Introduction

This is the third in a series of articles where I will be covering the historical performance and operating results of popular and highly recognized mREITs (mortgage REITs). In my first installment, I covered Annaly Capital Management (NLY) found here; in my second installment I covered Dynex Capital, Inc. (DX) found here; with this installment I am covering AGNC Investment Corp (AGNC).

Hopefully, for anyone that has followed this series, they would recognize by now that although these are all mortgage REITs with very high current yields, they are far from high return investments. In my previous two examples, I did illustrate that these companies generate a lot of cumulative dividend income over time, but simultaneously have been destroying principal. Additionally, they all have histories of cutting their dividends significantly and doing it numerous times in lockstep with their falling earnings. Consequently, despite their high current yields, they have produced rather anemic total return track records.

As a result, I have personally suggested that I do not consider them suitable instruments for retirement accounts. However, I want to clarify my position as well as clearly state why I don’t consider these suitable for retirees looking for or needing income to live off.

Characteristics of Suitable Investments for Retirement Accounts

In my personal experience working with and talking with retired investors I believe I have a pretty good handle on what most retirees want – and perhaps more importantly – need. Retirees have generally worked long and hard for their money, and their retirement accounts generally represent their life savings.

Consequently, most retirees that I have talked to and worked with have given a clear message regarding what they want and what they need. For starters, they would like to think that they could get their hard-earned money to now work for them as hard as they worked for it.

Additionally, and contrary to what many might suggest, retirement doesn’t need to mean a reduced standard of living. This notion is often associated with another notion suggesting that retirees should choose fixed income over equities. Therefore, when and if the retiree does overweight fixed income, their fixed future incomes will be ravaged by inflation, and therefore, their standard of living will potentially diminish with time.

Of course, the idea of recommending fixed income is further predicated on the notion that it is safer than equity. At first glance, this seems to make sense, because most retirees that I talked to also stress a need and desire for safety. They intuitively and intelligently understand that they will not have the luxury of many decades of time to recoup losses if they should occur. As a result, the concept of safety is most often attached to preservation of capital (not losing their principal).

Furthermore, retirees often also associate safety with predictability. Retirees want and need to believe that their portfolios are producing a stable and preferably growing level of income. In my opinion, this is precisely why so many retirees are attracted to dividend growth investing as a strategy that can meet their goals and needs. Therefore, as a general statement, companies with long histories of increasing their dividend every year are desirable, and companies that reduce or cut dividends are considered undesirable.

Finally, most retirees understand that if it sounds too good to be true, it probably is. Consequently, the most prudent, and I would argue most intelligent retirees are smart enough not to chase yield.

