Introduction

Although some might disagree, I believe that investors either in retirement, or close to becoming retired, should be a little more conservative with how their portfolios are positioned. This position is primarily predicated on the reality that investors in retirement do not have the luxury of the time often needed to recover from bad decisions, or from bad market environments in general.

In conjunction with this more prudent and conservative portfolio positioning, retired investors are best served to take a long-term buy-and-hold investment strategy. Consequently, this would also apply that retired investors should favor consistent and predictable performance over inconsistent and erratic performance. This further supports the prudence of investing in blue-chip high-quality dividend growth stocks for the equity portion of their portfolios.

I believe the biggest advantage that blue-chip dividend growth stocks offer retired investors is a predictable and consistent growth of dividend income regardless of market price behavior. Common sense, and historical reality, clearly validates the prudence of steady dividend growth over highly volatile market price action. With dividend growth stocks, the income stream is highly predictable whereas the capital appreciation component fluctuates along with emotionally charged market reactions.

Therefore, I am not in favor of chasing yield in retirement accounts, especially in highly volatile mREITs. To be clear, this particular asset class is volatile and erratic with both price and dividends. With that said, many mortgage REITs (mREITs) are currently offering extremely high double-digit yields that capture the attention of income seeking investors such as retirees. The following stock price quotation courtesy of Seeking Alpha shows that the popular mREIT, Annaly Capital Management (NLY), statistically speaking appears to be an extremely attractive dividend stock with a very low valuation and a high dividend yield (highlights in yellow are mine).

Wow, an investor might conclude, a dividend yield of almost 12% and a P/E ratio of only 8 which is approximately half the valuation that most stocks trade at. Since I am looking for income, this is almost too good to be true – or is it? Now, I understand (especially considering today’s generally low interest rate levels), how investors might become smitten with double-digit yields. On the other hand, I believe if those same investors look closer under the hood, they might have a different attitude and perspective.

Annaly Capital Management Historical Performance

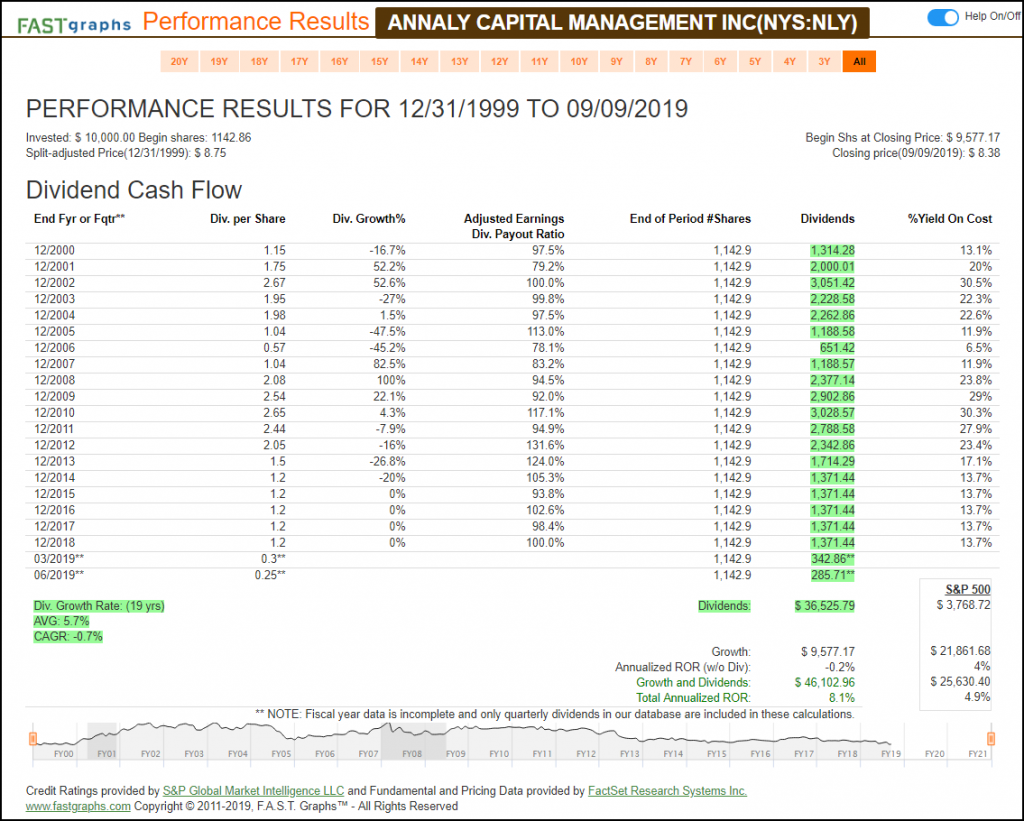

For starters, a bottom-line examination of Annaly’s cumulative dividend production over the last couple of decades is nothing short of awesome. A $10,000 investment made on December 31, 1999 would have generated $36,525.79 in dividends through June 2019. That is approximately 10 times the dividend income that an equal investment in the S&P 500 would have produced. The average retiree would be quite happy with those long-term dividend income results.

