Introduction

Throughout this series I have referenced the idea that the stock market in the general sense may be overvalued, or at least fully valued. On the other hand, I have also pointed out that it is a market of stocks and not a stock market. In that vein, I have suggested that there are many companies in virtually every sector that are either attractive or undervalued despite general market levels. However, I have also suggested that there are certain sectors such as the Finance Sector where low valuations were abundant.

In contrast, the Technology Services Sector covered in this article is a sector where overvaluation is rampant. In other words, this is currently a hot sector where sound valuation has been thrown out the window in favor of what I can only describe as hype and speculation. Importantly, it has long been my contention that you can overpay for even the best companies. In my humble opinion, this is precisely what is happening in the Technology Services Sector with names such as Autodesk Inc., Microsoft, Accenture, Adobe and many more too numerous to mention. Although these are all great companies, I believe they are also all great companies that are being significantly overvalued by the market. With this article, I will be covering only 5 that are not.

A Sector By Sector Review

This is part 17 of a series where I have conducted a simple screening looking for value over the overall market based on industry classifications and subindustry classifications reported by FactSet Research Systems, Inc.

In part 1 found here I covered the Consumer Services Sector. In part 2 found here I covered the Communication Sector. In part 3 found here I covered the Consumer Durables Sector and its many diverse subsectors. In part 4 found here I covered Consumer Nondurables. In part 5 found here I covered companies in the Consumer Services Sector. In part 6 found here I covered the Distribution Services Sector. In part 7 found here I covered the Electronic Technology Sector. In part 8 found here I covered the Energy Minerals Sector. In part 9 found here I covered the Finance Sector. In part 10 found here I covered the Health Services Sector. In part 11 found here I covered the Health Technology Sector. In part 12 found here I covered the Industrial Services Sector. In part 13 found here I covered the Non-Energy Minerals Sector. In part 14 found here I covered the Process Industries Sector. In part 15 found here I covered the Producer Manufacturing Sector. In part 16 found here I covered the Retail Trade Sector.

In this part 17 I will be covering the Technology Services Sector.