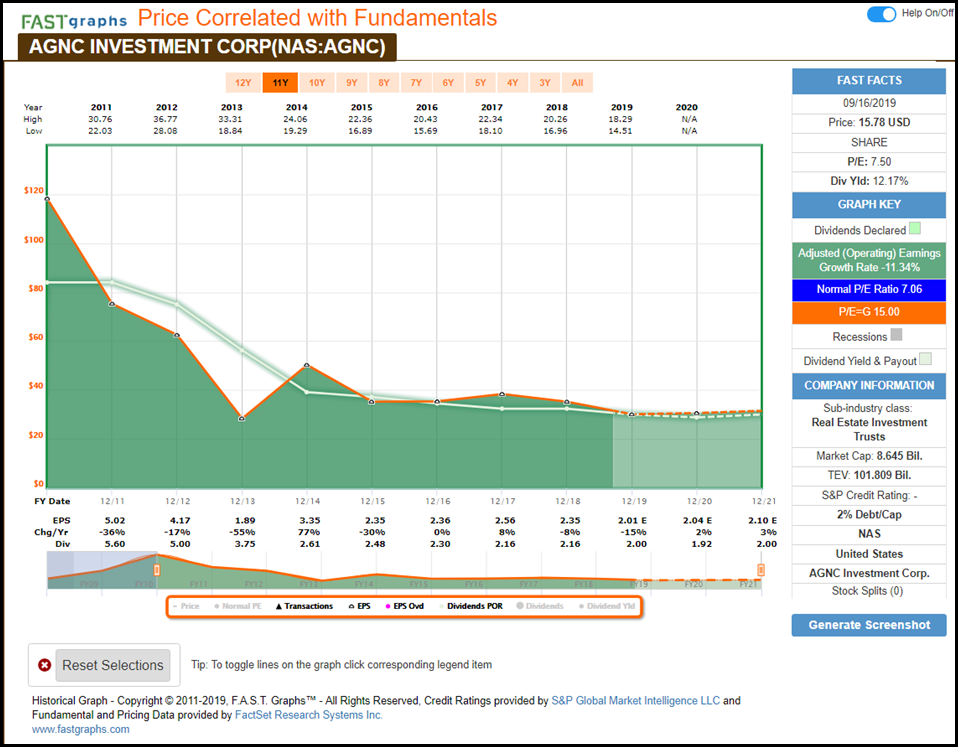

AGNC Investment Corp: Earnings and Dividends Only

Since mortgage REITs don’t own real estate, they are appropriately valued utilizing operating earnings. The following graphic clearly illustrates why I don’t believe that mortgage REITs are suitable for retirement portfolios based on the criteria stated above.

The reader should note that operating earnings (the orange line on the graph) have been in a steady freefall since the beginning of 2011, and dividends (the white line) have fallen suit. This is a vital perspective that in my mind, clearly demonstrates why these are not suitable for prudent retirement accounts. Unfortunately, most investors don’t have this perspective. All they see are statistics telling them that the valuations appear low (P/E ratios) and the dividend yields high (current yield 12.17%).

AGNC Investment Corp: Performance By The Numbers

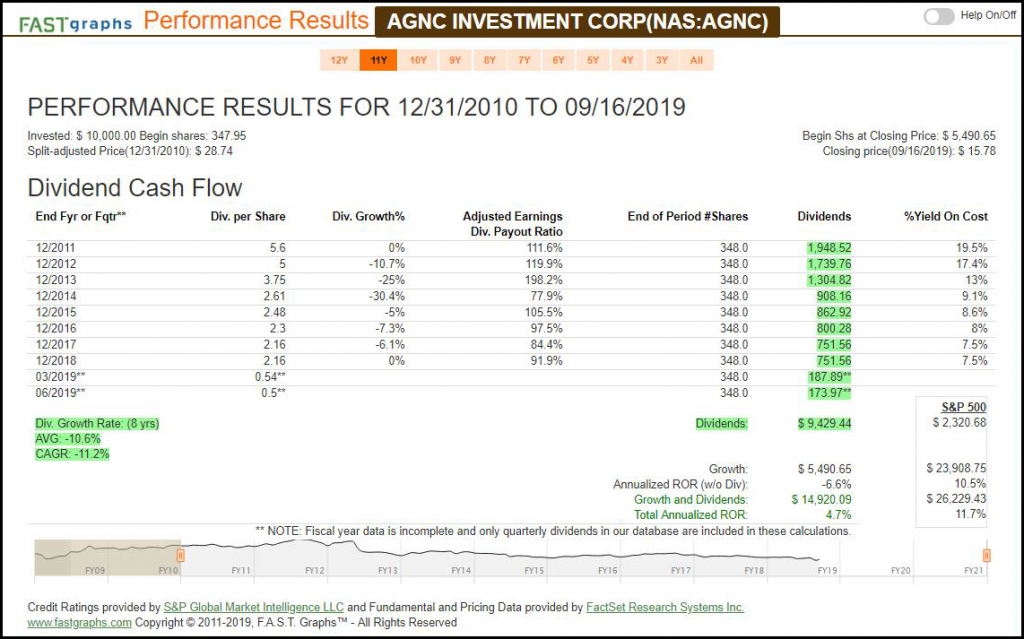

However, when you evaluate long-term performance by running the numbers, a more somber perspective comes to light. For starters, even though the current yield appears high at first glance, the long-term reality tells an entirely different story. AGNC has reduced their dividend at a compound annual growth rate (CAGR) of -11.2% since 2011.

To put this into perspective, had an investor put $10,000 in the stock on December 31, 2010, they would have received $1948.52 in dividend income that year. However, their income would have fallen to $751.56 by year-end 2018 and is forecast to fall another 4% in 2019. That’s not your money working hard, that is your money hardly working.

Furthermore, this is significantly more severe than inflation eating away at fixed income. This is destruction of your income on top of inflation. Consequently, if you are living off your dividend income, your standard of living would be severely reduced.

As this relates to safety, not only has dividend income fallen since 2010, your principal would have been ravaged as well. That original $10,000 investment made on December 31, 2010 would only be worth $5490.65 through yesterday’s close. That is not price volatility, nor is that cyclicality, that is protracted financial destruction. Since I postulated that safety relates to preservation of capital, this mortgage REITs hardly meets that criteria.