However, I would question whether the average retiree would have been willing to hold onto this company over that timeframe so that they could have achieved those dividend income results. A closer look suggests that a buy-and-hold approach to Annaly since 2000 would have presented several challenges. Here is the full dividend record:

The reader should note not only the many dividend cuts, but the general inconsistency of the dividend payments as well. Additionally, capital appreciation over this timeframe was very poor relative to the average company. As you can see, Annaly shareholders barely broke even. However, the total return that shareholders received since 2000 was superior to the overall market.

Nevertheless, even though the outcome was palatable, the journey was treacherous and nerve-racking. I highly doubt that most retired investors would have been capable of staying the course to achieve those results. Additionally, when you examine different timeframes you get significantly different outcomes, most of which underperform the market on a total return basis (I will be presenting this in detail in the video below). Consequently, I do not consider Annaly – or mortgage REITs for that matter -suitable for retirement accounts despite the high yields.

“Investment Must Be Rational; If You Don’t Understand It, Don’t Do It” Warren Buffett

In addition to what I covered above, one of my primary issues with including mortgage REITs in retirement accounts is the complexity of their business models. As the title of this section suggests, I find the business model of mortgage REITs both complex and confusing. The following excerpt taken from Nariet attempts to explain the business model of mREITS. Although I generally understand what they do, I consider it extremely difficult to attempt to forecast future results. Consequently, I personally have little confidence in evaluating mREITS, and even less in attempting to forecast what their futures would hold for me as a shareholder.

“Nariet: The mREIT Business Model

mREITs hold mortgages and MBS on their balance sheets, and fund these investments with equity and debt capital. Their general objective is to earn a profit from their net interest margin, or the spread between interest income on their mortgage assets and their funding costs. mREITs rely on a variety of funding sources, including common and preferred equity, repurchase agreements, structured financing, convertible and long-term debt and other credit facilities. mREITs raise both debt and equity in the public capital markets.

mREITs typically use less borrowing and more equity capital to finance their acquisitions of mortgages and MBS than do other large mortgage investors.”

Common Shares Outstanding

The last sentence above also presents an issue I have with investing in mREITS – extreme dilution. Later, when I show earnings per share and other metrics, look back on how dilutive these businesses are to shareholders. Since 1998 Annaly Capital Management’s shares outstanding have increased from 13 million to 1.2 billion by the end of 2018. That is a compound annual growth rate (dilution rate) of 25.4% per annum to shareholders.

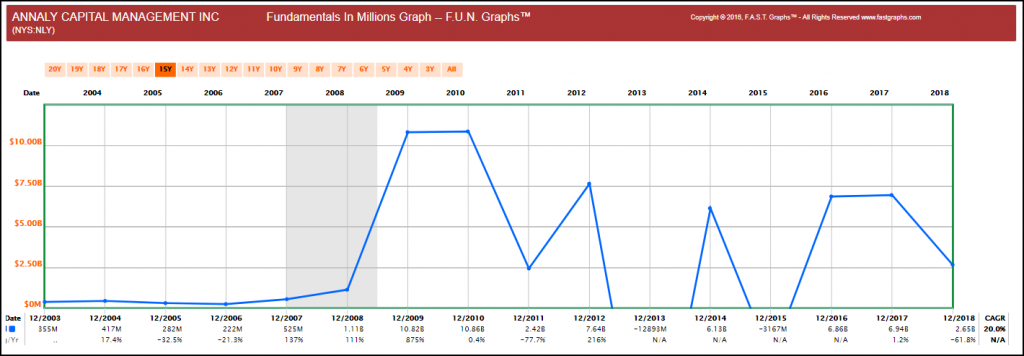

Operating Cash Flow Per Share

As a result of the complexity of the mortgage REITs’ business model in conjunction with the dilution mentioned above, operating cash flow tends to be very erratic – even turning negative in many years. Therefore, it is no wonder that mREITs have such spotty dividend records. It is hard to pay and/or increase your dividends when cash flows are collapsing, or worse yet, turning negative. The following graphic plots Annaly Capital Management’s operating cash flow since 2003.

mREITs Risks and Risk Management:

Since mREITs operate in such a dynamic market, it is incumbent on management to be able to deal with many types of risk. However, this also implies utilizing many hedging strategies that are very difficult for the lay investor, and for that matter, the professional investor to understand and evaluate.

