Introduction

The Non-Energy Minerals Sector is mostly comprised of very cyclical and typically commodity-based companies. Consequently, very few companies in this sector offer the consistency and predictability that prudent and/or conservative investors might require. As a result, I personally tend to eschew investing in companies in this sector. In addition to the general cyclical nature of their businesses, income seeking investors might also note the unpredictability and/or reliability of their dividend income streams.

Nevertheless, this series of articles is presented with the objective of covering all the sectors that FactSet reports on. Therefore, it is only appropriate that I cover all the sectors comprised of individual stocks. However, I do want to be clear that this sector is not one that I consider appropriate for prudent long-term investing. With that said, more active investors might find trading opportunities in this sector. But I believe prudent long-term buy-and-hold investors will be hard-pressed to find anything that suits their goals or objectives.

A Sector By Sector Review

This is Part 13 of a series where I have conducted a simple screening looking for value over the overall market based on industry classifications and subindustry classifications reported by FactSet Research Systems, Inc.

In part 1 found here I covered the Consumer Services Sector. In part 2 found here I covered the Communication Sector. In part 3 found here I covered the Consumer Durables Sector and its many diverse subsectors. In part 4 found here I covered Consumer Nondurables. In part 5 found here I covered companies in the Consumer Services Sector. In part 6 found here I covered the Distribution Services Sector. In part 7 found here I covered the Electronic Technology Sector. In part 8 found here I covered the Energy Minerals Sector. In part 9 found here I covered the Finance Sector. In part 10 found here I covered the Health Services Sector. In part 11 found here I covered the Health Technology Sector. In part 12 found here I covered the Industrial Services Sector.

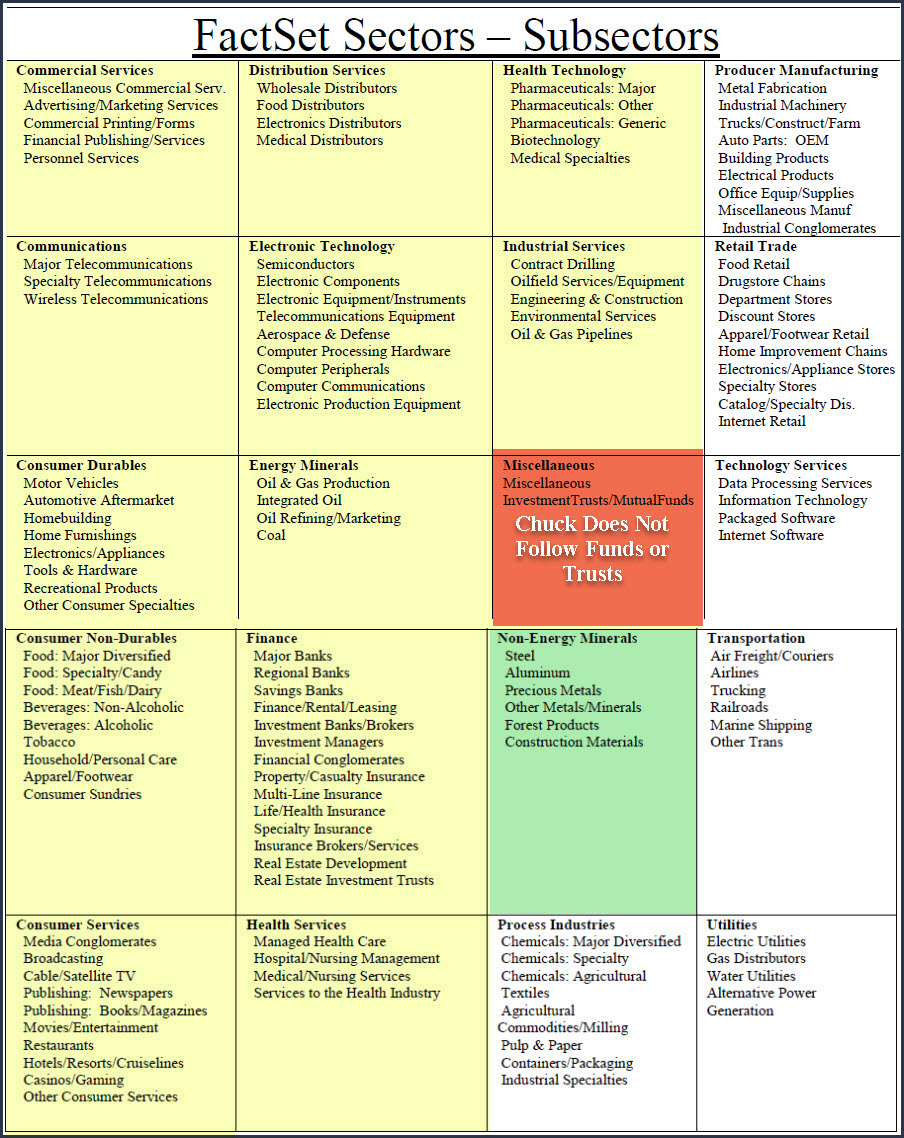

I am skipping the Miscellaneous Sector that consists of Investment Trusts/Mutual Funds as I do not follow these. I have that sector highlighted red on the list.