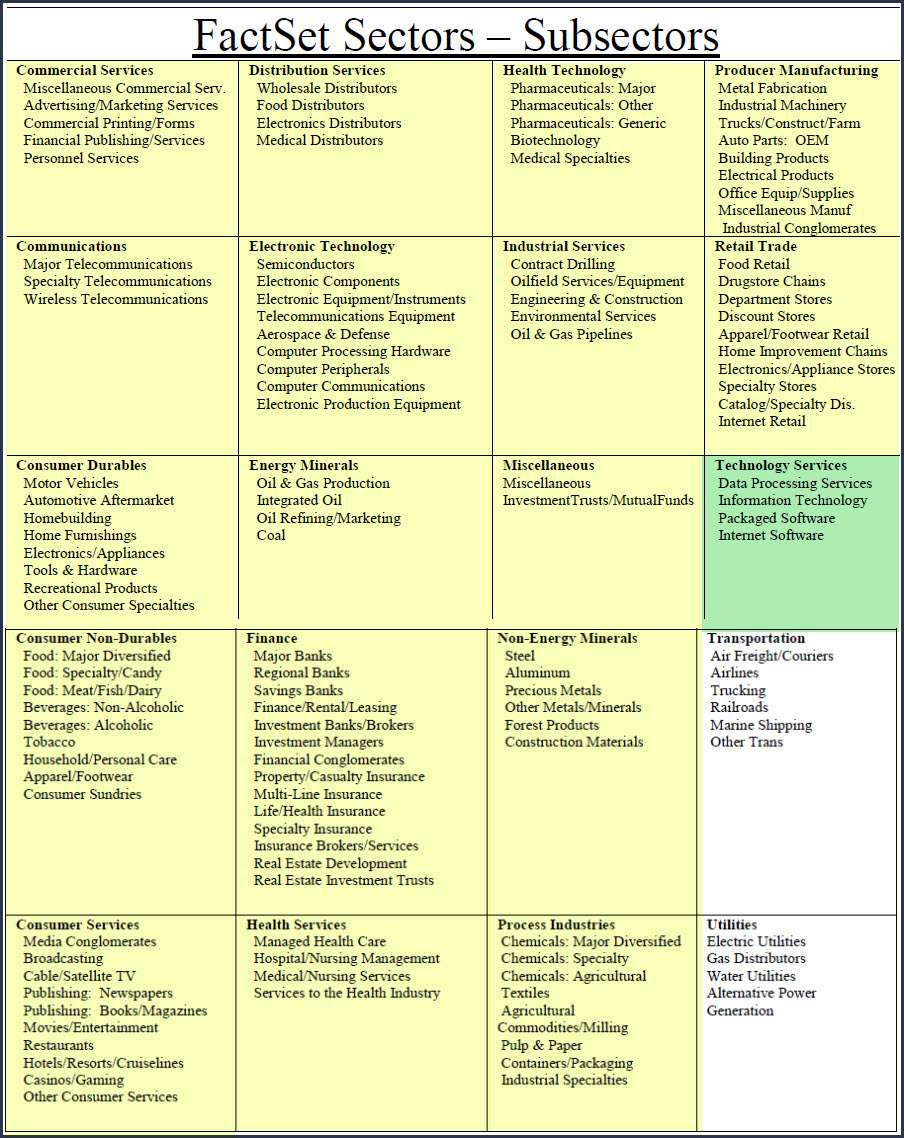

In each article in this series, I will be providing a listing of screened research candidates from each of the following industry sectors, the sector I’m covering in this article is marked in green:

Sector 17: Technology Services

- Data Processing Services

- Information Technology

- Packaged Software

- Internet Software

A Simple Valuation and Quality Screening Process

With this series of articles, I will be presenting a screening of companies that have become attractively valued primarily as a result of the bearish market activities experienced in 2018 from each of the above sectors. I will be applying a rather simple valuation and quality-oriented screen across each of the sectors. First, I have screened for investment-grade S&P credit ratings of BBB- or above. Next, I have screened for low valuations based on P/E ratios between 2 and 17. Finally, I have screened for long-term debt to capital no greater than 70%.

By keeping my screen simple, and at the same time rather broad, I will be able to identify attractively valued research candidates that I might have overlooked through a more rigorous screening process. In other words, I’m looking for fresh ideas that I might have previously been overlooking. Furthermore, I want to be clear that I do not consider every candidate that I have discovered as suitable for every investor. However, I do consider them all to be attractively valued. Additionally, I also believe that every investor will be able to find companies to research that meet their own goals, objectives and risk tolerances as this series unfolds.

Portfolio Review: Technology Services Sector: 5 Research Candidates

FAST Graphs Screenshots of the 5 Research Candidates

The following screenshots provide a quick look at each of the 5 candidates screened out of over 19,000 possibilities. However, there are only 668 companies categorized as Technology Services, and these 5 were the only ones I was comfortable presenting in this article. The company descriptions are provided courtesy of the Wall Street Journal. In the FAST Graphs analyze out loud video that follows the screenshots, I will provide additional details and thoughts on the possible attractiveness as well as the potential negatives of each of these research candidates.