Finally, the only thing that has been predictable with this company so far has been weakening fundamentals and dividend income. That is not the kind of predictability that retired investors are looking for. Instead, prudent retired investors want to see a steadily rising level of income. They might be able to withstand some volatility along the way, but volatility is not the same as a steadily falling stock price for more than 8 years in a row. Consequently, I would not call this mortgage REIT a cyclical investment, instead, I would call it a financial instrument of capital destruction.

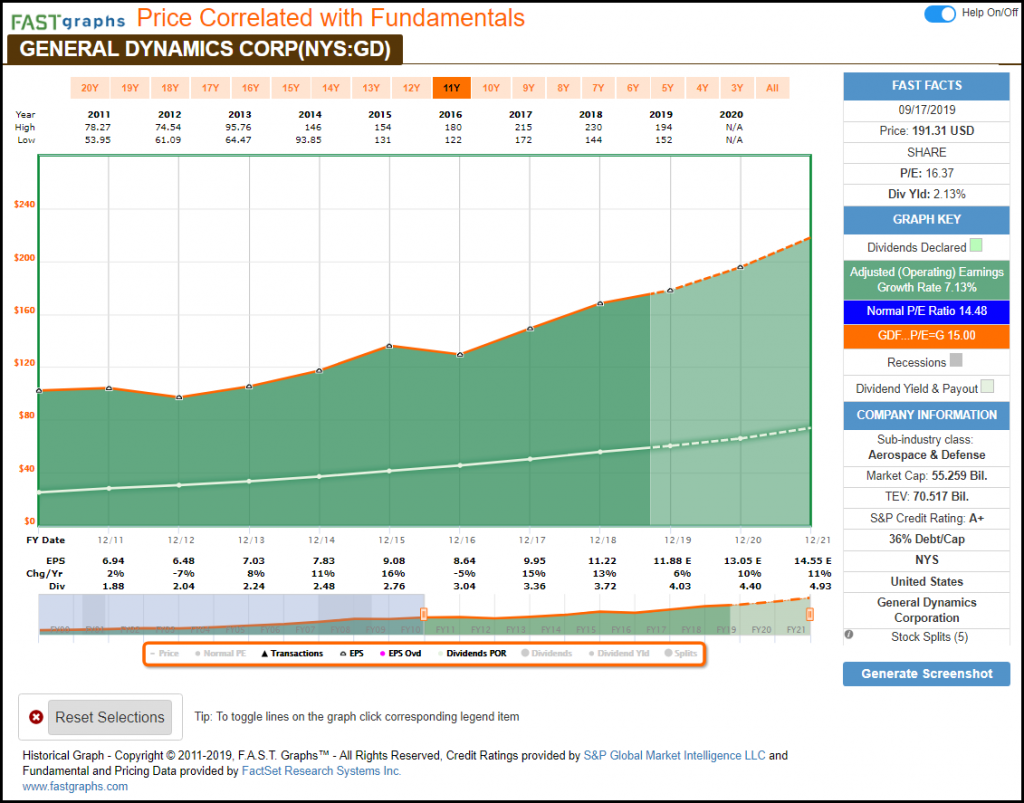

General Dynamics: Earnings and Dividends Only

For perspective, I offer the following Dividend Aristocrat, General Dynamics (GD), which is a high-quality dividend growth stock that I do consider suitable for retirement accounts. Allow me to list the primary differences I see.

First and foremost, General Dynamics has grown earnings at an average rate of 7.13% since the beginning of 2011 in contrast to AGNC whose earnings were reduced by -11.34% per annum. Therefore, we have a consistently growing A+ rated dividend growth blue-chip that is steadily increasing shareholder value versus a mortgage REIT that is not rated that has been steadily diminishing shareholder value.

But perhaps most importantly, as it relates to retired investors relying on their dividend income to live off, General Dynamics has consistently increased its dividend each year. Consequently, retired shareholders have and can continue to look forward to seeing their dividend income increase each year.