In this part 13 I will be covering the Non-Energy Minerals Sector.

In each article in this series, I have been providing a listing of screened research candidates from each of the following industry sectors. However, due to the cyclical nature of most of the companies within this sector, I do not personally consider any of the research candidates. Instead, I offer them as prime examples of how different individual stocks can be relative to the general market. The sector I’m covering in this article is marked in green:

Sector 13: Non-Energy Minerals

Steel

Aluminum

Precious Metals

Other Metals/Minerals

Forest Products

Construction Materials

A Simple Valuation and Quality Screening Process

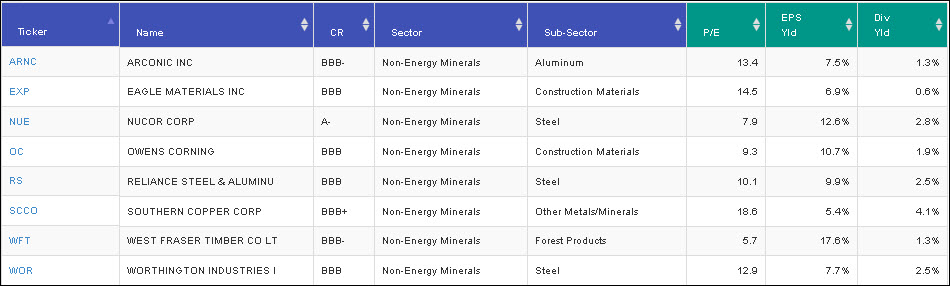

With this series of articles, I will be presenting a screening of companies that have become attractively valued primarily as a result of the bearish market activities experienced in 2018 from each of the above sectors. I will be applying a rather simple valuation and quality-oriented screen across each of the sectors. First, I have screened for investment-grade S&P credit ratings of BBB- or above. Next, I have screened for low valuations based on P/E ratios between 2 and 17. Finally, I have screened for long-term debt to capital no greater than 70%.

By keeping my screen simple, and at the same time rather broad, I have been able to identify attractively valued research candidates that I might have overlooked through a more rigorous screening process. In other words, I’m looking for fresh ideas that I might have previously been overlooking. Nevertheless, I consider most companies in this sector too cyclical to be considered long-term buy-and-hold investments. The only exceptions in this sector review might be Owens Corning and to a lesser extent Worthington Industries Inc. Consequently, I only offer these mostly cyclical companies in order to illustrate the diversity of individual stocks relative to the overall market.

Portfolio Review: Non-Energy Minerals Sector: 8 Diverse Cyclical Companies

FAST Graphs Screenshots of the 8 Diverse Cyclical Companies

The following screenshots provide a quick look at each of the 8 cyclical companies screened out of over 19,000 possibilities. However, there are only 1,413 companies categorized as Non-Energy Minerals, and I am not comfortable presenting any of them as potential attractively valued research candidates. This sector is too cyclical for my personal taste. Nevertheless, a primary objective of this series of articles is to illustrate the reality that it is a market of stocks and not a stock market. Therefore, I am covering all the sectors representing individual stocks by FactSet. Consequently, individual stocks should not be evaluated with the same broad brush.

The company descriptions are provided courtesy of the Wall Street Journal. In the FAST Graphs analyze out loud video that follows the screenshots, I will provide additional details and thoughts on why I personally tend to avoid this sector, as well as the potential negatives of each of these cyclical companies.