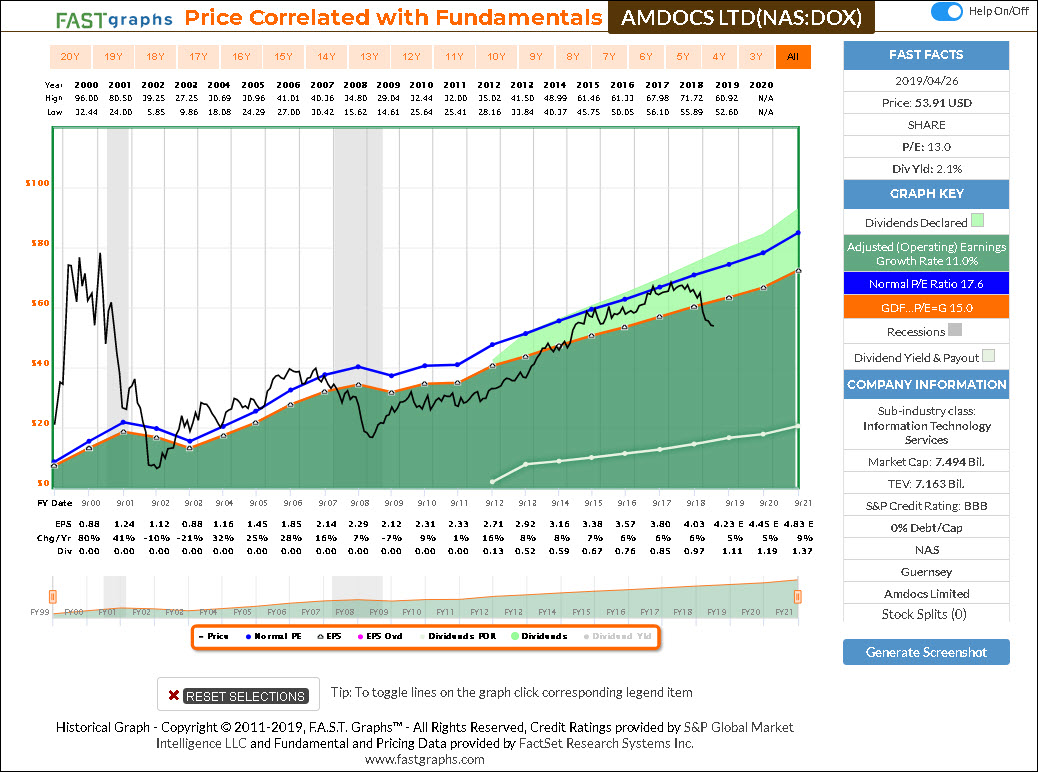

Amdocs (DOX)

Amdocs Ltd. is a holding company, which engages in the provision of software and services solutions for communications, entertainment, and media industries. It specializes in the development, implementation, and management of software and services associate with business support systems, operational support systems, service-driven network and other network solutions, entertainment offerings, and digital solutions.

The company was founded in 1988 and is headquartered in Chesterfield, MO.

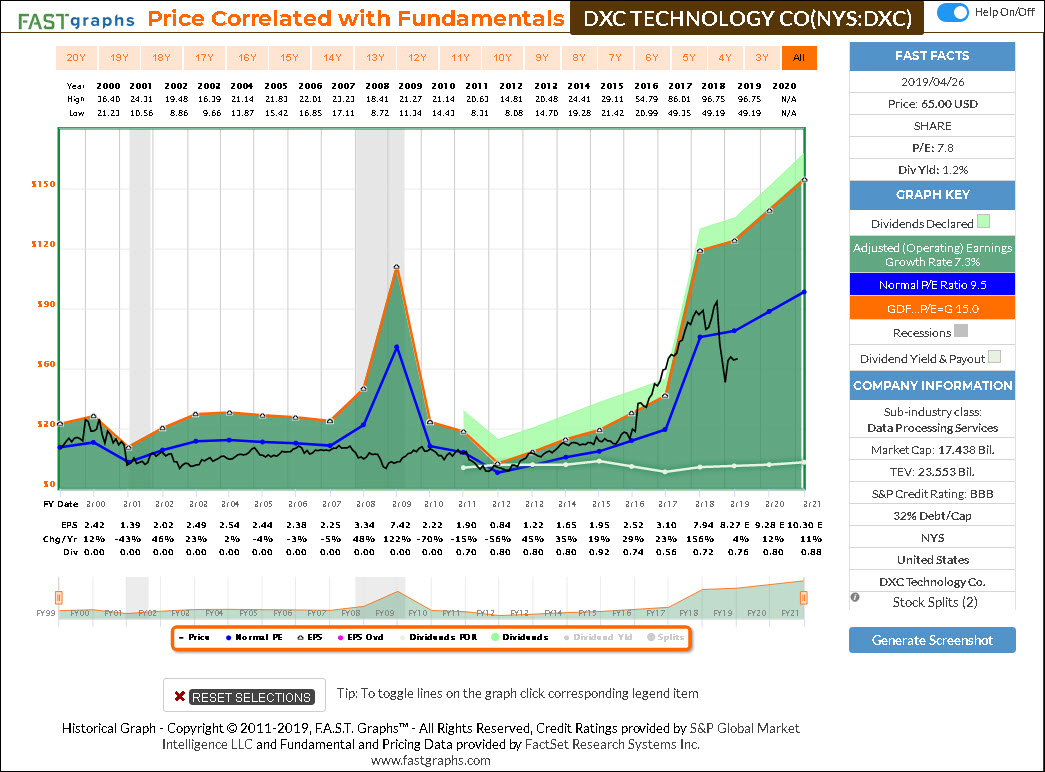

DXC Technology (DXC)

