less than four times.

FAST Graphs Analyze Out Loud Video: Interest Rates and Stock Values

In the following video, I will be illustrating that the commonly held theory that there is an inverse relationship between interest rates and stock values has not been valid over the past two decades. In order to illustrate that I will be featuring the P/E ratio versus interest rates on several Dow Jones Industrial Average stocks.

If the theory that stock values and interest rates moved inversely to each other were true, the graphs would show interest rates falling since calendar year 2000 while stock values (P/E ratios) increased. Therefore, I strongly suggest that you check out the video and see “Interest Rates and Stock Values Truth Be Told.”

Summary and Conclusions

First and foremost, this article was written to argue in favor of thinking about your specific investments in contrast to worrying about generalities or macro factors such as the level of interest rates. As has been most often throughout my career in the financial services industry, my best lessons were taught by some of the greatest investors that ever walked the planet. My lack of concern over interest rates was taught by the venerable Warren Buffett as follows:

“If we find a company we like, the level of the market will not really impact our decisions. We will decide company by company. We spend essentially no time thinking about macroeconomic factors. In other words, if somebody handed us a prediction by the most revered intellectual on the subject, with figures for unemployment or interest rates, or whatever it might be for the next two years, we would not pay any attention to it. We simply try to focus on businesses that we think we understand and where we like the price and management. Warren Buffett “

If we are to behave as prudent investors, I do believe that we should consider most everything we can when evaluating the desirability of an investment. However, I further believe as Warren Buffett suggested above, then it makes more sense to worry about the individual business than it does macro events or factors that are unpredictable and for the most part out of each investor’s control.

Nevertheless, with that said, there are certain industries that are more either vulnerable or benefited by interest rate levels. Consequently, if I was evaluating a business in those industries, it would only make sense to consider interest rates. For example, companies in the housing sector would find it difficult to grow in a rising rate environment. The same might be true for autos because both home and automobile sales are highly dependent on borrowing money.

On the other hand, companies that are debt free might not see their businesses impacted too much by interest rates. In these cases, interest rates might only impact spending of their customers, especially those customers that are heavily reliant on credit for their purchases. But the primary point is that interest rates are simply another factor that should be appropriately considered when evaluating individual businesses. However, they are not a dominating factor as many people believe.

Sign up for your 14-day free trial to FAST Graphs: www.fastgraphs.com

Disclosure: Long JNJ

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.