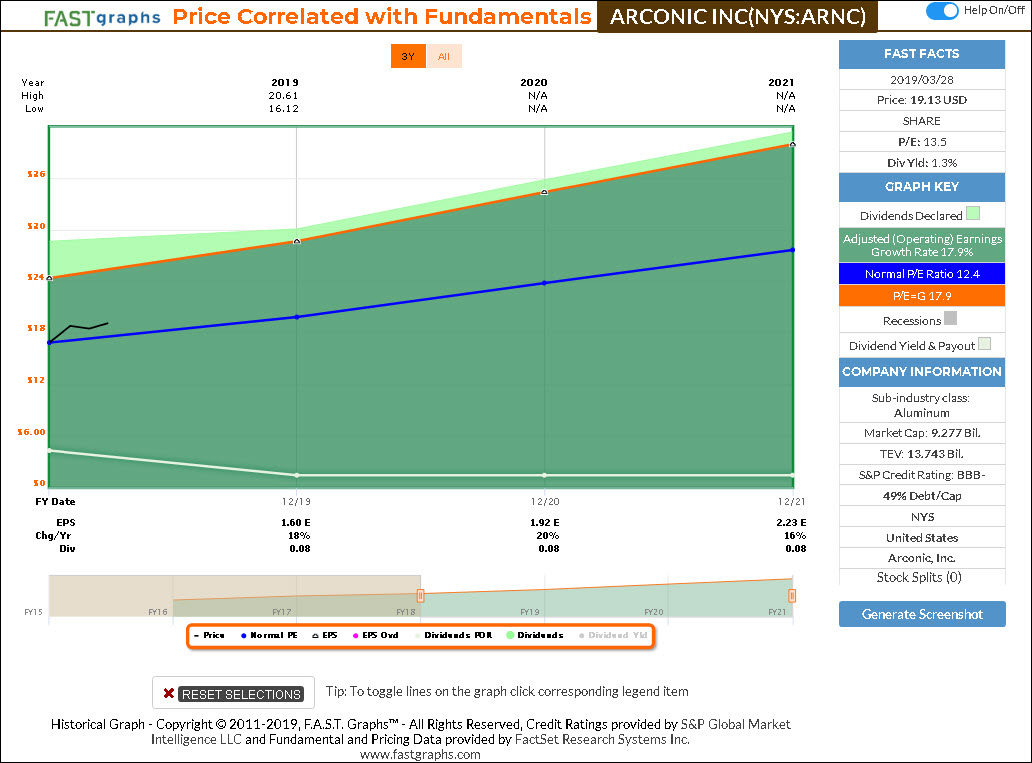

Arconic Inc (ARNC)

Arconic, Inc. engages in the manufacture and engineering of lightweight metals. It operates through the following segments: Global Rolled Products; Engineered Products and Solutions; and Transportation and Construction Solutions. The Global Rolled Products segment produces aluminum sheet and plate. The Engineered Products and Solutions segment include fastening systems (titanium, steel, and nickel superalloys); seamless rolled rings (mostly nickel superalloys); investment castings (nickel superalloys, titanium, and aluminum); and extruded, machined and formed aircraft parts (titanium and aluminum). The Transportation and Construction Solutions segment offers aluminum structural systems, architectural extrusions, and forged aluminum commercial vehicle wheels.

The company was founded in 1888 and is headquartered in New York, NY.

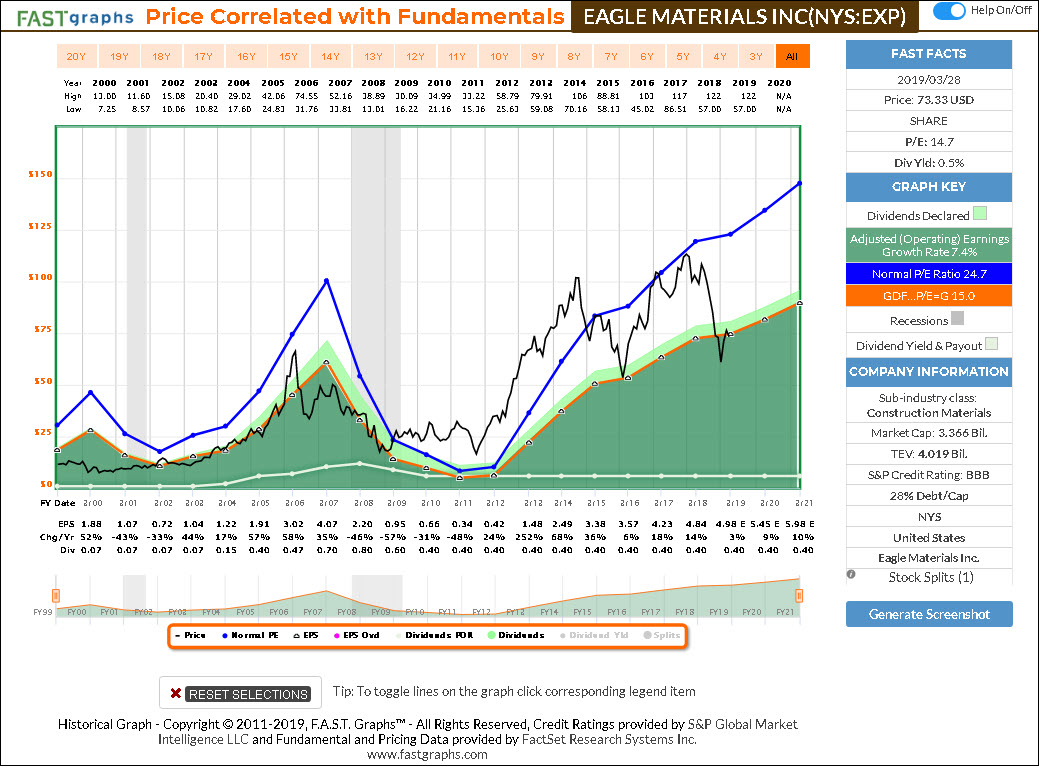

Eagle Materials Inc (EXP)