General Dynamics: Performance By The Numbers

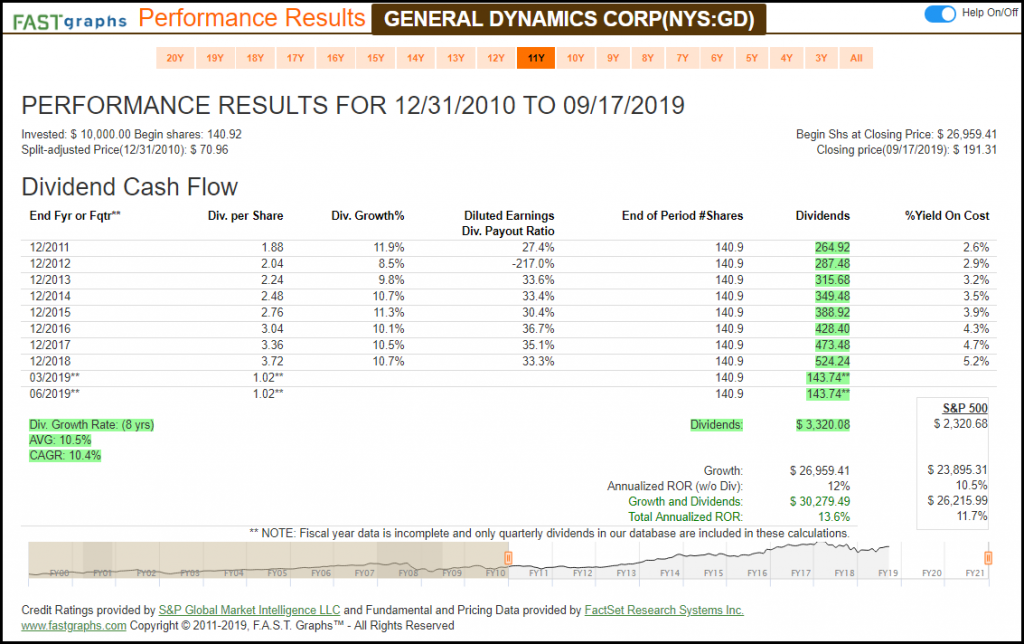

Moving on to a performance comparison we see that our blue-chip dividend growth stock has provided its retired shareholders with a consistent dividend growth rate averaging 10.5% per year. Although our dividend income was admittedly less than what our mortgage reproduced, it did have the advantage of growing steadily every year rather than being reduced each year. Consequently, retired shareholders received a consistent and reasonably predictable income increase each year. That’s analogous to getting a raise in pay each year.

Furthermore, our dividend growth stock has also increased our principal 2.7 times over this timeframe; whereas AGNC reduced our principal by over 45%, shrinking our original $10,000 investment into a mere $5483.69. Moreover, when dividends are included in the total return calculation (assuming they were spent not reinvested) we also discover that our Dividend Aristocrat also outperformed the general market over this timeframe.

mREIT AGNC Investment Corp vs Dividend Aristocrat General Dynamics: FAST Graphs Analyze out Loud Video

The primary focus of the following video will be to illustrate why I do not consider AGNC a suitable choice for the retirement accounts of investors that are already retired. I will accomplish that by providing a perspective beyond current statistics. AGNC was founded in 2008, and it could be argued that our long-running bull market since that time has been a worst-case environment.

Nevertheless, it has brought more than a decade of subpar total return performance despite the stock offering high current yields. Therefore, my objective is to take the blinders off the reader’s eyes thereby moving from a narrow-minded look at current statistics to a broader and I believe clear longer-term view and perspective. I believe a good way to accomplish this is by also contrasting AGNC and its long-term performance with the blue-chip Dividend Aristocrat General Dynamics.

Summary and Conclusions

I am hopeful that this series has opened investors’ eyes to the reality that high-yield does not imply high return. In fact, in most cases, just the opposite is true. On the other hand, high yield typically does imply high risk and often leads to below-average total returns. Taking on high risk to get a lower rate of return is the exact opposite of what taking on high risk should be about. In theory at least, we should only take on higher risk with the expectation of earning higher returns as our reward.

Additionally, I am hopeful that this series has also opened investors’ eyes to the reality that statistics don’t always tell the complete story. Statistically speaking AGNC looks quite attractive. Their blended P/E ratio is only 7.5 which would normally indicate a very low valuation. Their current yield of 12.17% is extremely high relative to current interest rates and yields on most securities.

However, this high-yield is very misleading considering how often and how drastically this mortgage REIT has cut its dividend. Regarding what appears to be a low P/E ratio, that is only true if the business is growing. As clearly illustrated, that has not been the case for AGNC since it was founded in 2008.

In closing, for all the reasons stated above, I do not believe that high yielding mortgage REITs are suitable investments for prudent retirement accounts where the retiree needs their dividend income to live off. I would acknowledge that there might be ways to trade these mortgage REITs and/or speculate in them. Nevertheless, I do not consider them prudent and conservative long-term buy-and-hold investments as I believe retirees should strive for. Caveat emptor.

Disclosure: Long GD.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.