DXC Technology Co. provides technology consulting, outsourcing and support services. It operates through the following segments: Global Business Services (GBS), Global Infrastructure Services (GIS) and United States Public Sector (USPS). The GBS segment provides technology solutions that help clients address challenges and accelerates the digital transformations that is tailored to each client’s specific objectives. The GIS segment offers to deliver predictable outcomes and measurable results, while reducing business risk and operational costs for clients. The USPS segment delivers IT services and business solutions to all levels of government in the United States.

The company was founded on 1st April, 2017 and is headquartered in Tysons, VA.

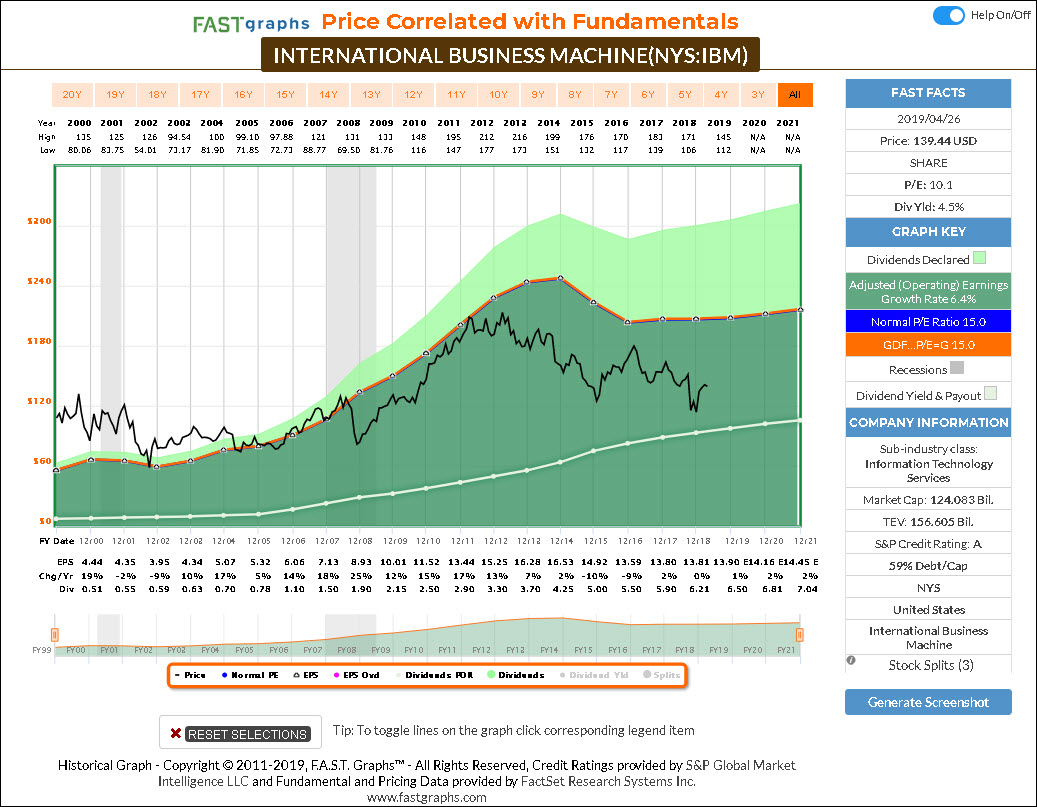

International Business Machines (IBM)

International Business Machines Corp. is an information technology company, which provides integrated solutions that leverage information technology and knowledge of business processes. It operates through the following segments: Cognitive Solutions, Global Business Services, Technology Services & Cloud Platforms, Systems, and Global Financing.