Eagle Materials, Inc. engaged in the manufacture and distribution of gypsum wallboard and cement. It operates through the following segments: Cement, Gypsum Wallboard, Recycled Paperboard, Oil and Gas Proppants, and Concrete and Aggregates. The Cement segment consists of raw material used in the production of portland cement which is calcium carbonate in the form of limestone.

The Gypsum Wallboard segment mines and extracts natural gypsum rock, which is used in the manufacture of gypsum wallboard. The Recycled Paperboard segment includes paper fiber, water and paper chemicals and these recycled paperboards are sold to gypsum wallboard manufacturers. The Oil and Gas Proppants owns frac sand mines, wet processing plants and drying facilities. The Concrete and Aggregates segment offers ready mix concrete, a building material which is used in construction.

The company was founded in 1963 and is headquartered in Dallas, TX.

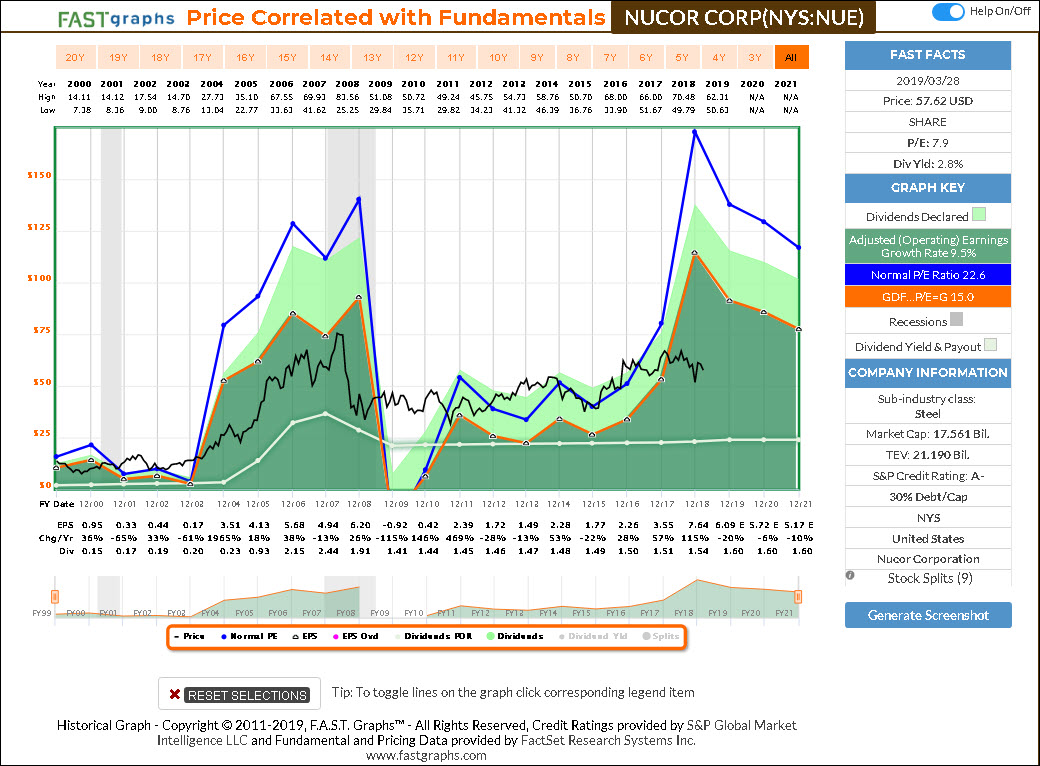

Nucor Corp (NUE)

Nucor Corp. engages in the manufacturing of steel and steel products. It operates through the following segments: Steel Mills, Steel Products, and Raw Materials. The Steel Mills segment comprises carbon and alloy steel in sheet, bars, structural and plate; steel trading businesses; rebar distribution businesses; and Nucor’s equity method investments.

The Steel Products segment includes steel joists and joist girders, steel deck, fabricated concrete reinforcing steel, cold finished steel, steel fasteners, metal building systems, steel grating, tubular products businesses, piling products business, and wire and wire mesh. The Raw Materials segment consists direct reduced iron, and ferrous and nonferrous metals.

The company was founded by Ransom E. Olds in 1905 and is headquartered in Charlotte, NC.