Here is what NARIET has to say about Risks and Risk Management

“Risks and Risk Management

Most mREITs are registered with the SEC and are required to publish regular financial statements for review and monitoring by investors and analysts. The business risks that mREITs face are similar to those of other financial firms. mREITs have considerable experience managing many types of risk:

Interest Rate Risk. Managing the effects of changes in short- and long-term interest rates is an essential element of mREITs’ business operations. Changes in interest rates can affect the net interest margin, which is mREITs’ fundamental source of earnings, but also may affect the value of their mortgage assets, which affects corporate net worth.

mREITs typically manage and mitigate risk associated with their short-term borrowings through conventional, widely-used hedging strategies, including interest rate swaps, swaptions, interest rate collars, caps or floors and other financial futures contracts. mREITs also manage risk in other ways, such as adjusting the average maturities on their assets as well as their borrowings and selling assets during periods of interest rate volatility to raise cash or reduce borrowings.

Credit Risk. The bulk of mortgage securities purchased by residential mREITs are agency securities backed by the federal government, which present limited credit risk. Commercial mREITs may be exposed to credit risk through their private-label RMBS and CMBS. The degree of credit risk for a particular security depends on the credit performance of the underlying loans, the structure of the security (that is, which classes of security are paid first, and which are paid later), and by the degree of over-collateralization (in which the face amount of the mortgage loans held as collateral exceeds the face amount of the RMBS or CMBS issued).

Prepayment. Changes in interest rates or borrower home sales affect the probability that some borrowers will refinance or repay their mortgages. When such a refinancing or repayment occurs, the investor holding the mortgage or MBS must reinvest the proceeds into the prevailing interest rate environment, which may be lower or higher. mREITs seek to hedge prepayment risk using similar tools and techniques as those they use to hedge against interest rate risks.

Rollover. mREIT assets are mainly longer-term MBS and mortgages, while their liabilities may include a significant amount of short-term debt, especially among residential mREITs. This term mismatch requires that they roll over their short-term debt before the maturity of their assets. Their ability to do so depends on the liquidity and smooth functioning of the short-term debt markets, including the repo market. The repo market is extremely liquid, with an estimated $2 trillion in outstandings and several hundred billion dollars in daily trading volume. Banks and dealers also use the repo market as an important source of market liquidity. In the financing markets, the liquidity of the agency MBS and TBA (To Be Announced) markets is comparable to the market for Treasuries. Commercial mREITs tend to match the duration of their assets and liabilities and face little rollover risk.”

FAST Graphs analyze out loud video: Annaly Capital Management

Proponents of mREITs like to tout the notion that dividend growth stocks are potentially overvalued because of their expected growth. Consequently, they believe that future growth will stagnate when the economy slows. In contrast, they will also promote mREITs’ tendency to outperform when the market is underperforming.

This is fine and good and has proven true over our last two recessions. On the other hand, there is a problem with this when your investment horizon is long-term. What these promoters do not point out is the fact that recessions and bad markets tend to be very short-lived, whereas bull markets tend to last much longer. Consequently, the advantage that a mREIT like Annaly Capital Management might offer during a recession, tends to be very short-lived.

In the video that follows, I will illustrate this performance anomaly as well as highlight the long-term risks that I believe mREITs engender. The most insightful and I consider important part of this article will be found in the video, please watch it for your own edification.

Summary and Conclusions

I do believe that there are certain circumstances, and investor types that might find mREITs viable investments, even attractive long-term investments. The secret to making a mREIT a successful long-term investment is to diligently reinvest the dividends. Investors that can do this, and can do it over the long run, can produce acceptable and even attractive long-term returns through investing in mREITs.

However, I do believe that these investor types are rare and in the minority. In reality, it takes a great deal of fortitude to be able to have the confidence to stay the course long enough in mREITs in order to take advantage of the benefits that they offer. Most investors are not capable of enduring significant volatility in both price and dividends.

On the other hand, for the reasons stated in the article and clearly illustrated in the video, I don’t consider mREITs suitable selections for retirement accounts despite their high yields. Therefore, this will be the first of 7 installments on some of the most popular and widely recognized mREITs. My primary purpose and objective is to ensure that all investors, and especially retired investors, understand the reality of investing in high-yielding mREITs.

Disclosure: No position.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.