The Cognitive Solutions segment comprises a portfolio of capabilities that help IBM’s clients to identify actionable insights and inform decision making for competitive advantage. It includes Watson, a cognitive computing platform that has the ability to interact in natural language, process amounts of big data, and learn from interactions with people and computers. This segment consists of Solutions Software, which provides the basis for many of the company’s strategic areas including analytics, security and social; and Transaction Processing Software, which includes software that primarily runs mission-critical systems in industries such as banking, airlines and retail.

The Global Business Services segment provides clients with consulting, application management and global process services. The Technology Services & Cloud Platforms segment provides comprehensive IT infrastructure and platform services that create business value for clients. The Systems segment provides clients with innovative infrastructure platforms to help meet the requirements of hybrid cloud and enterprise AI workload. The Global Financing segment encompasses two primary businesses: financing, primarily conducted through IBM Credit LLC, and remanufacturing and remarketing.

The company was founded by Charles Ranlett Flint and Thomas J. Watson Sr. on June 16, 1911 and is headquartered in Armonk, NY.

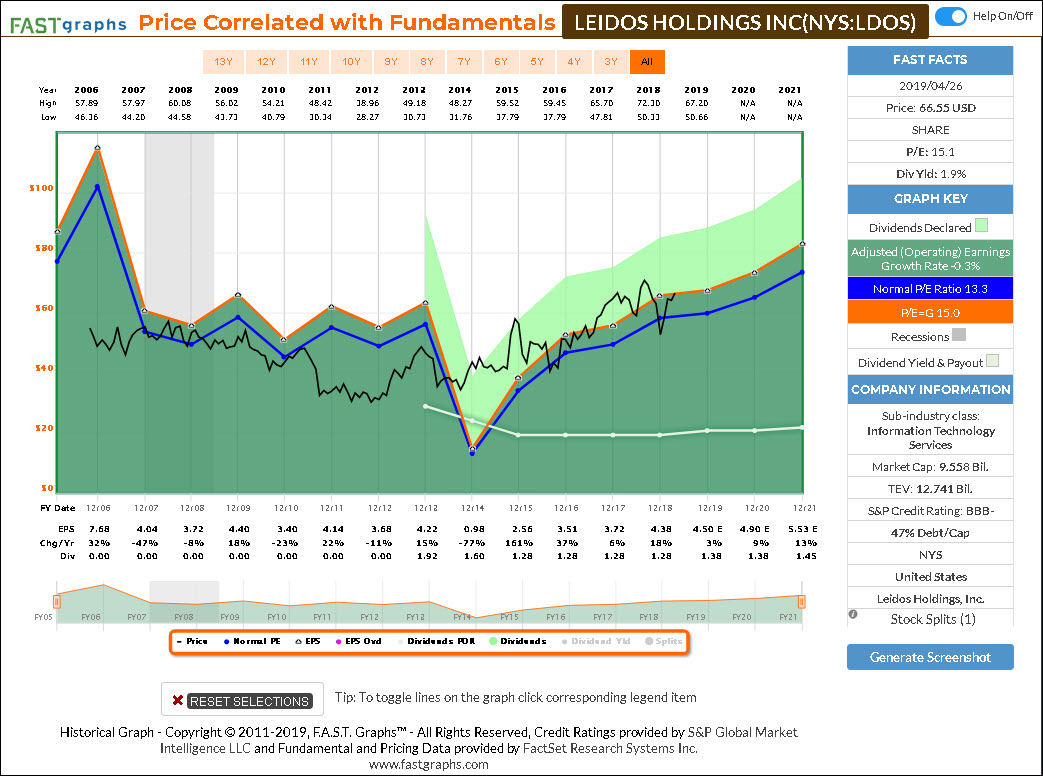

Leidos Holdings Inc (LDOS)

Leidos Holdings, Inc. is a holding company, which engages in the provision of scientific, engineering and information technology services and solutions in the areas of defense, intelligence, civil and health markets. It operates through the following three segments: Defensive Solutions, Civil, and Health. The Defensive Solutions segment focuses on deploying agile, cost-effective solutions to meet the ever-changing missions of the company’s customers in areas of intelligence surveillance and reconnaissance, enterprise IT and integrated systems and cybersecurity and global services.

The Civil segment focuses on seamlessly integrating and protecting physical, digital and data domains. The Health segment offers solutions to federal and commercial customers that are responsible for the health and wellbeing of people worldwide including service members and veterans.