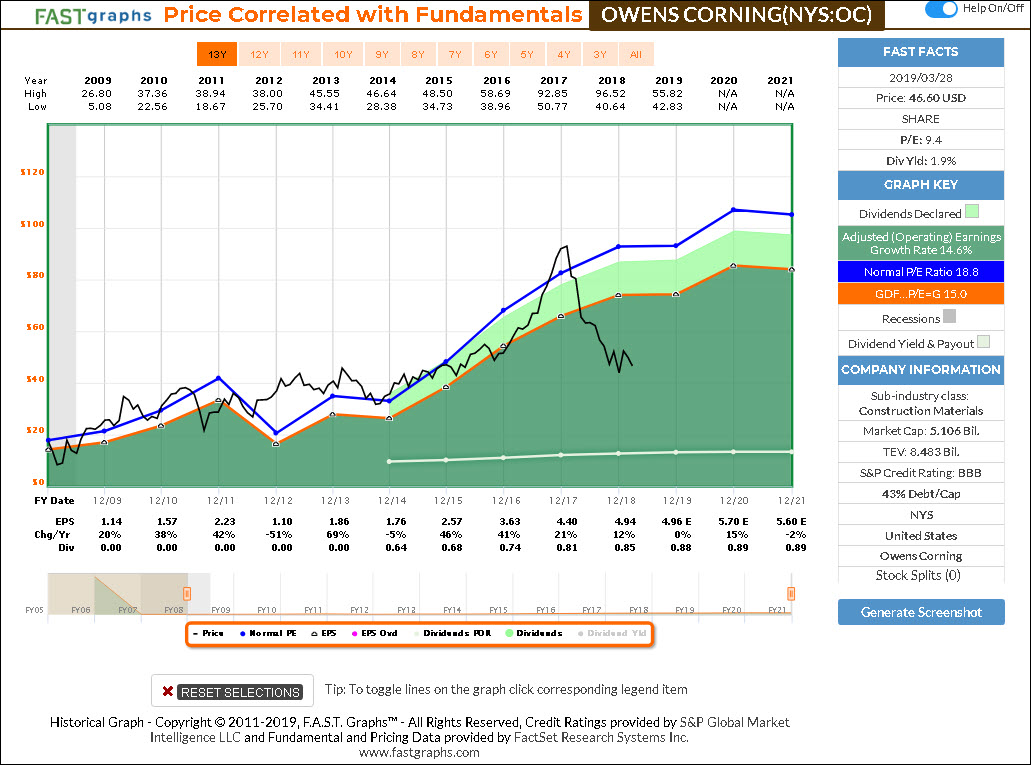

Owens Corning (OC)

Owens Corning engages in the development, manufacture, and marketing of insulation, roofing, and fiberglass composites. It operates through the following segments: Composites, Insulation, and Roofing. The Composites segment manufactures, fabricates, and sells glass reinforcements in the form of fiber, and also includes vertically integrated downstream activities.

The Insulation segment provides insulating products which help customers conserve energy; provide improved acoustical performance; and offer convenience of installation and use. The Roofing segment offers laminate and strip asphalt roofing shingles and other products including oxidized asphalt and roofing accessories.

The company was founded on October 31, 1938 and is headquartered in Toledo, OH.

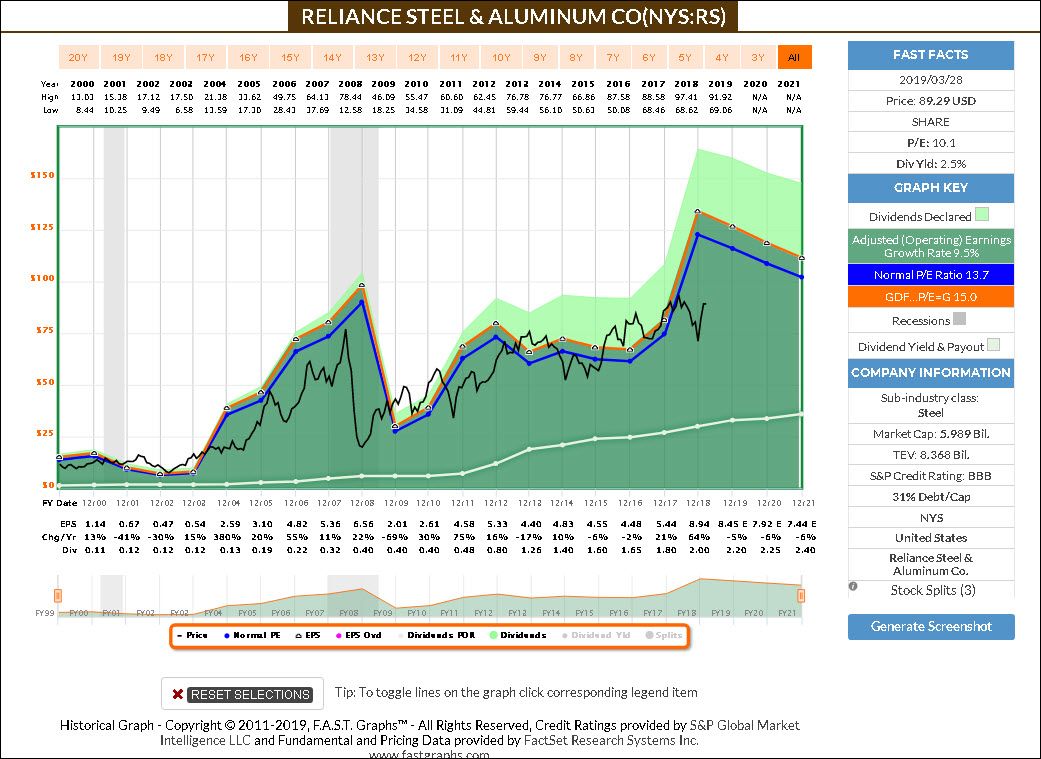

Reliance Steel & Aluminum (RS)

Reliance Steel & Aluminum Co. operate a metals service center network, which provides value added metals processing services and distributes metal products. Its products include alloy, aluminum, brass, copper, carbon steel, stainless steel, titanium, and specialty steel products. It offers beam, bar and tube cutting; bending, forming and shaping; coil and flat roll processing; machining and manufacturing; plate and sheet cutting and burning ; and other special services.

The company was founded by Thomas J. Neilan on February 3, 1939 and is headquartered in Los Angeles, CA.

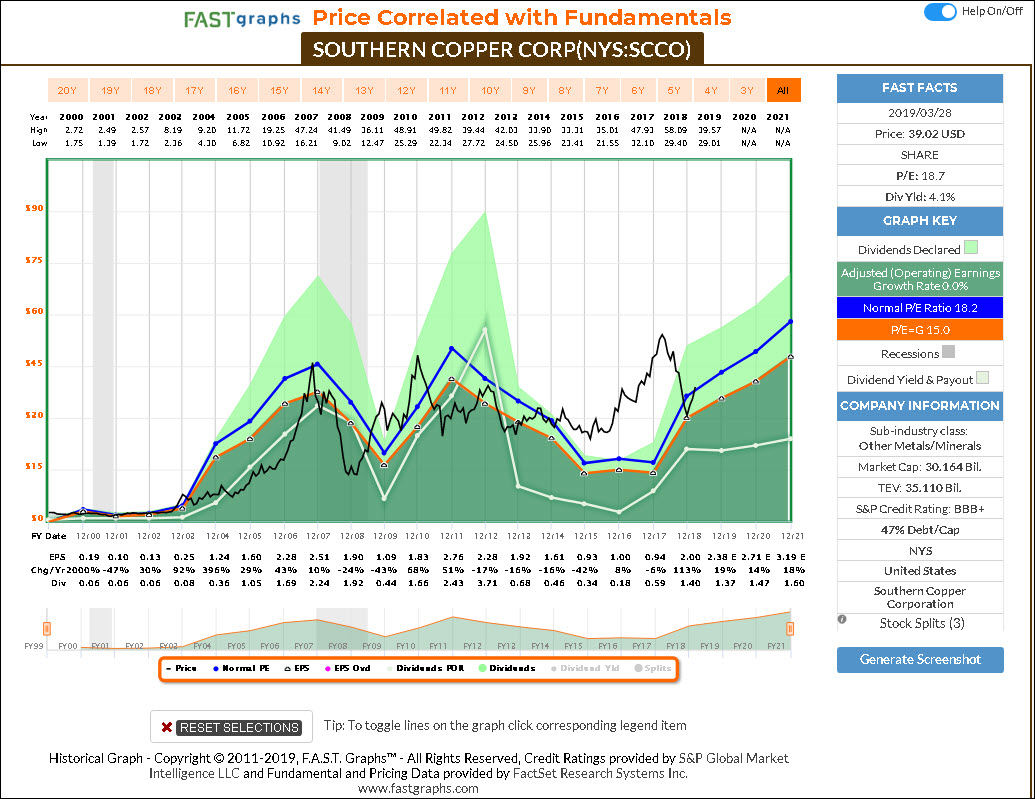

Southern Copper Corp (SCCO)

Southern Copper Corp. engages in the development, production, and exploration of copper, molybdenum, zinc, and silver. It operates through the following segments: Peruvian Operations, Mexican Open-Pit Operations, and Mexican Underground Mining Operations. The Peruvian Operations segment focuses on the Toquepala and Cuajone mine complexes and the smelting and refining plants, including a precious metals plant, industrial railroad, and port facilities that service both mines.