The company was founded by John Robert Beyster on February 3, 1969 and is headquartered in Reston, VA.

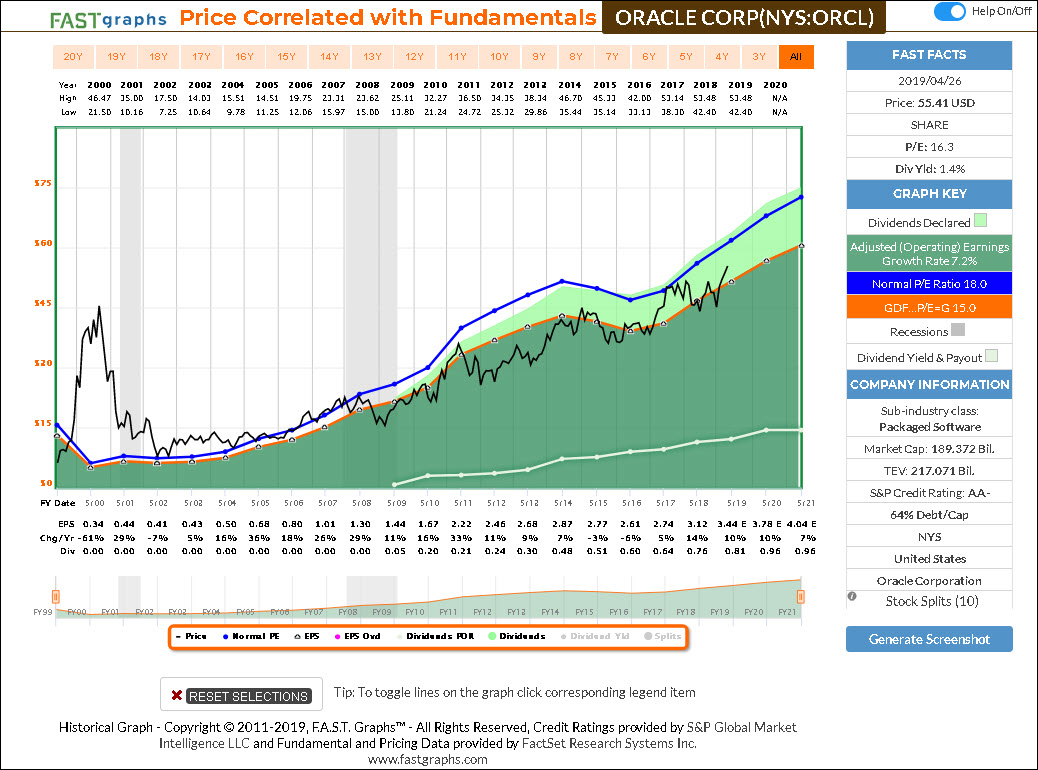

Oracle Corp (ORCL)

Oracle Corp. engages in the provision of products and services that address all aspects of corporate information technology environments. It operates through the following segments: Cloud and License, Hardware, and Services. The Cloud and License segment markets, sells, and delivers applications, platform, and infrastructure technologies. The Hardware segment provides hardware products and hardware-related software products including Oracle Engineered Systems, servers, storage, industry-specific hardware, operating systems, virtualization, management and other hardware related software, and related hardware support. The Services segment offers consulting, advanced support, and education services.

The company was founded by Lawrence Joseph Ellison, Robert Nimrod Miner, and Edward A. Oates on June 16, 1977 and is headquartered in Redwood City, CA.

F.A.S.T. Graphs Analyze Out Loud Video:

Summary and Conclusions

The Technology Services Sector is comprised of many companies that are excellent businesses in their own right. Consequently, it is also a sector comprised of many companies with exciting prospects for above-average future growth. Unfortunately, if you overpay to buy that growth you will not be participating in it as you would if you bought the stock at attractive valuations. As Warren Buffett once so aptly put it: “price is what you pay, value is what you get.”

Although I believe it’s important to invest in good businesses with bright futures, I also believe it’s equally as important to only invest your money when the numbers justify the risk you are assuming. Caveat emptor!

Disclosure: Long IBM,LDOS,ORCL

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.