The Mexican Open-Pit Operations segment consists of La Caridad and Buenavista mine complexes and the smelting and refining plants, including a precious metals plant and a copper rod plant and support facilities that service both mines. The Mexican Underground Mining Operations segment includes underground mines that produce zinc, copper, lead, silver and gold, a coal mine that produces coal and coke, and a zinc refinery.

The company was founded on December 12, 1952 and is headquartered in Phoenix, AZ.

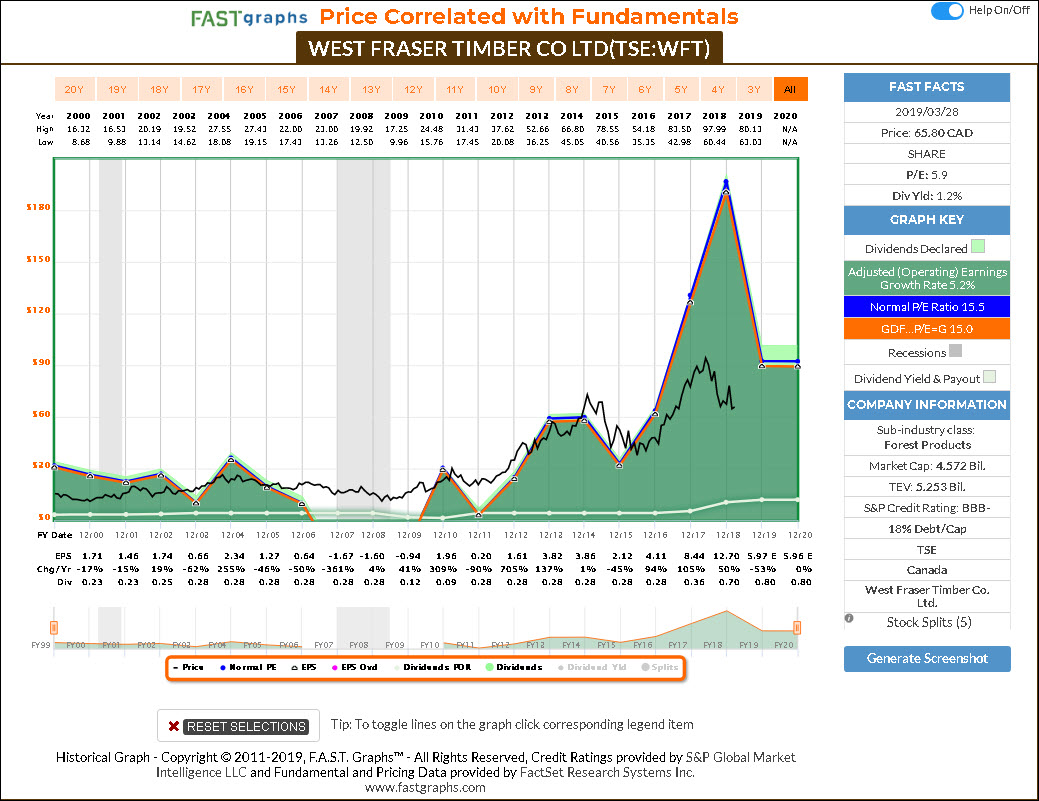

West Fraser Timber Co (WFT)

West Fraser Timber Co. Ltd. is an integrated wood products company. Its products include lumber, wood chips, plywood, pulp and newsprint. Its products include Spruce-Pine-Fir, laminated veneer, and southern yellow pine lumber, medium density fiberboard, plywood, treated wood, pulp and paper. The firm operates through the following segments: Lumber, Panels, Pulp and Paper, and Intracompany Fibre Sales.

The company was founded by Henry Holman Ketcham Jr., Samuel Kendall Ketcham, and William Peters Ketcham in 1955 and is headquartered in Vancouver, Canada.

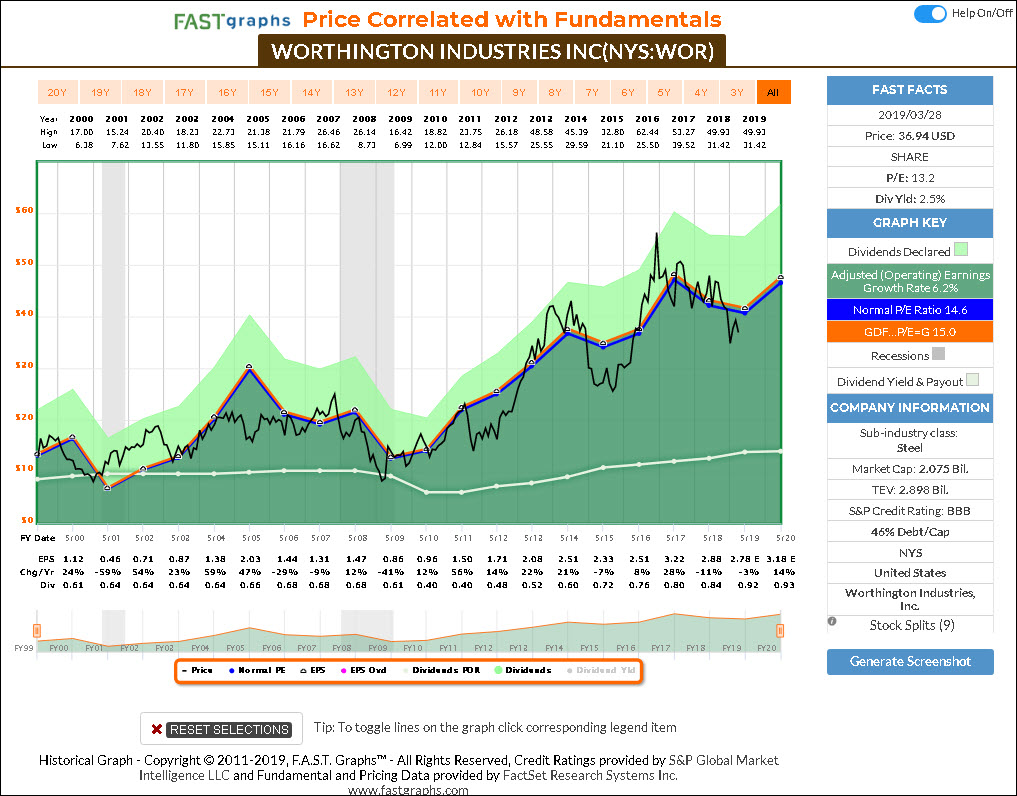

Worthington Industries (WOR)

Worthington Industries, Inc. engages in steel processing and manufacturing metal products. It offers pressure cylinder products such as propane, oxygen and helium tanks, hand torches, refrigerant and industrial cylinders, camping cylinders, scuba tanks, compressed natural gas cylinders and helium balloon kits; engineered cabs and operator stations and cab components; framing systems for mid-rise buildings; steel pallets and racks; and, through joint ventures, suspension grid systems for concealed and lay-in panel ceilings; laser welded blanks; light gauge steel framing for commercial and residential construction; and current and past model automotive service stampings. It operates through the following segments: Steel Processing, Pressure Cylinders, Engineered Cabs, and Others.

The Steel Processing segment include slitting, blanking, cutting-tolength, laser blanking, laser welding, tension leveling and warehousing. The Pressure Cylinders segment consists of the Worthington Cylinders business unit and Worthington Aritas. The Engineered Cabs segment refers to the Worthington Industries Engineered Cabs business unit, a noncaptive designer and manufacturer of high-quality, custom-engineered open and enclosed cabs and operator stations and custom fabrications for heavy mobile equipment used primarily in the agricultural, construction, forestry, military and mining industries. The Other segment involves Worthington Energy Innovations.

The company was founded by John H. McConnell in 1955 and is headquartered in Columbus, OH.

F.A.S.T. Graphs Analyze Out Loud Video:

Even though I am reluctant to offer any of the stocks covered in this article as attractive research candidates, I do believe there is a great deal of value that can be gleaned from reviewing them. First and foremost, these companies provide clear and undeniable evidence that business results are what generate returns over the long run. In other words, the examples presented in the following video clearly illustrate that operating results are more important and relevant than shorter-term stock price volatility.

Summary and Conclusions

I believe it is critically important for investors to understand as clearly as possible the nature of the companies they are considering investing in and the general nature of the sector those companies operate in. I have never believed in investing in a stock with only the hope that it might go up or that it might pay me an attractive dividend. Instead, I have always endeavored to have a calculated rate of return objective for each of my stock investments based on reasonable expectations of the future.

However, in order to accomplish that, I feel that I need to identify companies and/or sectors that provide reasonably predictable and consistent past, present and future results. I don’t see that with the Non-Energy Minerals Sector. Instead, I see a lot of cyclicality, a lot of erratic earnings growth and very unpredictable dividend income streams. Consequently, my personal view is to leave investments in this sector to those with a more short-term trading orientation. As a long-term buy-and-hold focused investor, I find little to like in this sector.

On the other hand, I found my efforts in researching companies in this sector to be a very worthwhile endeavor. I believe this sector speaks volumes about the importance of focusing on the business and its operating results versus obsessing with short-term price activity. In the long run, earnings and/or cash flows determine market price and dividend income. That sword cuts both ways.

Disclosure: No positions.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.